Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Jun 30, 2020

Daily Global Market Summary - 30 June 2020

Most APAC and all US equity markets closing higher today, with US equities reporting the best quarterly performance since 1998. Most European equity markets and oil closed modestly lower, while iTraxx and CDX IG/HY all ended the day tighter. Also noteworthy, is gold breaching $1,800 per ounce for the first time since 2011 and 5yr US government bonds coming close to breaching a new record low yield. As we enter the new quarter, all eyes are now focused on Thursday's US June non-farm payroll and weekly jobless claims reports.

Americas

- US equity markets closed higher, with another small surge (similar to yesterday) occurring shortly before the end of the trading session; Nasdaq +1.9%, S&P +1.5%, Russell 2000 +1.4%, and DJIA +0.9%. The Nasdaq ended the quarter at +31%, S&P 500 +20%, and DJIA +18%, which is the US equity market's best quarterly performance since Q4 1998.

- 10yr US govt bonds closed +3bps/0.65% yield. 5yr US govt bonds closed +2bps/0.29% yield, but earlier in the day came close to breaching the all-time intraday low yield of 0.26%.

- Gold futures closed at +1.1%/$1800 per ounce and were as high as $1,804 per ounce at 11:27am EST, breaching $1,800 for the first time since September 2011.

- CDX-NAIG closed -3bps/76bps and CDX-NAHY -20bps/516bps.

- Crude oil closed -1.1%/$39.27 per barrel.

- The US Conference Board Consumer Confidence Index jumped 12.2

points (14.2%) to 98.1 in June, remaining well beneath its

pre-pandemic level. With a survey cutoff date of 18 June, the

reading likely does not fully reflect renewed concerns around the

resurgence of the COVID-19 pandemic, which we expect to weigh on

economic growth and breed considerable uncertainty about the

outlook for some time. (IHS Markit Economists David Deull and James

Bohnaker)

- The present situation index advanced 17.8 points to 86.2, nearly twice the increase seen in the expectations index, which gained 8.4 points to 106.0.

- The expectations index has been stable during the pandemic and as of June was well above its 2019 average—a marked contrast from the Great Recession, when the index of expectations plunged by more than half and remained beneath its prior peak for years. This stability is a function of the speed of the current downturn and indicates that consumers expect a recovery to take hold more quickly than in the prior episode.

- The labor index (the percentage of respondents viewing jobs as plentiful minus the percentage viewing jobs as hard to get) improved, increasing 9.7 points to ‑3.0. It had registered 32.6 in February.

- The net percent of respondents expecting business conditions to improve in six months rose 5.3 percentage points to 27.3%, the highest since 1984. A net 24.2% expected employment conditions to improve, the most on record in data beginning in 1967. However, the net share of respondents expecting higher incomes inched up only 1.5 points to 0.7%.

- Purchasing plans were mixed in June. The share of respondents planning to buy autos in the next six months increased 0.4 percentage point to 11.7%, and the share planning to buy homes increased 0.5 point to 6.5%. The share planning to buy major appliances fell 1.0 point to 45.5%.

- Vacation plans within six months were still deeply depressed at 33.0% in June, having increased only 1.2 percentage points since April. The share planning to travel by airplane fell even further, to 15.7%.

- S&P CoreLogic Case-Shiller composites reported little

impact to price appreciation from COVID-19. Data in April were

again limited to only 19 cities as opposed to 20 under normal

circumstances. Data for Wayne County, Michigan, were unavailable

and as a result, there are no data for Detroit in this release.

(IHS Markit Economist Troy Walters)

- Both the 10-city and 20-city composite indices were up 0.3% month over month (m/m).

- Home prices were up month on month in 16 of the 19 cities reported. Increases ranged from 0.1% in Dallas and Washington DC to 1.3% in Cleveland. Prices fell in Seattle (down 0.1% m/m) and Portland (down 0.2% m/m) while San Francisco was flat.

- On an annual basis, home price growth was up slightly or steady in April. The 10-city index was up 3.4% year on year (y/y), unchanged from the previous month. The 20-city index was up 4.0% y/y, slightly faster than March.

- Prices in April were higher than one year earlier in all of the cities covered. Phoenix, accelerating to 8.8% y/y, remained the growth leader. Seattle remained in second place at 7.3% y/y. Minneapolis followed at 6.4%. Chicago remained the slowest-growing market at 1.4% y/y.

- Growth in the national index accelerated again in April, this time to 4.7% y/y.

