11 Dec 2018 | 17:58 UTC — Insight Blog

Tellurian-Vitol LNG deal signals shifting balance of power

By J Robinson

The preliminary LNG offtake agreement announced on December 6 between export developer Tellurian and trader Vitol, marks a conspicuous shift in the balance of power in LNG contract markets.

The memorandum of understanding calls for Vitol to lift 1.5 million mt/yr, equivalent to nearly 70.1 Bcf/yr of gas, on an FOB basis from Tellurian's Driftwood LNG-export terminal over a 15-year term.

What makes the otherwise routine supply agreement so consequential is that Vitol's purchase price is actually linked to a destination market price in northeast Asia—the Platts JKM.

It is among the first, if not the only such agreement in the global LNG market.

For the buyer Vitol, the deal dramatically reduces market risk since its contracted LNG-purchase price effectively includes a built-in margin for profit.

While Vitol pays more for LNG as the JKM rises, it also pays less as the benchmark index declines.

If that destination-market linkage wasn't compelling enough, the agreement also includes a shipping component, further reducing the risk imposed by fluctuating charter rates in the global freight market.

Export margin

In recent weeks, volatility in LNG-import and shipping markets, and even in the US onshore gas market, brings some perspective to those contract terms.

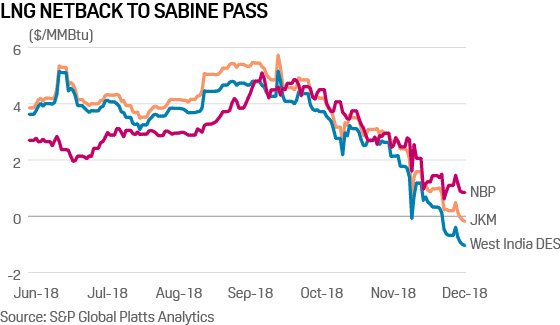

In Northeast Asia, flagging demand for winter LNG supply has seen the JKM tumble. On December 8, the index sank to just $8.75/MMBtu, down from a multi-year high at over $12/MMBtu in September.

At the same time, shipping rates have skyrocketed, recently hitting their highest on record $190,000/d in the Asia Pacific Basin. While prices have since declined modestly, a US Gulf Coast LNG offtaker is still paying nearly $3.60/MMBtu to reach Japan/Korea, and about $4.30/MMBtu to South China or Taiwan.

Meanwhile, the feedstock cost for US LNG exporters has climbed sharply in recent weeks, tracking the upward trend in NYMEX prompt-month futures, which were trading Friday at close to $4.50/MMBtu.

Under more typical, existing LNG-offtake contracts, recent market volatility has crushed the margin on US LNG delivered to northeast Asia.

After paying gas feedstock and onshore transport costs, equal to 115% of the NYMEX Henry Hub, plus shipping, Panama Canal and related freight fees, the profit margin on US LNG delivered to Japan/Korea is actually negative, according to Platts Analytics.

What's more, that calculation actually excludes the liquefaction fee, ranging from $2.25/MMBtu to $3.50/MMBtu since it's typically considered by the industry to be a "sunk cost".

Second-wave exports

In an interview Thursday, Tellurian CEO Meg Gentle said that the exact details of the offtake agreement with Vitol were still being ironed out, so it remains unclear what export-price floor Vitol might face, or whether a liquefaction take-or-pay fee or some more flexible option fee would apply for the buyer.

Regardless of the agreement's exact terms, the announcement was likely unnerving to the US' second wave of LNG export developers that are now in contentious pursuit of offtake contracts, particularly from buyers in Asia's growing import market.

Go deeper: S&P Global Platts special report on LNG financing

While the offtake agreement was Tellurian's first, making them more likely to accept contract terms generous to the buyer, it still speaks volumes about the shifting balance of power in LNG contracting markets.

If Gentle's prediction is correct that the Platts JKM could become an index price for US LNG exports, the move implies much stiffer competition ahead for second-wave projects developers.

The US' largest LNG exporter, Cheniere Energy, currently holds contracts linked to the NYMEX Henry Hub price, effectively shielding the producer from fluctuations in the cost of feedstock gas.

For second-wave producers, though, the ability to delink their feedstock gas cost from Henry Hub—and potentially source gas at a fraction of the benchmark price thanks to new investments—might be their best way to compete heading into the 2020s.