24 Jan 2019 | 18:29 UTC — Insight Blog

JKM reveals three surprises in 2018 as LNG's commoditization accelerates

Featuring Marc Howson

The LNG market continues to confound expectations. The past year saw strengthening of Platts’ JKM despite new supply, as well as de-correlation from other commodities, and flattening seasonality.

Meanwhile, in 2017/2018, large volumes of more flexible, market-priced LNG supplies reached final investment decision and were agreed for delivery. These will start to flow into the market in 2023/2024, providing an additional medium-term catalyst for the ongoing commoditization of LNG.

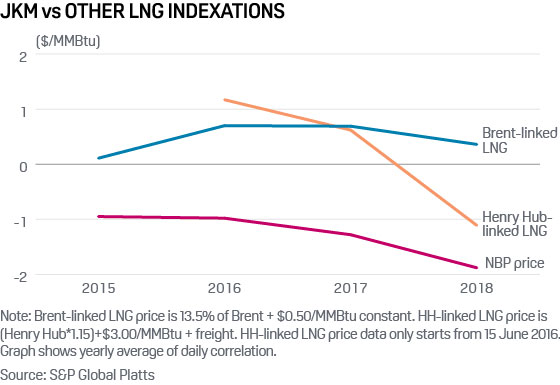

1. JKM decoupled from other LNG pricing indexations

In 2017 there was a relatively high correlation of global LNG and gas prices as increased supply of destination-flexible US LNG helped reduce the spread between JKM and NBP prices. JKM is the benchmark LNG spot price, reflecting LNG deliveries into northeast Asia, and JKM Derivatives are cash-settled against JKM.

But expectations of continued strong price coupling, as US LNG ramped up further, proved misguided in 2018. JKM’s correlation to typical Brent- and Henry Hub-linked LNG contracts, as well as to the NBP, fell sharply. Drivers included new US and Australian liquefaction trains suppressing JKM in the first quarter, while Brent stabilized with OPEC production discipline. Subsequently, during summer 2018, JKM rose far quicker than Brent due to proactive Chinese and South Korean pre-winter LNG buying.

JKM’s correlation with Henry Hub-linked LNG contracts was especially hampered by Henry Hub’s unexpected price surge in the last quarter of 2018, underpinned by a particularly cold winter. In addition, soaring Atlantic and Pacific LNG charter rates after the summer, as shipping journeys lengthened with US LNG deliveries into Asia, further eroded the relative competitiveness of US LNG, while JKM declined.

Legacy LNG contracts linked to either oil or Henry Hub prices face very different price drivers to LNG. This provides an incentive for counterparties to re-negotiate contracts based on non-LNG market pricing, to better reflect LNG market fundamentals.

2. JKM strengthened despite supply growth

JKM reduced its discount to the typical Brent-linked LNG contract price by almost 50%, in absolute terms, year-on-year. By contrast, the absolute premium of JKM over NBP prices grew by nearly 50% year-on-year. Whereas JKM was assessed at a discount to typical Henry Hub-linked LNG contract pricing in 2016 and 2017, this reversed last year, as JKM averaged over US$1/MMbtu above Henry Hub-linked LNG contract pricing.

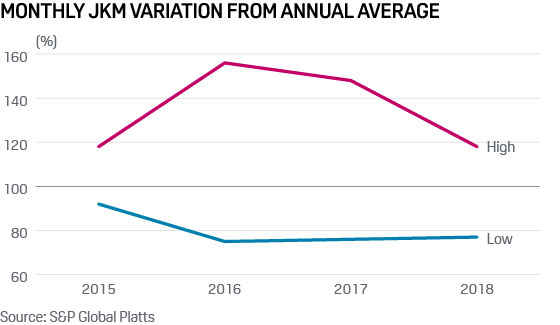

3. JKM seasonality flattened

Strong growth in the seasonal Chinese gas market underpinned JKM’s particularly high 2016 and 2017 seasonality, peaking in the northern hemisphere winter.

However, in 2018 sharply declining global LNG supply in the second quarter, combined with proactive north Asian buying ahead of winter facilitated by growing Chinese LNG/gas storage capacity, reduced JKM’s seasonality. LNG production then ramped up aggressively during the November and December higher demand months, contributing to an uncharacteristic JKM decline in late 2018.

LNG marketing strategies evolve

While the LNG market in 2018 proved unpredictable, it was primarily driven by LNG-specific influences leading to JKM’s decoupling from other commodity prices. It is therefore unsurprising that LNG players are increasingly adopting physical, and derivative, pricing based on LNG benchmark to minimize cross-commodity pricing risks and undertake like-for-like hedging.

Go deeper: S&P Global Platts Special Report on LNG financing

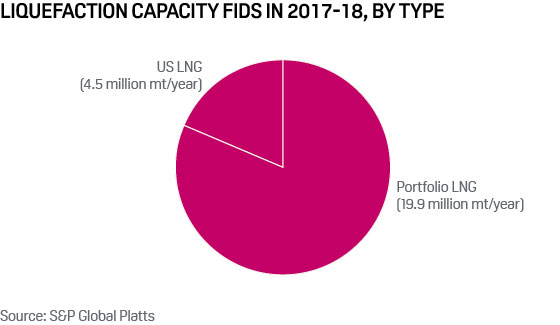

This was publicly illustrated by Tellurian’s 15-year agreement with Vitol, announced in December, for the supply of 1.5 mt/year of JKM-priced LNG. In addition, three of the four liquefaction projects, taking FID in 2017/2018, accounting for over 80% of the volumes, were underpinned by portfolio supplies, as the chart above shows.

These supplies, from Canadian and African projects, are usually marketed by a portfolio offtaker, who is free to sell the volumes at LNG market prices, with no fixed destination, when volumes ramp up. This type of flexible marketing strategy provides a further medium-term catalyst for LNG’s commoditization, increasing ensuring LNG is priced against its own fundamentals.