- The level of corn and wheat on hand as of June 1 came in above

expectations, reflecting downturns in usage in the March-May

period, according to USDA's Grain Stocks report. (IHS Markit Food

and Agricultural Commodities' Roger Bernard)

- USDA said that 3.03 billion bushels were stored on farms, up 3% from year-ago, while off-farm stocks were at 2.20 billion bushels, down 2% from June 1, 2019. The figures reflected higher stocks compared with June 2019 in Iowa, Minnesota and Nebraska which more than offset the reductions in stocks in Illinois and Indiana. The implied disappearance for March-May was 2.73 billion bushels, marked a sharp reduction from 3.41 billion bushels used during the same quarter in 2019. That likely reflects in large part the sharp reduction in US ethanol production during that period.

- USDA said that 1.386 billion bushels of soybeans were present on June 1, down 22.3% from year ago, and just under expectations there would be 1.392 billion bushels on hand. On-farm stocks were at 633 million bushels, down 13.3% from year ago, while off-farm supplies were at 753 million bushels, down 28.5% from year ago. The implied disappearance for the March-May quarter was 869 million bushels, an 8% reduction from the year-ago quarter.

- The level of wheat stocks on June 1 totaled 1.044 billion bushels, down from 1.08 billion in 2019, but above expectations there would be 980 million bushels on hand. Farmers are holding more supplies than year ago, with on farm stocks of 232 million bushels, up 12.3% from June 1, 2019, while off-farm holdings were 812 million bushels, down 7% from year ago. Of the top five states, only Oklahoma reported smaller stocks on had compared with year ago. Implied disappearance for March-May was 372 million bushels, down a sharp 28% from the same period in 2019.

- Nikola opened the order books for its upcoming Badger electric pick-up truck on 29 June, taking USD5,000 refundable deposits. Nikola announced the Badger earlier this year (see United States: 12 February 2020: Nikola announces plans for electric pick-up truck). Nikola says it is accepting pre-orders for either the battery electric vehicle (BEV) version or the fuel-cell hydrogen electric vehicle (FCEV) version. The BEV version is expected to have a range of 300 miles and the FCEV version a range of 600 miles. In a statement, company founder and executive chairman Trevor Milton said, "The technology on the Badger is next to none; it has one of the most advanced powertrains and infotainment systems on the market. The features include over-the-air updates, keyless entry, independent torque control of every wheel, 906 HP, 980 ft. lbs. of torque, 15 kilowatt power export with 220V and 110V, tie-down tracks inside the truck for cargo, hidden refrigerator, up to 600 miles of range, and waterproof displays. You couldn't dream of building a better pickup truck than the Badger and we offer it in both fuel cell and battery-electric options." Nikola has previously announced that the Badger electric truck will be produced in partnership with another OEM. On 29 June, the company confirmed that it would announce the OEM deal prior to the Nikola World event to be held on 3-5 December 2020. (IHS Markit AutoIntelligence's Stephanie Brinley)

- Gilead Sciences (US) has announced the Wholesale Acquisition Cost (WAC) price of remdesivir, set at around USD3,200 for a five-day course of treatment (6.25 vials on average). Factoring in government discounts, US federal programs as well as other "developed countries" where remdesivir is authorized for use would be expected to pay USD2,340 for a five-day course of treatment (USD390 per vial). Gilead noted that this price ensures affordability for those developed countries "with the lowest purchasing power" and eliminates the need for country-by-country pricing negotiations. This price lies in-between the Institute for Clinical and Economic Review (ICER)'s two benchmarks: the traditional cost-effectiveness benchmark (USD4,580-5,080), and the cost-recovery price taking into account research and development (R&D) costs (USD1,010-1,600). (IHS Markit Life Science's Margaret Labban)

