Since the first publication of the S&P Indices Versus Active (SPIVA) U.S. Scorecard in 2002, S&P Dow Jones Indices has been the de facto scorekeeper of the ongoing active versus passive debate.

This edition marks the first release of the SPIVA Asia Ex-Japan Scorecard, which measures the performance of actively managed funds relative to relevant benchmarks for domestic equity, international equity and bond funds available in Greater China, Korea and Southeast Asia.

Highlights

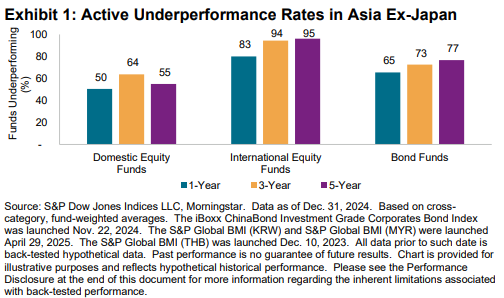

In 2024, a majority of actively managed funds underperformed across domestic equity, international equity and bond fund categories. The underperformance rates generally increased as time horizons lengthened. Exhibit 1 summarizes the percentage of underperforming funds over one-, three- and five-year periods ending in 2024.

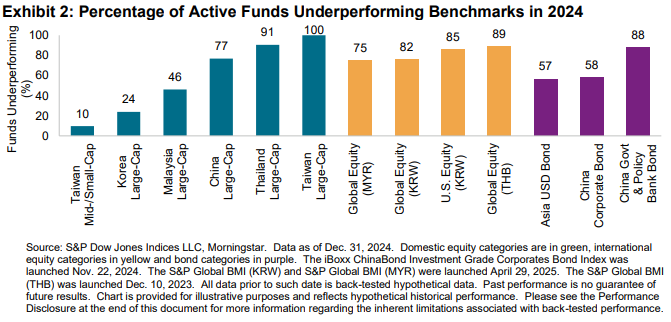

- While rising markets were generally welcomed by both fund managers and their clients, 2024 proved to be a challenging year for active managers in Asia ex-Japan seeking to outperform, with a majority (greater than 50%) of funds underperforming their assigned benchmark in 10 out of 13 fund categories (see Exhibit 2).

- Domestic equity funds displayed a wide range of beat rates across categories. Taiwan Mid-/Small-Cap funds excelled, with 90% of funds outperforming the S&P Taiwan MidSmallCap, followed by Korea Large-Cap funds, where about three quarters surpassed the S&P Korea BMI’s poor performance of -10.7%.

- Conversely, all Taiwan Large-Cap funds fell short of the S&P Taiwan BMI’s impressive 35.3% return. Additionally, over three quarters of China Large-Cap funds struggled to keep pace with the market, which experienced a strong rebound in Q4.

- Outperformance was scarce among international equity funds. More than three quarters of Global Equity funds in Korea, Malaysia and Thailand underperformed the S&P Global BMI in their respective local currencies, reflecting trends observed in other markets. The higher underperformance of funds domiciled in Korea may have been partially driven by the negative impact of currency hedging amid a sharp depreciation of the Korean won.

- All three bond fund categories showed majority active underperformance. China Government and Policy Bank Bond funds had the highest underperformance rate (88%), versus the iBoxx ChinaBond Government & Policy Banks Bond Index’s robust 8.4% gain.