Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Jun 22, 2018

Global and domestic market woes hit South African rand

South Africa followed in the footsteps of other emerging markets such as Turkey and Argentina by witnessing a 9.2% depreciation of the local currency's exchange rate against the US dollar over the 7 June to 19 June period, as positive emerging-market sentiment takes a breather. This pushed the South African rand lower to an average of ZAR13.88:USD1.0 by 19 June from ZAR12.70:USD1.0 a week ago. South Africa has witnessed the biggest sell-off of local bonds by foreign investors on record. Since the start of May, the daily average sell-off of local bonds increased to ZAR1.67 billion, leaving debt sales at a cumulative ZAR44.7 billion (USD3.3 billion or 7.7% of gold and foreign-reserve holdings) over the May-to-current-date period.

The South African economy followed in the footsteps of other emerging markets challenged by global and local sentiment changes. South Africa is facing structural growth impediments, lack of fiscal space to stimulate the economy as government debt holdings escalate, and a widening current-account deficit meaning heavy reliance on financing from volatile portfolio flows as foreign direct investment dwindles. Policy uncertainty in the South African economy, particularly regarding property rights, the independence of the South African Reserve Bank, the central bank, and looming strike action at embattled power producer Eskom, highlights the problematic political climate that limits the government's ability to impose fiscal discipline in a pre-election year. Eskom's wage bill continues to jeopardize the parastatal's financial health, and so it is not surprising that the power producer announced the cutting back of some pipeline infrastructure projects in the next few years to balance its books. The likelihood is high of the company not meeting striking workers' high wage demands and this could jeopardize uninterrupted electricity provision to the economy. South Africa's larger construction companies have also been under severe pressure since 2016. Basil Read, a large Johannesburg Stock Exchange-listed construction company, saw its share price collapse during the past week as the company applied for business rescue due to challenging domestic operational conditions, particularly regarding the issuing of state contracts.

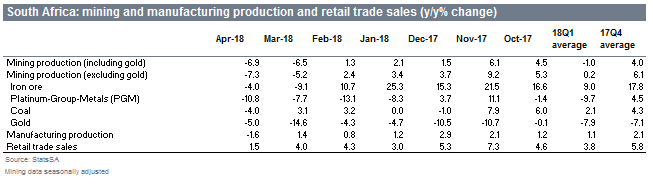

The recent weakness of the rand could leave South Africa's headline inflation close to the upper end of the 3-6% target range during 2018. Steep fuel price increases in the aftermath of a higher fuel levy, weaker currency, and higher oil prices could exert pressure on headline inflation, in our view. Furthermore, the higher petrol prices and a hike in the value-added tax rate to 15% in April are expected to leave consumer spending under pressure during the second quarter. in addition, policy uncertainty could delay pipeline private investment spending (including residential investment), especially if the land redistribution debate starts to heat up again in August, moving into 2019 ahead of the national elections.

Therefore, we deem the risk of a negative quarterly growth outcome during the second quarter as relatively high. Our forecast for the rand's exchange rate remains unchanged at ZAR13.20:USD1.0 by year-end. The global market environment remains supportive of South Africa's growth prospects, but the country has failed to take adequate advantage of stronger international trade flows since 2017. Nonetheless, the weaker currency could support overall export growth during the second half of 2018. We expect South Africa's GDP growth to average 1.4% this year. The weak growth backdrop will, in our view, leave the South African Reserve Bank's policy rate unchanged for the remainder of the year. Should the inflation outcome move beyond our current projections, a policy rate hike should not be ruled out.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-and-domestic-market-woes-hit-south-african-rand.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-and-domestic-market-woes-hit-south-african-rand.html&text=Global+and+domestic+market+woes+hit+South+African+rand+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-and-domestic-market-woes-hit-south-african-rand.html","enabled":true},{"name":"email","url":"?subject=Global and domestic market woes hit South African rand | S&P Global &body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-and-domestic-market-woes-hit-south-african-rand.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Global+and+domestic+market+woes+hit+South+African+rand+%7c+S%26P+Global+ http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-and-domestic-market-woes-hit-south-african-rand.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}