- Autonomous vehicle (AV) sensor maker Velodyne Lidar is reportedly in talks to go public through a reverse merger. Velodyne plans to merge with Graf Industrial, a blank-check company, helping the AV sensor maker to conduct an initial public offering (IPO), reports Bloomberg. Merging with a blank-check company has become a common way for companies to go public during the COVID-19 pandemic, which has battered automotive businesses. Graf Industrial raised USD225 million in an IPO in 2018. Velodyne is one of the pioneers of LiDAR solutions for advanced driver assistance systems (ADAS) and autonomous driving applications. LIDAR sensors are necessary for autonomous driving as they measure distance via pulses of laser light and generate 3D maps of the world around them. The company's technology is used by automakers including Mercedes-Benz AG and Ford Motor Company. Last year, there were reports that Velodyne had hired bankers for a potential IPO, seeking to surpass its last private valuation of USD1.8 billion. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Ford has announced the 'Ford Promise' program allowing customers to return a vehicle in the event of job loss within one year of purchase. Ford says that, under the Ford Promise program, customers who lose their job within one year of the purchase or lease of a vehicle and choose to return it to Ford will be covered for up to USD15,000 of the balance outstanding. Ford intends this amount to cover any value loss and encourage consumers to purchase a vehicle despite economic uncertainty. Ford says the enrolment period for the program runs through 30 September 2020. Ford is to run an advertising campaign to raise awareness of the program. In a statement, Ford US marketing, sales and service head Mark LaNeve said, "We feel like right now, the economy is at the stage of recovery where people want things to be back to normal, they want to buy, but they're still a little nervous about what the future holds. We want them to know we understand that, and we're here to support them in their buying decisions." To qualify for the program, a customer must lease or purchase a vehicle through Ford Credit, which will reduce the customer's outstanding balance based on the average trade-in value set by the National Automobile Dealers' Association, and waive an additional USD15,000. (IHS Markit AutoIntelligence's Stephanie Brinley)

- Canada's real GDP by industry output decreased 11.6% month on

month (m/m) in April, an all-time low pace as output across all

industries was lower and near the 11.0% Statistics Canada flash

estimate. (IHS Markit Economist Arlene Kish)

- This time, output in the goods-producing industries (down 17.0% m/m) declined at a much faster pace than that in the services-producing industry (down 9.7% m/m).

- Industrial production output plunged 16.1% m/m, as manufacturing retreated 22.5% m/m.

- The real GDP by industry output decline in March was revised down 0.3 percentage point to -7.5% m/m.

- April was the first full month measuring the negative impact of the coronavirus disease 2019 (COVID-19) virus and likely marks the bottom as reopening plans began in May. The expected second-quarter real GDP decline will be significant, falling over 30% quarter on quarter, annualized.

- Paraguay's GDP growth of 3.5% year on year (y/y) in the first quarter of 2020 was on a low base of comparison, as the economy contracted by 2.7% y/y in the corresponding quarter of 2019. The key supporters of growth in the first quarter of 2020 were agriculture, thanks to a solid rebound in soybean production, and construction due to the completion of public-works projects and good weather. (IHS Markit Economist Ellie Vorhaben)

- Private consumption, investment, and government spending supported the economy. Net exports were a drag on growth - despite solid soybean production, weak prices and demand undermined export revenue.

- On 29 June, the government updated its Economic Reactivation Plan by increasing planned spending to USD2.5 billion, or 7% of GDP (previous fiscal stimulus measures amounted to 4% of GDP). Of this spending, USD2.15 billion will be raised through reallocations from different parts of the budget, while USD350 million in new debt will be issued.

- The plan includes up to four payments of PYG500,000 (about USD74) for those who are unemployed between August and December 2020.

- The soybean crop is expected to grow to 10.5 million tons in 2020, compared with 8.5 million tons in 2019. Countering this positive growth forecast are lower prices, which are set to fall by 4.3% on average in 2020; additionally, demand from key trading partners will be weaker as the region falls into recession.

Europe/Middle East/ Africa

- European equity markets closed lower except for Germany +0.6%; UK -0.9%, Spain -0.6%, Italy -0.4%, and France -0.2%.

- Most 10yr European government bonds closed lower except for Italy -4bps; Germany +2bps and Spain/France/UK +1bp.

- iTraxx-Europe closed -4bps/67bps and iTraxx-Xover -14bps/383bps.

- Brent crude closed -1.4%/$41.27 per barrel.

- Authorities in Denmark recently ordered a cull of mink after outbreaks of the COVID-19 virus on two farms. The Ministry of Environment and Food of Denmark first alerted the OIE to a SARS-CoV-2 outbreak on a mink farm in Northern Jutland on June 17. This marked the country's first confirmed case of virus infection in animals. Animals on the farm had no symptoms and there was no report of increased mortality. Samples were taken from the animals because the Danish Veterinary and Food Administration had been informed about a person with contact to the farm who had tested positive for COVID-19. Mink at another farm in the same region also later tested positive. These outbreaks have led to precautionary culls of the animals and the launch of a new screening program. The screening program will apply to 120 mink herds across the country. It will aim to determine whether initial findings were isolated cases or whether there has been widespread infection among mink herds. (IHS Markit Animal Health's Sian Lazell)

- The headline rate of HICP inflation in the eurozone edged up

from 0.1% to 0.3% in June according to Eurostat's flash estimate,

the first acceleration in five months. This is in line with the

signals from member states' data that have been released in the

past few days. (IHS Markit Economist Ken Wattret)

- The first rise in the inflation rate for energy since January was the main reason for the pick-up (see table and first chart below), primarily reflecting the rise in oil prices since late April. Energy inflation remained deeply negative nonetheless (-9.4%), keeping the overall inflation rate well below the ECB's below but close to 2% objective.

