Blog — 9 Jul, 2021

How to use ESG Heat Maps in Credit Risk Analysis

This is the first blog in a new series about how to integrate ESG Heat Maps into Credit Risk Analysis.

Incorporating environmental, social and governance (ESG) factors in credit risk analysis is fast becoming an international best practice and is a mandatory requirement of the European Banking Authority (EBA) Guidelines on Loan Origination and Monitoring that came into effect on 30th June 2021. [1]

Despite this, credit, investment, and sustainability officers are still facing several challenges in their analysis, as often ESG data, methodologies and trained resources are limited when dealing with large loan and investment portfolios.

To reduce the complexities surrounding analysis, industry professionals rely on Sector and Country ESG Heat Maps as effective tools to identify investments and borrowers exposed, directly or indirectly, to increased risks associated with ESG factors.

Heat Maps are sector and/or countries rankings based on a wide range of ESG metrics.

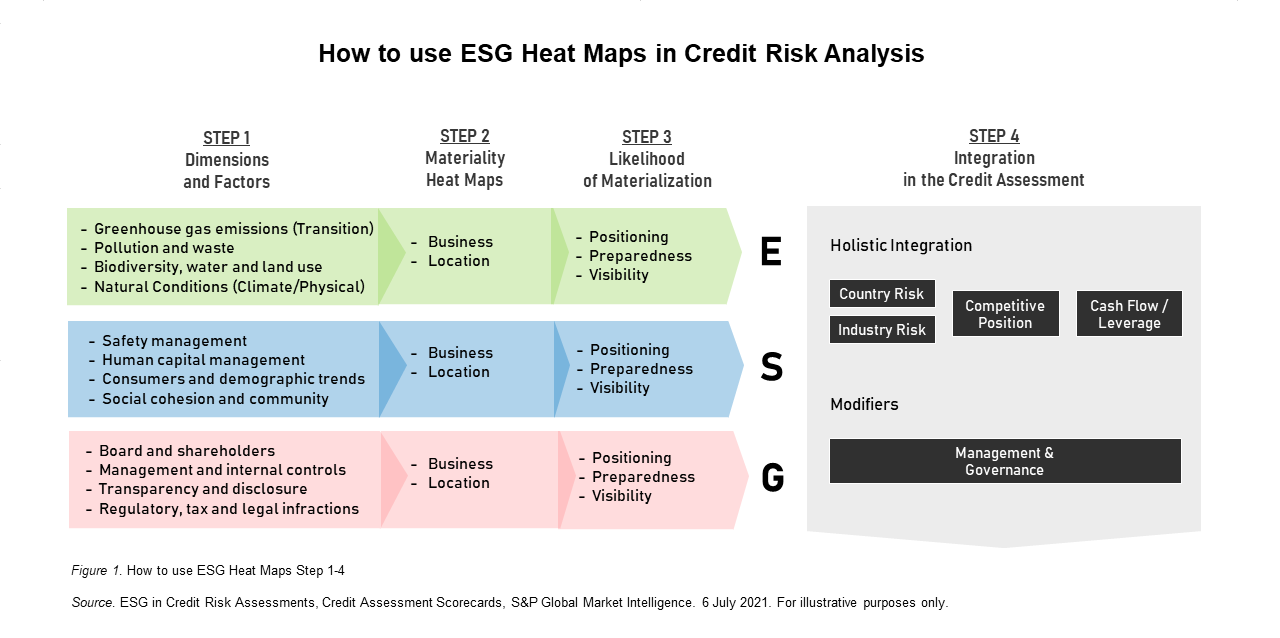

To help you create a transparent and structured approach for identifying ESG risks and opportunities, we have developed a 4-step framework for how to use ESG Heat Maps in Credit Risk Analysis.

Step 1: Define ESG Risk Dimensions and Factors

For each of the three ESG dimensions (i.e., environmental, social and governance), it is first necessary to define the relevant ESG credit risk factors, which can influence the capacity and willingness of an obligor to meet its financial commitments and that can have negative or positive credit impacts. For example, greenhouse gas emission, pollutions and waste or climate physical risk as key environmental credit risk factors. Please refer to our previous blog series, where we explored the three dimensions in detail.

Step 2: Assess Materiality of ESG Risks Using ESG Heat Maps

Next, it is necessary to assess the materiality of ESG risks each borrower is exposed to, directly and indirectly, using ESG Heat Maps. Material ESG risks are those that are likely to affect the financial condition or operating performance of a business. You can use ESG Heat Maps as effective analytical tools that quickly screen large portfolios and identify counterparties exposed to increased financial risks. These are risks which are associated with ESG factors and based on their business activity and geographic location. For example, a Heat Map will show if a business is in a region known for destructive hurricanes or wildfires or if it is exposed to significant transition risk due to increasing regulation.

Step 3: Assess Likelihood of ESG Risks to Materialize

Third, you will need to perform an in-depth and systematic analysis on each borrower, prioritizing the selected ones in order to determine the likelihood that ESG risks will materialize, reviewing: 1) each borrower’s business model and preparedness, and 2) the time-horizon ESG risks are expected to materialize (often long-term) versus the credit assessment time horizon (usually two to five years).

Step 4: Integrate ESG in Your Analysis

Finally, you need to reflect the relevant ESG risks and opportunities in the borrower’s credit assessment, coherently with the credit framework adopted. Our Corporate Credit Assessment Scorecards enable you to integrate ESG factors holistically in several areas of the analysis:

- Industry risk assessments: For regulatory requirements and supervision affecting an entire sector

- Competitive position: For changing consumer preferences and/or reputational damages, which may affect those issuers with environmentally or socially unfriendly business models

- Financials, forecasts, or other specific financial risk factors: For quantifiable ESG risks impacting cash flows and/or leverage

- Management and governance modifier: For poor planning, governance, and control practices, when not holistically reflected in other areas of the analysis

If you would like to know about our Scorecards or our approach to integrating ESG in credit assessments get in touch here.

[1] "Final Report – Guidelines on loan origination and monitoring", European Banking Authority, May 29th, 2020.

Theme

Location

Products & Offerings