20 December 2024

2025 Auto Sales Forecast: 89.6M Vehicle Sales Worldwide

Article Summary

New global auto sales are expected to rise 1.7% year-over-year, to 89.6 million units, according to S&P Global Mobility’s 2025 auto sales forecast.

As 2025 approaches, S&P Global Mobility forecasts 89.6 million new vehicle sales worldwide next year, reflecting cautious recovery growth. 2025 automotive forecasts have been downgraded across the board, reflecting expected post-election US policy shifts. Resulting impacts to vehicle demand will be significant, especially interest rates, trade flows, sourcing, and BEV adoption rates.

Global new vehicle sales in 2025 are expected to rise 1.7% year-over-year, to 89.6 million units, according to a new forecast by S&P Global Mobility.

The global auto sector remains focused on managing production and inventory levels in response to regional demand patterns, which include slower growth in key markets, in some cases related to slower electric vehicle adoption rates.

The forecast outlook incorporates several factors, including improved supply, tariff impacts, still-high interest rates, affordability challenges, elevated new vehicle prices, uneven consumer confidence, energy price and supply concerns, risks in auto lending and the challenges of electrification. In the US, president-elect Donald Trump is expected to hit the ground running in 2025 with a range of policy priorities, including universal tariffs, deregulation, and wavering BEV support.

"2025 is shaping up to be ultra-challenging for the auto industry, as key regional demand factors limit demand potential and the new US administration adds fresh uncertainty from day one," said Colin Couchman, executive director of global light vehicle forecasting for S&P Global Mobility. "A key concern is how 'natural' EV demand fares as governments rethink policy support, especially incentives and subsidies, industrial policy, tariffs, and fast evolving OEM target setting."

2024 global vehicle sales are expected to reach 88.2 million units, according to S&P Global Mobility. This reflects a 1.7% increase from 2023, supported by ongoing inventory restocking throughout the year as supply chains become more stable.

Market-by-market vehicle sales forecasts

Europe: Wrapping up 2024, the Western/Central European market should deliver just under 15.0 million units (+1.1% y/y), as customers remain cautious, and OEMs continue to fine-tune their propulsion mix. Into 2025, this storyline will intensify as strict 2025 emission rules further influence the market mix and topline, S&P Global Mobility forecasts the market flatlining around 15 million units, up by just 0.1% y/y - reflecting economic recession risks, still-high car prices, tapering EV subsidies, EV tariffs, and political uncertainty in Germany and France.

"Key challenges include the dynamic electrification storyline, alongside EU tariffs on mainland Chinese imports, Trump tariff risks, hesitant consumers, a new EU Commission, and vigorous lobbying regarding EU emission targets," Couchman said.

United States: S&P Global Mobility projects US sales volumes to reach 16.2 million units in 2025, an estimated increase of 1.2% from the projected 2024 level of 16.0 million units and reflective of a still uncertain environment for auto sales levels.

"2025 brings with it mixed opportunities and uncertainty for the auto industry as a new administration and policy proposals take hold," said Chris Hopson, manager of North American light vehicle sales forecasting for S&P Global Mobility.

"New vehicle affordability issues that coalesced to constrain auto demand levels for much of 2024 will not be resolved quickly in 2025. Vehicle pricing levels are expected to decline but remain high; interest rates are expected to shift further downwards, but inflation levels are anticipated to remain sticky, and new vehicle inventory should also progress, but careful management is expected too. Combined with an uneasy consumer, we project this translates to mild growth prospects for auto sales."

Mainland China: For the year ending, the combination of the CNY130 billion extension of New Energy Vehicle (NEV) incentives, together with the new CNY75 billion trade-in scheme, 2024 is estimated to recover to at least 25.8 million units (+1.4% y/y), according to S&P Global Mobility. For 2025, despite below par economic activity, the automotive sector will continue to be supported by the NEV and trade-in schemes, along with local government auto incentives, wider government stimulus, and the continuation of the vehicle price wars. 2025 demand for Mainland China is forecasted at 26.6 million units, up a further 3.0% over 2024 levels.

The NEV boom is likely to extend into 2025 with electrified vehicle prices benefitting from cheaper battery costs together with generous national and regional subsidy programs to help stimulate new vehicle demand. Coupled with full NEV tax exemption through to the end of 2025, NEV penetration (as % of passenger vehicles) is projected to further increase to 58% in 2025, from 49% in 2024, according to S&P Global Mobility estimates.

Japan: Looking to 2025, Japanese light vehicle demand should be back in growth mode following a disappointing 2024, largely reflecting Daihatsu's unexpected halt in shipments due to emissions irregularities. S&P Global Mobility projects sales volumes to reach 4.6 million units in 2025, an estimated increase of 5.4% from the projected 2024 level below 4.4 million units. The prospect of US universal tariffs, and weaker global economic fundamentals, could prove problematic for Japan—a key net exporter of automobiles, especially to North America, although expected slower US BEV growth could offer a silver lining.

2025 vehicle production outlook stagnates as global risks intensify

Global light vehicle production in 2024 is expected to finish at 89.1 million units - a 1.6% deterioration compared to 2023 levels, with all regions except mainland China and South America experiencing decline.

The production outlook for 2025 is dominated by the assumption that the incoming US administration will levy a new wide-reaching tariff regime, effectively creating a universal tariff of 10% on all goods coming into the US except for Canada and Mexico where the terms of the USMCA are assumed and mainland China where it is assumed a tariff of 30% will be applied.

For 2025, S&P Global Mobility forecasts global light vehicle production levels to decline by 0.4%, to 88.7 million units. The tariff effects are difficult to isolate in each region especially considering the ongoing challenges of inventory management, and with continued volatility at the vehicle program level as OEMs make strategic adjustments to their future product plans.