- While the inflation rate for unprocessed food moderated for the second straight month in June, it remained relatively elevated at 5.9%.

- The inflation rate excluding food, energy, alcohol and tobacco prices weakened again in June, slipping from 0.9% to 0.8%, its lowest level since May 2019 and uncomfortably close to its record low of 0.6% recorded in early 2015 when the ECB was compelled to launch its Asset Purchase Programme.

- Notably, services inflation decelerated again, to 1.2%, well down on the recent peak of 1.9% in November 2019, while non-energy goods inflation was flat at just 0.2%.

- According to the United Kingdom's Office for National

Statistic's (ONS) second estimate, the UK economy shrunk by 2.2%

quarter on quarter (q/q) in the first quarter, the sharpest decline

since the third quarter of 1979. This was a downward revision of

0.2 percentage point from the first estimate. (IHS Markit Economist

Raj Badiani)

- In addition, real GDP contracted by 1.7% year on year (y/y) in the first quarter, the biggest fall since the end of 2009.

- Consumer spending bore the brunt of squeezed activity during the first quarter, falling by 2.9% q/q, revised down from the initially reported 1.7% q/q drop.

- The drop in consumer spending was catastrophic since the fully-enforced lockdown was in place for only seven working days during the first quarter.

- The ONS reported large falls in spending on transport, restaurants and hotels, and clothing and footwear.

- However, there were pockets of improved demand, namely for food and drink, alcohol and tobacco, and televisions and audio-visual equipment.

- Households' saving ratio increased to 8.6% in the first quarter of 2020, a significant step-up from 6.6% at end-2019.

- Fixed capital formation fell for a second successive quarter, declining by 1.1% q/q in the first quarter because of weaker investment in dwellings as well as government investment.

- Business investment fell by 0.3% q/q in the first quarter, gaining some initial traction from the decisive general election outcome in December 2019 before being pushed back by the COVID-19-virus crisis "halting investment plans and retaining cash buffers, in particular in retail, leisure, travel and hospitality".

- Service-sector output in the first quarter posted its sharpest quarterly fall on record (see table below). Meanwhile, production output also tumbled, in line with shrinking manufacturing activity. Construction output was badly affected by the imposition of the anti-contagion measures, resulting in a very sharp drop in March.

- More worryingly, the ONS reports deeper GDP losses in April (published on 12 June) after the emergency quarantine and social-distancing measures were in place for the whole month to tackle the COVID-19-virus outbreak. The ONS reports that real GDP fell by 20.4% month on month (m/m) in April, the largest drop since the monthly series began in 1997 after falls of 5.8% m/m in March and 0.2% m/m in February. In annual terms, the economy in April was 24.4% smaller compared with a year earlier.

- Consumption of goods in France jumped by 36.6% month on month

(m/m) in May, according to figures published by the National

Institute of Statistics and Economic Studies (Institut national de

la statistique et des études économiques: INSEE). May's rebound

follows declines of 16.0% m/m in March and 19.1% m/m in April. (IHS

Markit Economist Diego Iscaro)

- Households' consumption of goods remains 7.2% below its pre-coronavirus disease 2019 (COVID-19) virus level in February. On a year-on-year (y/y) basis, it still declined by 8.3% in May.

- The m/m rebound in May was boosted by consumption of items that had been particularly hit during March and April, when a strict lockdown was in place (the restrictions started to be relaxed on 11 May).

- Consumption of durables rose by 162.1% (following falls of 43.8% in March and 44.9% in April), driven by higher sales of transport equipment (+219.1% m/m; after declines of 52.1% m/m and 51.0% m/m) and household durables (+138.8% m/m; following falls of -31.7% m/m and -38.7% m/m).

- Energy production, which fell by 11.3% in March and by 24.3% m/m in April, also rebounded by 27.6% m/m. Consumption of food products rose by 0.6% m/m in May, which was boosted during the lockdown as restaurants remained closed for dine-in customers until early June.

