Research — April 03, 2025

Energy utility capex predicted to top $1 trillion from 2025 through 2029

The nation's electric, gas and water utilities are directing substantial investments into infrastructure enhancements aimed at modernizing mature generation, transmission and distribution networks, and meeting new demand. These initiatives include the construction of new natural gas, nuclear, solar and wind power generation facilities, alongside the integration of advanced technologies such as smart meters, smart grid systems, cybersecurity protocols, electric vehicles and battery storage solutions. This significant capital outlay is anticipated to augment profit growth within the utility sector for the foreseeable future.

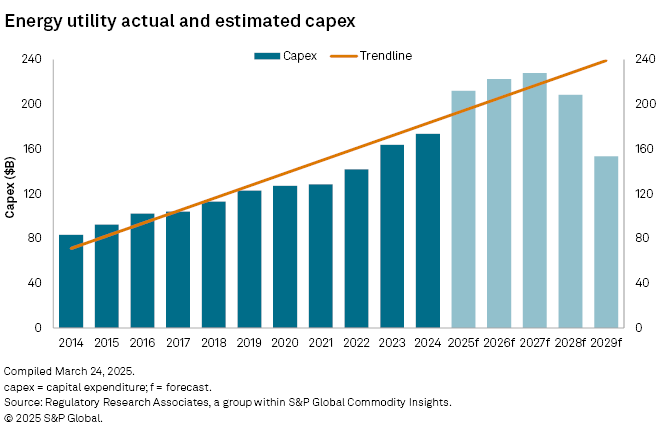

➤ Projected capital expenditures for 2025 among the 47 energy utilities in Regulatory Research Associates' representative sample of publicly traded, US-based utilities are forecast to reach over $212 billion. This represents a 22% increase from the $173 billion spent in 2024, a 29% increase compared with the nearly $164 billion spent in 2023, and a nearly 50% hike compared to the $146 billion invested in 2022.

➤ Aggregate energy utility investments are projected to hit new highs of $222 billion in 2026, $228 billion in 2027 and $208 billion in 2028. These increases are predominantly propelled by federal legislation passed in 2021 and 2022 that supports infrastructure investment, state-level energy transition plans and incentives, and a strong surge in demand from datacenters amid the continuing expansion of AI and cloud computing technologies.

➤ Within the smaller investor-owned water utility sector, total capex is projected to grow approximately 15% in 2025 to $6.2 billion, from $5.4 billion in 2024. This continues double-digit growth rates of 11% posted in 2023 and 13% in 2022.

➤ While the aggregate energy capex forecast for 2029 drops to $153 billion, the level is rather likely to rise significantly over time as utility companies solidify their future project plans throughout the remainder of 2025 and in the years ahead.

Several factors are anticipated to drive an increase in utility capex over the coming years. The pressing need to replace aging infrastructure is already catalyzing considerable investment. Concurrently, state-level renewable portfolio standards are escalating, necessitating substantial expansions in low-carbon energy generation capabilities. Further bolstering these dynamics are federal infrastructure investment initiatives, notably the Inflation Reduction Act of 2022 (IRA), which aims to transition the US power generation landscape predominantly to zero-carbon sources by 2035.

Energy utilities are ramping up infrastructure investments in 2025, 2026 and 2027

Despite potential uncertainties stemming from the new US administration regarding investments supported by the IRA, the financial frameworks underpinning these initiatives are generally expected to withstand administrative changes. Many of the subsidies are structured as tax credits, effectively functioning as tax reductions, thereby providing significant insulation from shifts in congressional or executive control. While the Trump administration may desire to revise some IRA-related renewable investment credits, multiple Republican lawmakers have cautioned against "undoing current and future private sector investments which will continue to increase domestic manufacturing, promote energy innovation and keep utility costs down."

|

Planned infrastructure investment strategies for US electric and gas utilities encompass the modernization of aging transmission and distribution systems, the development of new natural gas, solar and wind power generation capacities, and the adoption of cutting-edge technologies such as smart meters, smart grid systems, cybersecurity measures and battery storage. These substantial investments are anticipated to form the foundation for sustained profit growth within the sector for the foreseeable future.