"The auto industry continues to navigate uncertain terrain as we enter 2025, particularly as we anticipate President-elect Trump's incoming universal tariffs," said Mark Fulthorpe, executive director of global light vehicle forecasting for S&P Global Mobility. "During 2025, the production landscape will change dramatically, as global trade slows, and as retaliatory measures are likely to emerge."

In mainland China, S&P Global Mobility forecasts stable production levels for 2025, up 0.1%, at 29.6 million units. Output levels should be supported by a combination of heady NEV domestic demand, alongside robust exports, albeit tempered by EU import tariffs on Chinese-made BEVs.

For the North American region, overall 2025 production is set to fall back by 2.4%, to 15.1 million units. The incoming Trump administration will mark a return to the predictably unpredictable with policies that are expected to influence overall demand and challenge vehicle mix assumptions. On a brighter note, deregulation should create tailwinds for the North American auto industry later in President Trump's second term.

Europe is expected to build 16.6 million units in 2025, down 2.6% from an estimated 17.0 million in 2024. The outlook reflects propulsion mix fine tuning ready for the 2025 step change in EU emissions rules, alongside new tariff/trade assumptions associated with the incoming Trump administration, with premium vehicles particularly at risk.

Consumer uncertainty around electrification, especially speed bumps in Europe & US

Through 2024, a host of OEMs have been walking back ambitious electrification plans for the coming five to 15 years. A key concern is how "natural" EV demand fares, as governments fine-tune policy support, especially incentives and subsidies, EV industrial policy, and tariffs. Outside China, automakers face twin challenges in the electrification transition—scaling output of sellable BEVs and finding willing customers to buy them.

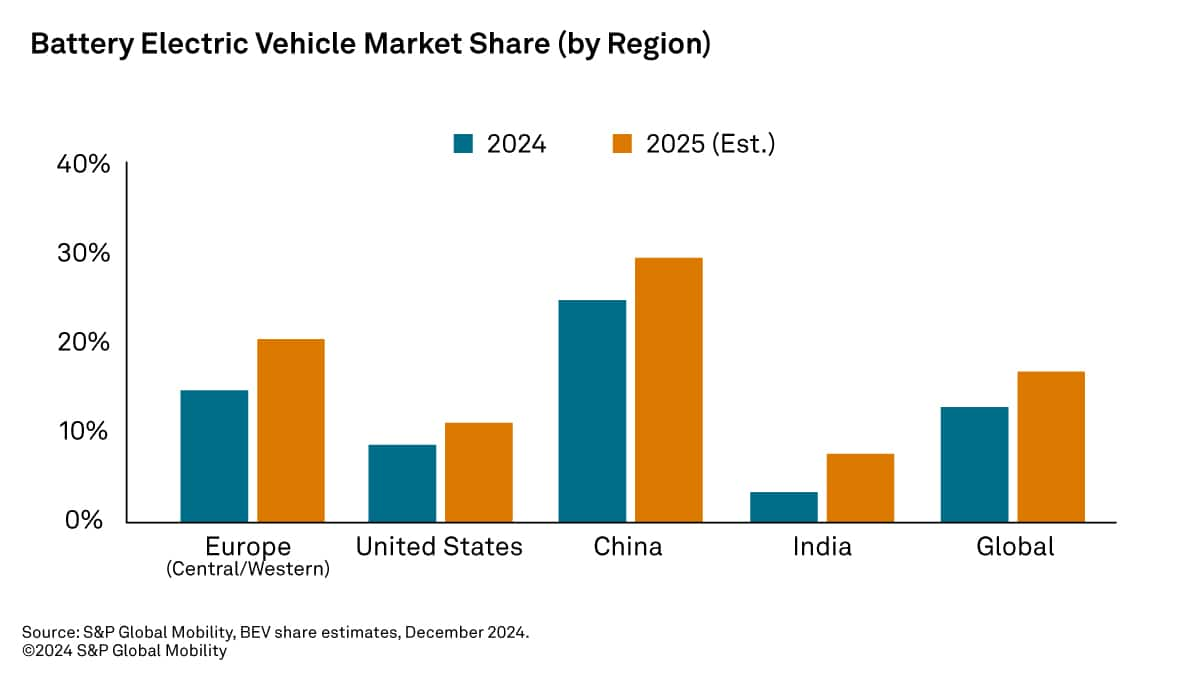

Despite the gloom, electric vehicles remain an important automotive growth sector, and S&P Global Mobility projects global sales for battery electric passenger vehicles to post 15.1 million units for 2025, up by 30% compared to 2024 levels, accounting for an estimated 16.7% of global light vehicle sales. For reference, 2024 posted an estimated 11.6 million BEVs globally, for 13.2% market share.

Major markets are forecast for most of this 2025 vehicle production outlook stagnates as global risks intensify, though smaller markets will also see modest increases. Forecasted BEV share by region is as follows:

Looking beyond 2025, many uncertainties persist regarding the pace of electrification, especially regarding charging infrastructure, grid power, battery supply chains, global sourcing trends, tariff trade barriers, the rate of technological advancements, and the necessary level of support from policymakers to facilitate the shift from fossil fuels to electric alternatives.

Currently, China's NEV program and Europe's "Fit for 55" initiative remain intact to support a sustainable mobility future. Less clear are President-elect Trump's intentions for US electric vehicle support, especially regarding the IRA and various policy initiatives.

S&P Global Mobility's light vehicle sales forecast covers 145+ and offers the most accurate, up-to-date data on global market trends, OEM performance, and segment growth. With expert insights and reliable projections, you can confidently plan for the future and maintain a competitive edge.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.