- With the exception of food and household durables, consumptions of all other goods remained well below their February levels

- French global automotive supplier Faurecia has warned that its sales in the second quarter will fall by around half as a result of the impact of the COVID-19 virus. According to a statement, its chief executive Patrick Koller made the announcement at the supplier's annual shareholders meeting held yesterday (29 June). He noted that the low point was April, stating that it was "a month severely affected by the lockdowns in Europe and North America, at a time when China was only just beginning its recovery." Along with the 19.7% year-on-year (y/y) decline in sales suffered in the first quarter at constant scope and currency, it now forecasts that sales in the six-month period could fall by around 35% y/y. (IHS Markit AutoIntelligence's Ian Fletcher)

- In South Africa's supplementary budget delivered on 24 June,

Finance Minister Tito Mboweni announced plans to cut public

spending in fiscal year 2020/21 by more than USD13.2 billion. This

is in addition to a USD14.9 billion cut announced in February, of

which USD9.1 billion is to come from reduced public-sector wages in

2020-22. Although no strikes are currently ongoing due to the

country's COVID-19 lockdown restrictions, the easing of

restrictions on social gatherings, together with existing wage

grievances between government and unions, will raise the likelihood

of strikes. (IHS Markit Country Risk's Langelihle Malimela)

- IHS Markit expects South Africa's GDP to decline by 8% in 2020, significantly lowering government revenues and likely resulting in increased borrowing. This places further pressure on government to lower the public-sector wage bill, which makes up a third of the state's expenditure.

- The spending cuts increase the likelihood of widespread protests across the public sector from July 2020. The current three-year public-sector wage agreement expires at the end of March 2021 and unions are likely to call for protests to pressure government to agree to an above-inflation increase commencing in April 2021.

- Although strikes are likely to be peaceful, some members of communities with reduced food supply due to the impact of the COVID-19-pandemic restrictions are likely to seek to take advantage of the strikes and engage in isolated looting of local supermarkets.

- The government's planned borrowing of USD7 billion is likely to be channeled towards its COVID-19 response, further raising concern among public-sector workers and unions that funds will not be available for salaries.

- BMW has announced it has opened the Additive Manufacturing Campus on the outskirts of Munich, according to a company statement. The new center brings together production of prototypes and series parts in one location, along with research into new 3D printing technologies, and associate training for the global rollout of toolless production. Investment in the campus, which will specialize in manufacturing components with the latest technologies as well as researching new manufacturing techniques, has come in at EUR15 million. A major focus of the Additive Manufacturing Campus will be research into scaling 3D printing production techniques. BMW is looking to use the technology to streamline component production for series development while also benefiting from improvements in R&D lead times. (IHS Markit AutoIntelligence's Tim Urquhart)

- The Austrian government will join the French and German administrations in Europe in offering incentive programs to promote the purchase of electric vehicles (EVs) as a stimulus package to help with economic recovery in the wake of the COVID-19 virus outbreak. According to a Reuters report, Economy Minister Leonore Gewessler said in a news conference that the government would offer EUR5,000 towards the purchase of an EV. (IHS Markit AutoIntelligence's Tim Urquhart)

Asia-Pacific

- Most APAC equity markets closed higher except for India -0.1%; Australia +1.4%, Japan +1.3%, China +0.8%, South Korea +0.7%, and Hong Kong +0.5%.

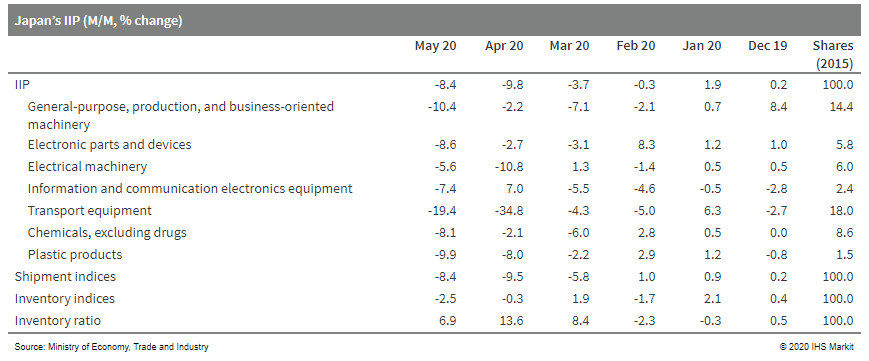

- Japan's Index of Industrial Production (IIP) fell by 8.4% month on month (m/m) in May following a 9.8% m/m decline in April. (IHS Markit Economist Harumi Taguchi)

- While manufacturers' shipments also fell by 8.4% m/m, continued sizeable drops in production contributed to a second straight month of decrease in inventory (down 2.5% m/m); however, the historical low level of shipments boosted the index of inventory ratio (up 6.9% m/m), breaking the highest level recorded in May.

