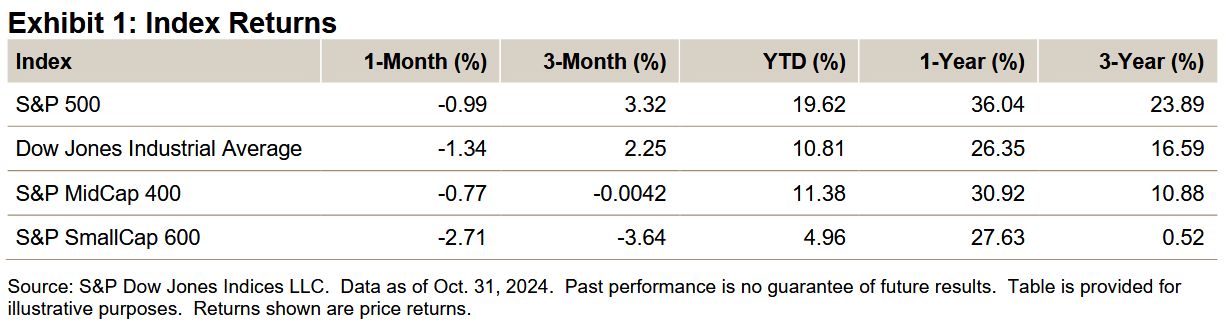

Key Highlights

- The S&P 500® was down 0.99% in October, bringing its YTD return to 19.62%.

- The Dow Jones Industrial Average® lost 1.34% for the month and was up 10.81% YTD.

- The S&P MidCap 400® fell 0.77% for the month, bringing its YTD return to 11.38%.

- The S&P SmallCap 600® moved down 2.71% in October and was up 4.96% YTD.

Market Snapshot

As of Oct. 30, all was good on the Street—not easy or relaxing, but profitable—as the S&P 500 was on the verge of posting its sixth consecutive monthly gain (15.45% cumulatively) and its ninth gain YTD (21.88%, with 47 new closing highs). But Halloween decided to throw in a scare (October as a month is scary, as it contains 32% of the worst 25 trading days in index history) and gave us a fall guy—the Magnificent 7, which declined significantly as a group that day (Oct. 31). However, the 0.96% total return as of Oct. 30 would have been a 0.38% loss absent the Magnificent 7, so as of Oct. 30 they had made the month, and even counting Halloweens broad 1.86% decline, the Magnificent 7 still didn’t drag the index down for the month—the group just took back its earlier October contributions. The net difference for the month’s total return was negligible, at -0.91% with the Magnificent 7 and -0.90% without it, compared to the group contributing 48% of the YTD gain. As for the Street, while the appeal to take the money and go on a two-month vacation is strong (potentially even stronger not to return), you need to be in it to win it.

NVIDIA added 0.57% to the index for the month and helped limit the October loss (it accounted for 25% of the YTD gain), as monthly breadth turned negative (199 issues up and 304 down). Gold continued to shine and the 10-year U.S. Treasury Bond glowed up (pushing prices down), while gasoline pump prices declined, helping CPI and PPI. The U.S. Fed’s next meeting is the day after the U.S. election, with a 0.25% cut expected and another 0.25% cut potentially expected on Dec. 18.

With over 72% of S&P 500 issues reported, Q3 earnings and sales are both on track to set a new quarterly record, with “a great big beautiful tomorrow” expected for earnings, as they are projected to set a new quarterly record in each quarter through 2025 (believe it or not)—and optimism has found an expensive new home, at 25 times trailing 12-month earnings and 21 based on 2025.

As for November, on the front page and definitely affecting trades will be the election. The results, based on the polls (not that they were accurate for 2020), may not be known for days (as mail-in ballots are counted and recounted), or longer if the courts get involved. All of which leads to significant uncertainty—which is the item the market hates the most. The administration determines where budgets are allocated, what taxes and credits will be, and policy toward regulations; without that clarity (or perception of clarity), companies may continue to be commitment shy. In the background will be earnings, as retail starts to declare (with holiday guidance, current estimates call for a 3% increase in spending), along with the Fed’s November meeting, as we also look ahead to the December meeting, while employment data and inflation will all affect trades.

The S&P 500’s market value decreased USD 0.465 trillion for the month (up USD 1.263 trillion last month) to USD 48.236 trillion and was up USD 8.197 trillion YTD; it was up USD 7.906 trillion for 2023 and down USD 8.224 trillion in 2022.

The Dow Jones Industrial Average set seven new closing highs in October (40 YTD), as it traded (and closed) above 43,000 (43,275.19 closing high and 43,325.09 intraday high), after setting seven highs in September, four in August and three in July. For the month, The Dow closed at 41,763.46, down 1.34% (-1.26% with dividends) from last month’s close of 42,330.15, when it was up 1.86% (1.96%) from the prior month’s close of 41,563.08 (1.76%, 2.03%). For the three-month period, The Dow was up 2.25% (2.72%), as the YTD period was up 10.81% (12.50%). The one-year return was 26.35% (28.85%), 2023 was up 13.70% (16.18%) and 2022 posted a decline of 8.78% (-6.86% with dividends).