Daily Index Insights offers a concise two-minute read on the latest news and trends in index markets. This resource includes performance data from S&P Dow Jones Indices across equities, fixed income, multi-asset, commodities, and factors. Our daily insights are designed to provide you with a comprehensive understanding of market movements, empowering you to make informed decisions based on the most current indices data and analysis.

“What would life be if we had no courage to attempt anything?”

Vincent Van Gogh (March 30, 1853 – July 29, 1890)

Happy Seward’s Day! On this day in 1867, the United States made a bold decision that would redefine its fortunes: the purchase of Alaska from the Russian Empire for $7.2 million, an astonishing two cents per acre. Though the treaty signed in Washington D.C. was famously dubbed “Seward’s Folly” by skeptics who saw only a barren wasteland, the territory’s immense wealth was soon revealed through the Klondike Gold Strike of 1896 and the later discovery of vast oil reserves. Today, Alaskans celebrate this public holiday to honor a transformation from a remote frontier into a vital, strategic pillar of the nation. 159 years later, what was once a ridiculed real estate deal stands as one of history's most lucrative acquisitions. Here is your daily dashboard.

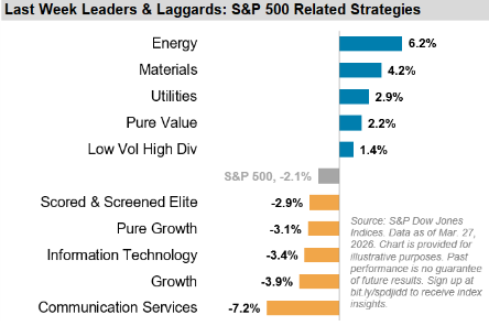

- The S&P 500® suffered a 2.1% drop last week and was down for the fifth week in a row, the longest losing streak since May 2022. Sector dispersion continued to be high, with 13.4% separating the week’s winner, Energy, up 6.2%, from laggard Communication Services, down 7.2%.

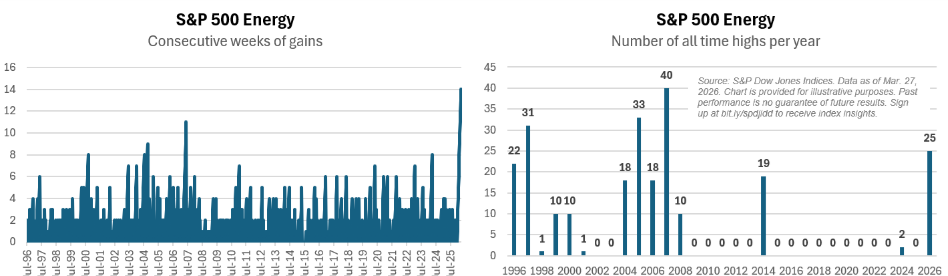

- While the S&P 500 has been losing ground for the fifth consecutive week, S&P 500 Energy is on a tear: its 14-week winning streak is the longest on record, and the sector also clocked up 25 all-time highs so far this year, the most in a calendar year since 2007.

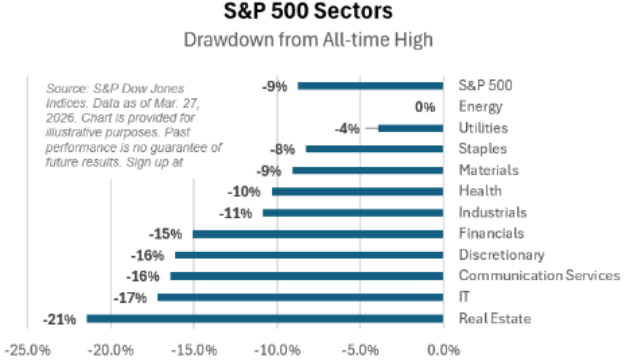

- S&P 500 Energy is flying high, but other U.S. large cap sectors are less buoyant: 6 of them are already in “correction territory”, standing at least 10% below their respective highs, while one, Real Estate, is in a protracted bear market, as the sector trades 21% below is previous high, achieved back in 2021.

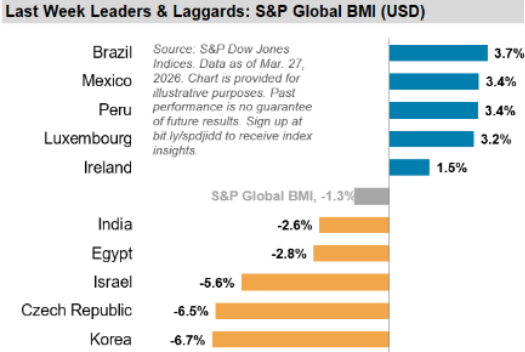

- While monetary policy makers in most developed markets, including in the U.S., are in wait and see mode while assessing the impact of the Iran crisis, some of their colleagues in emerging markets, including in Brazil and Mexico, have been cutting overnight rates last week. Equities in both Latin-American countries jumped in response, and were the top two performing S&P Global BMI regions last week with gains of 3.7% and 3.4%, respectively. At the other end of the spectrum, Korea plunged 6.7%, extending its month-to-date decline to 17% (all returns are total returns in USD).