- Although a major factor behind the fourth consecutive monthly contraction in production remained a sizeable decline in the production of autos (down 23.1% m/m), the negative effects of containment measures in Japan and the country's trade partners suppressed production deeply in a broader range of industry groupings, particularly for auto-related production (iron and steel, rubber products, and general-purpose machinery) and information technology-related production (semiconductor production machinery, electronic parts and devices, and information and communication electronic equipment).

- The fall in inventory largely reflected destocking in autos, iron and steel, and production machinery, but the inventory ratio increased in a broad range of industry groupings because demand remained weak.

- The May results were weaker than what IHS Markit had expected,

suggesting a steeper contraction of real GDP growth in the second

quarter of 2020 than current forecasts.

- Japan's unemployment rate increased to 2.9% in May 2020 from

2.6% in April 2020, reaching the highest level since May 2017. (IHS

Markit Economist Harumi Taguchi)

- The rising unemployment rate reflected continued severe business conditions, particularly for workers in accommodations and drinking and eating services, wholesale and retail stores, and life-related services and amusement, despite reopenings following the lifting of a state of emergency in late May. While lower employment figures for non-regular workers were the major factor behind a rise in the unemployment rate, the number of regular workers employed declined by 10,000 from a year earlier for the first fall in eight months.

- The severe business conditions also lowered the ratio of active job openings to active job applications to 1.20 in May from 1.32 in April, reflecting a continued decrease in effective job openings (down 8.6% month on month [m/m]), while effective job applications rose by 0.7% m/m.

- Although the ratio of new openings to new applications improved to 1.88 in May 2020 from 1.85 in April 2020, new openings fell by 32.1% year on year (y/y), which is the sharpest decline since May 2009, largely driven by decreases in accommodation and drinking and eating services, life-related services and amusement, manufacturing, wholesale and retail, and other services.

- Although the slight improvement in the ratio of new openings to new applications could be an early sign of a bottom for the contraction of labor demand, labor conditions are likely to remain sluggish, reflecting the gradual easing of containment measures and social distancing guidelines.

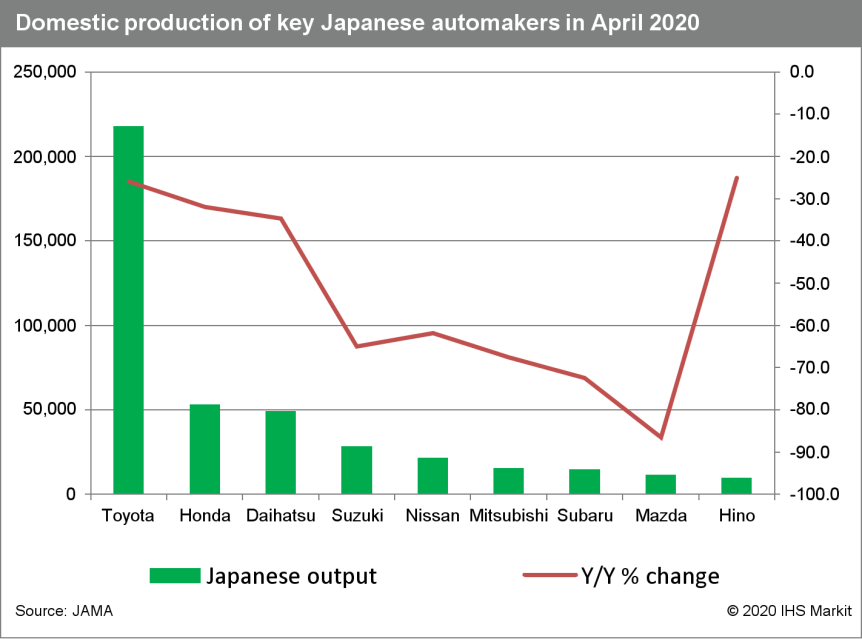

- According to figures released by the Japan Automobile Manufacturers Association (JAMA) today (30 June), Japanese vehicle production experienced a sharp decline of 46.2% year on year (y/y) to 438,770 units during April mainly because the COVID-19 virus outbreak affected automakers' production operations. (IHS Markit AutoIntelligence's Isha Sharma)

- Output in the passenger car category reached 359,403 units during the month, down by 48.6% y/y.

