Introduction

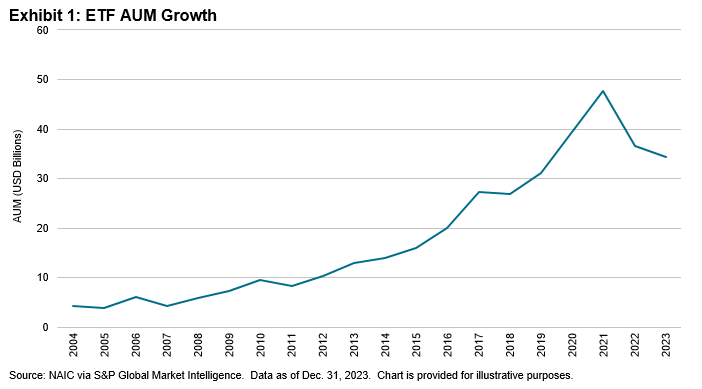

In 2023, U.S. insurers held USD 34.4 billion in exchange-traded funds (ETFs). For the second year in a row, we saw large outflows from large insurers. In 2022, the bear market exacerbated the outflows to decrease AUM by 23%. In 2023, the market acted against the outflows and AUM only decreased by 6%.

One company selling fixed income ETFs accounted for 50% of the outflows. These outflows accounted for most of the fixed income outflows. A more diversified set of companies selling equities accounted for the other half of the outflows. The combined outflows over 2022 and 2023 has altered the profile of ETF holdings by insurers. In our ninth annual study of ETF usage by U.S. insurance general accounts, we review ETF usage across various types of companies and across different asset classes. We also analyze how trading patterns have varied over the years.

Holding Analysis

As of year-end 2023, U.S. insurers invested USD 34.4 billion in ETFs. This is a fraction of the USD 8.1 trillion in U.S. ETF AUM, as well as the USD 8.4 trillion in insurance general account assets. Exhibit 1 shows the use of ETFs by U.S. insurers over the past 20 years.