Blog — 22 Jul, 2021

Fund Financing Through a Credit Lens Credit Risk Factors for Alternative Investment Funds AIFs

By Suming Xue

This is the second blog in a three-part series on AIFs. These funds provide an option to invest in different asset classes − such as hedge funds (HFs) and private equity (PE) − primarily for Limited Partners (LPs) that are typically large pension funds, insurance companies, and family offices. In the first blog, Fund Financing Through a Credit Lens: Understanding the Basics of AIFs, we looked at how fund financing works and a number of critical factors to consider when assessing AIF exposure. We now look further at some of the potential risks with AIFs and available tools to evaluate their creditworthiness.

Key questions when assessing an AIF’s creditworthiness

Identifying an AIF’s potential credit risks may be challenging, and a series of questions should be addressed to help better understand the financial strengths and weaknesses.

- Could the AIF see a steep loss in value in the event of adverse economic situations? The value of the assets could be reduced due to unfavorable market conditions, which would impair the credit quality of the fund.

- How stable is the AIF’s source of funding and the investor capital base? The stability of the investor capital base is driven by a combination of three factors: permanence of capital, diversity, and the strength of equity investors. Permanent capital without redemption rights from a diverse base of highly-rated LPs represents a positive situation. As such, capital would likely be readily available to absorb any losses.

- Does the AIF have liquidity to service its debts and meet any other obligations? The fund’s liquidity is measured by its liquidity needs versus the potential sources of liquidity. An AIF with mixed assets that are strong and marketable and of different maturities should offer the fund the ability to quickly dispose of assets in times of stress without a significant discount.

- Could additional risks arise from the countries in which the AIF operates? Any geopolitical concerns could hamper a fund’s creditworthiness.

- Does the AIF have a good track record on performance? A fund needs sufficient cash flows to cover its financial commitments. A fund that has exhibited strong profitability and an extensive track record is likely to be able to weather turbulent market conditions.

S&P Global Market Intelligence’s AIF Credit Assessment Scorecard is constructed to assist in analysing the specific risk factors relevant to AIFs. This includes such factors as concentration, market risk, funding and liquidity risk, and country-level issues. In addition, a good understanding of an AIF's investment performance track record, its internal governance and risk management practices, and the regulatory environment in markets in which it operates can further refine the analysis.

An example of recovery prospects with subscription credit facilities

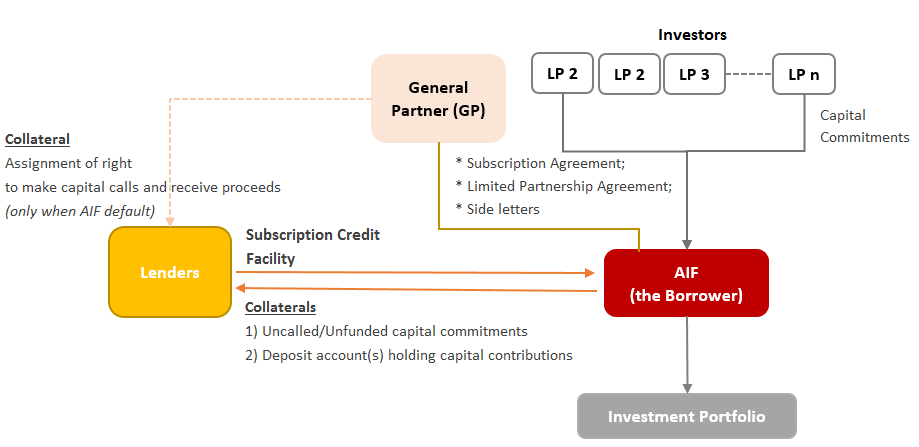

Historically, subscription credit facilities (capital call facilities) have been used for short-term bridge financing, secured against investors’ committed capital (see Figure 1 for an illustration of a facility structure). According to Preqin, in the past decade, the proportion of funds using subscription credit facilities peaked at 53% for vintage 2016 funds, more than double pre-financial crises 2007-2008 levels.[1] This expansion of subscription credit facilities can be attributed to the fact that these facilities lend against the LP’s uncalled capital commitment,[2] rather than the investments held by the fund. This has the benefit of improving liquidity and operating efficiency, and enhancing competitiveness in investment bidding and cash flow management.

Figure 1: Simple Version of the Structure of a Subscription Credit Facility

Source: S&P Global Market Intelligence. For illustrative purposes only.

Typically, the primary source of repayment for a subscription credit facility is from the unfunded capital commitment of the eligible LPs.[3] Increased pressure due to COVID-19 has made many lenders (both private lenders, as well as financial institutions) ponder what the impact would be if an AIF fails to repay a subscription credit facility, or if LPs are not in a position to pay and/or the amount called from the LPs is a significant amount of an LP’s total commitment.[4]

To address this concern, S&P Global Market Intelligence’s Capital Call Facility Loss-Given Default (LGD) model is designed to identify key aspects that one should consider to assess such potential losses. This includes the creditworthiness of eligible LPs and their total committed, as well as unfunded, capital and their previous loss experience.

As mentioned earlier, identifying an AIF’s potential credit risks may be challenging, and there are a number of questions that should be considered. Taking these questions into account, S&P Global Market Intelligence’s AIF Credit Assessment Scorecard helps assess the likelihood that an AIF will default, and the Capital Call Facility LGD model provides an indication of the potential loss in the event of default. Together they provide lenders with a holistic view of credit risk.

[1] “Subscription Credit Facilities”, Preqin Special Report, June 2019.

[2] Uncalled capital commitment is the portion of an investor’s capital commitment that is unfunded and may be subject to a capital call, excluding any amounts subject to a pending capital call that have not yet been funded as a capital contribution.

[3] Eligible LPs are those that meet the criteria lenders set in the subscription credit facility agreement, for example, having an acceptable credit rating.

[4] There has been only one known institutional default, i.e., Abraaj Group liquidation case in 2018/19. Although there is an elevated concern at the systemic risks given the sizeable exposure to such facilities and the recent influx of new providers entering the subscription lending market from Europe, the U.S., and Asia, there is no anecdotal evidence suggesting that any AIFs failed to repay subscription credit facilities. The purpose of the article is to suggest a tool for estimating the LGD for subscription line facilities in the case of an AIF default, if and when one happens.

Theme

Location

Products & Offerings