- Within the passenger car category, production of standard cars with an engine displacement of more than 2.0-litres was down by 54.7% y/y to 203,374 units during the month, while output of small vehicles was down by 24% y/y to 94,760 units.

- Production of mini-vehicles, categorized as vehicles equipped with engines smaller than 660cc, was down by 51.3% y/y to 61,269 units.

- Similar declines were witnessed in the truck and bus segments, falling by 32.4% y/y to 70,985 units and by 16.8% y/y to 8,382 units, respectively.

- In January-April, Japanese vehicle production declined by 17% y/y to nearly 2.8 million units.

- Output in the passenger car category reached 2.4 million units during this period, down by 17.2% y/y, while truck production declined by 16.4% y/y to 359,726 units and bus output by 7.3% y/y to 34,857 units.

- According to IHS Markit's forecasts, Japanese light-vehicle

output is expected to decline by 22.3% y/y to 7.159 million units

in 2020. However, we expect production volumes in 2021 to recover

by 9.3% y/y to 7.828 million units.

- Toyota began construction of a manufacturing plant in Tianjin, northeast China, with joint-venture (JV) partner FAW Group on 29 June. The new plant will be dedicated to the production of new energy vehicles (NEVs) and related components, such as electric-vehicle batteries. The plant project, which involves an investment of CNY8.5 billion (USD1.20 billion), is due to be completed by June 2022. In addition, under its partnership with GAC Motor, Toyota is building a new vehicle assembly line in Guangdong province, southeast China. Construction is due to be completed during the fourth quarter of 2020, with vehicle production scheduled to start in March 2021. Local media reports indicate that the new expansion project will allow Toyota to speed up its introduction of electric vehicles (EVs) in the Chinese market. The first models due to be produced by the GAC Toyota JV include a mid-size electric sport utility vehicle (SUV) and an electric multipurpose vehicle (MPV). The two new expansion projects will boost the Japanese automaker's production capacity in China by 400,000 units per annum. Much of the added capacity will be used to ramp up production of the automaker's upcoming battery EVs in China. (IHS Markit AutoIntelligence's Abby Chun Tu)

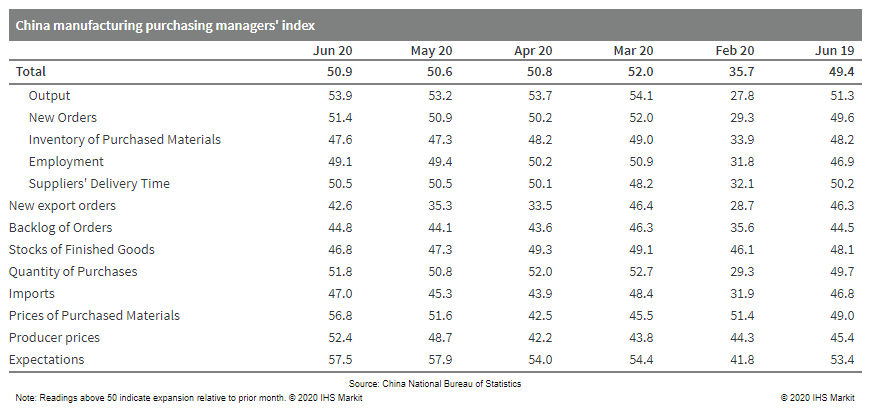

- China's official manufacturing purchasing managers' index (PMI) came in at 50.9 in May, up 0.3 point from April and the fourth consecutive month above the 50 expansionary threshold since the pandemic outbreak. (IHS Markit Economist Yating Xu)

- Production sub-index rose by 0.7 point to 53.9, significantly above the three-year average figure in June.

- New orders increased for the second consecutive month to 51.4 in June.

- Prices rose significantly in June due to the price rise in the upstream petroleum, steel and non-ferrous metals manufacturing, input prices expanded further and output prices improved to expansion for the first time since May 2019.

- Sub-index of new export orders and imports continued to improve with weak recovery in global economy over the past month, while they remained in deep contraction and far below the three-year average in June.

- Employment sentiment worsened further.

- PMI expanded in 14 out of the 21 surveyed manufacturing sectors. Medical, non-ferrous metals, communication equipment and electric equipment machinery reported strong recovery in new orders and production.

- Improvement in exports was concentrated in petroleum, communication equipment and electric equipment while auto, chemical and petroleum processing drove the recovery in imports. However, PMI for low-end trade-related manufacturing, such as textile, clothing and timber remained in contraction.

