November 2022 Commentary

Major stock and bond indices posted a welcome rally in November after months of consecutive declines. Markets reversed course this month, driven principally by expectations that policymakers would soon lower the pace of future rate increases.

Market sentiment improved broadly in November. In China, a 20-point playbook of “relaxed” COVID-19 control measures issued by the National Health Commission sparked hopes of an eventual reopening of the country. The eurozone inflation figure for November eased more than expected, supporting a smaller European Central Bank rate hike in December. In his recent remark at the Brookings Institution, U.S. Federal Reserve Chair Jerome Powell indicated that the time for a slower pace of rate increases may come as soon as the next Federal Open Market Committee (FOMC) meeting.

This month, the U.S. Treasury yields moderated, with the 10-year yields falling below 4.0% to 3.68%, while the U.S. dollar continued to soften, dropping over 5%. This combination of lower bond yields and a weaker dollar acted as a catalyst for the market reversal.

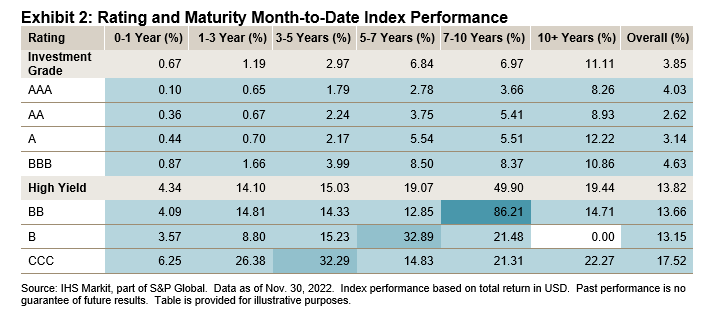

In Asia, U.S. dollar bonds rebounded in November, with the iBoxx USD Asia ex-Japan Index increasing 5.11%, its best monthly performance so far in 2022. The index yield dropped by 0.9 percentage points to 6.47%, and the index spread tightened by 53 bps to 253 bps. As shown in Exhibit 1, the overall index and its major subindices all posted positive returns this month. The China Real Estate Index recorded the largest gain, surging over 30%, while the China LGFV Index registered a comparatively lackluster performance of 0.31%.

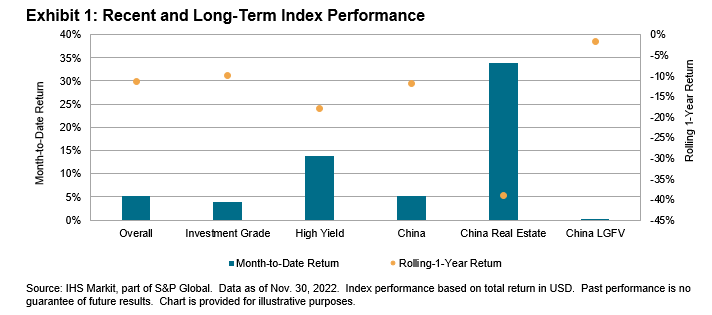

This month, positive performance was observed across the maturity buckets in all credit rating curves. Strong returns were seen in long-dated investment grade (IG) bonds, while significant gains were observed across the curve in the high-yield (HY) category, particularly in maturity buckets with China real estate debt.