Expansion of renewable generation resources

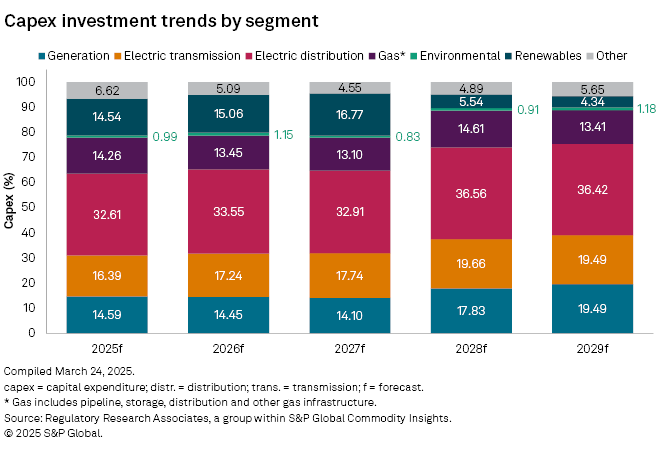

Investment in renewables within RRA's coverage area is projected to exceed $25 billion in 2025, reach above $27 billion in 2026 and exceed $31 billion in 2027 for the utilities that presented a segmented breakdown of their capex. The aggregate renewables investment in each of these years is likely to be considerably higher as some utilities only offered a consolidated view of their planned energy investments.

Renewable energy investment is anticipated to continue on a growth trajectory in subsequent years. Several factors will drive ongoing development in electric utility renewable energy, including declining technology costs, state policies and renewable portfolio standards and consumer and corporate demand, all within a broad trend toward decarbonization in the utility sector.

|

The expansion of renewable generation resources, often located far from demand centers, will require new transmission line projects. Furthermore, despite challenges to the rate of return levels authorized by the Federal Energy Regulatory Commission — such as from periodic changes in return on equity calculation methodologies and underlying models — the average return on equity permitted for transmission investments remains higher than the average equity returns sanctioned by state commissions in traditional general base rate proceedings.

Natural gas integral to energy transition

Natural gas capex will continue to be driven by the need to replace aging gas distribution infrastructure over the long term, in line with state and federal safety mandates. Despite challenges in various regions, natural gas is expected to remain a vital energy source for the foreseeable future, particularly to bridge capacity gaps created by rising datacenter demand that cannot presently be entirely met by renewables due to intermittency coupled with insufficient availability of energy storage.

Furthermore, midstream pipelines and downstream distribution networks are poised to play a pivotal role in efforts by many midstream and utility companies to extend the life span of their infrastructure through LNG exports and through domestic transportation of renewable natural gas and hydrogen blends.

For additional insight into infrastructure investments over the next several years within the US utility industry, refer to the capex databook as of March 24, 2025, also available via the Research Library. The data incorporates intelligence distilled from the aggregation of multiple individual company forecasts.

To access the most recent previous capex analysis, refer to Energy utility capex projected to eclipse $790B from 2025 through 2028.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

For a complete, searchable listing of RRA's in-depth research and analysis, please go to the S&P Capital IQ Pro Energy Research Library.

Regulatory Research Associates is a group within S&P Global Commodity Insights.

S&P Global Commodity Insights produces content for distribution on S&P Capital IQ Pro.

Note: This report is designed to identify capital expenditure trends in the US utility sector, drawing data from a range of sources, including corporate investor presentations, annual reports and other sources. While S&P Global Market Intelligence strives to ensure the accuracy of the included underlying data, the sources vary in terms of depth, quality and timeliness. Actual company-specific capital expenditure information should be acquired from filings with the US Securities and Exchange Commission.

Theme

Location

Products & Offerings

Segment