- Manufacturing PMI showed continuous recovery in different scale of enterprises, except deterioration in small firms with its PMI declined by 1.9 points from May to 48.9 in June.

- China's non-manufacturing PMI rose by 0.8 point to 54.4 in June, with acceleration in services and slowdown in construction.

- Construction PMI declined by 1 point to 59.8, but it remained above the figure a year ago and expectation sub-index rose by 0.3 point from May.

- Service PMI picked up by 1.1 points to 53.4. Among the 21 surveyed service sectors, 15 sectors reported PMI above 50 with faster expansion in transportation, information and software and finance. Particularly, production services PMI rose by 4.5 points. However, household services and culture and entertainment remained in contraction.

- The composite output PMI, covering both manufacturing and

non-manufacturing sectors, came in at 54.2, up 0.8 point from the

previous reading.

- Mainland China's National Development and Reform Commission

(NDRC) and the Ministry of Commerce (MOC) jointly published the

2020 negative list for foreign investment on 24 June, continuing

the efforts of further opening up domestic market and improving

business environment to stabilize foreign investment. (IHS Markit

Economist Lei Yi)

- The newly updated list, effective 23 July, reduces number of restricted areas for foreign investment to 33, from 40 in the 2019 version. This is the third revision since the nation adopted the practice; 63 areas were listed as off-limits for foreign investors in the initial 2017 version.

- All three financial sector related items in the 2019 list were removed, lifting existing caps on foreign ownership of securities, securities investment fund management, futures, and life insurance companies. Note that such a move was originally scheduled in 2021 according to the 2019 list, but was accelerated in accordance with the "phase one" US-China trade deal.

- Other sectors that have eased entry restrictions include agriculture, manufacturing, infrastructure, and transportation. Foreign investors are now allowed to control up to 66% ownership in wheat breeding and seed production, to participate in construction and operation of water supply and drainage networks of large cities, and to invest in air traffic control system, radioactive mineral processing, and nuclear fuel production. Foreign ownership limits in commercial vehicle enterprises will also be removed as scheduled.

- Continuing the regular updates of negative list despite the ongoing pandemic demonstrates the nation's determination in pushing for more market-friendly reforms, which helps maintain its long-term attractiveness for foreign investment.

- Further opening-up measures in the services sector are expected, especially for "high-end services" featuring high-tech, skilled labor, and high value-add.

- Mainland China's tourism sector continued its gradual recovery

during the three-day Dragon Boat Festival, which lasted from 25 to

27 June. According to the Ministry of Culture and Tourism, number

of tourists reached 48.8 million, and tourism revenue totaled

CNY12.3 billion, which represented contraction of 49% y/y and 69%

y/y, respectively. (IHS Markit Economist Lei Yi)

- Still, this has shown notable improvement from the three-day Tomb Sweeping Day holiday in early April, during which tourist numbers nationwide were down 61% y/y with tourism revenue 81% lower than in 2019. The situation during the Labor Day holiday was better, with tourists and revenues only down 41% y/y and 60% y/y, respectively; yet this could partially attribute to the fact that the holiday got extended by one day to five days in 2020.

- Data from China Tourism Academy showed that, over 30% of tourists shortened their travel distance and more than 50% intended to reduce travel budget during the Dragon Boat Festival. Only 5.6% of tourists chose to travel by train or by air.

- Electric vehicle (EV) startup Byton is suspending operations globally on 1 July for six months, according to media reports, citing a company spokesperson. Byton has built a factory in China and has produced a handful of vehicles to obtain necessary approval for production, but no definite start date for sales has been set amid the COVID-19 pandemic. US news outlet The Detroit Bureau reports the Byton spokesperson as saying, "Without a revenue stream, we just hit the wall." In addition, China Tech News recently reported that Byton sent an email to its US employees notifying them that the company would implement lay-offs in the United States before 30 June. The report added that the company's US office would retain research-and-development (R&D)-related intellectual property and operational positions. Byton has not issued a formal statement. Although Byton has been moving forward with launch plans, it furloughed 450 workers in the US in April. (IHS Markit AutoIntelligence's Stephanie Brinley)

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-01-july-2020.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-01-july-2020.html&text=Daily+Global+Market+Summary+-+30+June+2020+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-01-july-2020.html","enabled":true},{"name":"email","url":"?subject=Daily Global Market Summary - 30 June 2020 | S&P Global &body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-01-july-2020.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Daily+Global+Market+Summary+-+30+June+2020+%7c+S%26P+Global+ http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-01-july-2020.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}