An unprecedented policy response appears to have curtailed the worst of the assault on risk assets amid COVID-19 disruption, though the improved sentiment has not shifted equally across the credit spectrum, LCD's survey of loan portfolio managers confirms.

With the dust settling on the extreme volatility — at least for now — LCD asked loan managers their forecast on future default and return expectations.

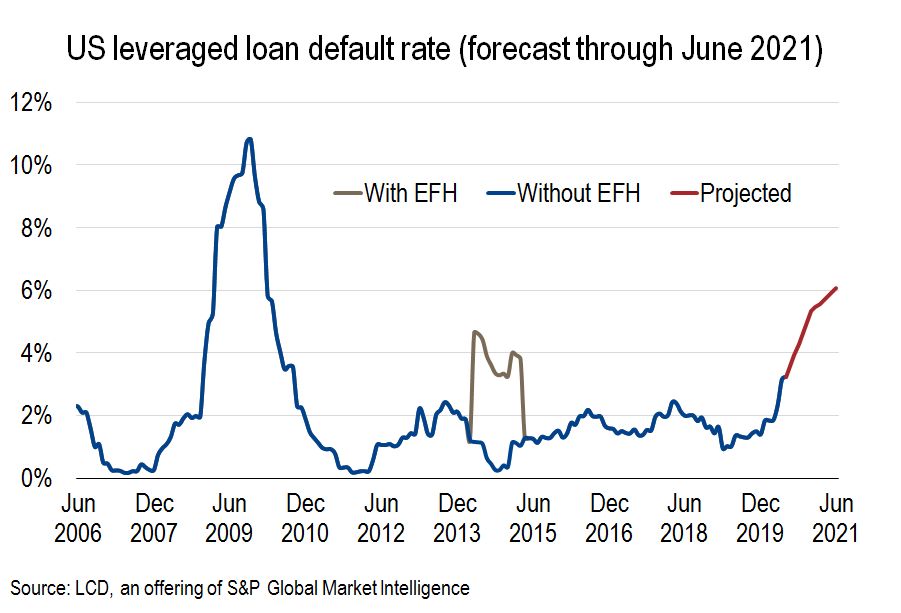

Polling for year-end 2020, participating portfolio managers, on average, expect the default rate to climb to 5.32%, from the June default rate of 3.23%. It has since risen to 3.48%.

There is typically a good deal of dispersion around these averages at the best of times, and currently, potential outcomes are as wide as they have ever been, given the many unknowns regarding the future direction of the COVID-19 pandemic, the sheer volume of government support, and the current lack of clarity on true earnings damage.

Nevertheless, 90% of responses for the year-end 2020 poll were clustered between 4% and 6%.

|

At year-end 2019, the consensus — with a caveat, of course, for the exception of the unforeseen shock that would materialize in the coronavirus crisis — pegged 2020 defaults at 2.32%. At the time, the default rate was just 1.39%.

Sentiment has no doubt improved from the March 23 distress peak, though these results suggest loan managers are still pricing in, on average, 3% of additional defaults from companies they had previously expected would remain solvent at year-end 2020. The uptick is seen in spite of the stimulus measures and actions taken by loan issuers to shore up liquidity via revolver draws and to secure additional covenant headroom.

In the 12-month forward period ending June 2021, managers, on average, predict the trailing rate will climb to 6.08%. In today's market, a 6.08% default rate would equate to a default amount of $70.3 billion, exceeding the 2009 peak of $63.1 billion.

Return to basics

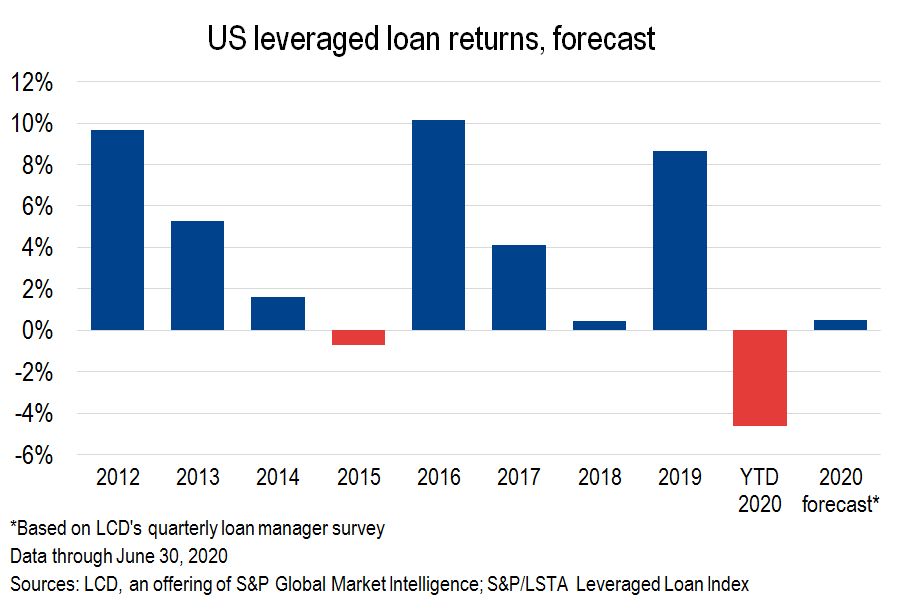

The bucking bronco of performance these past several months has made for a wild ride, though survey respondents, on average, think returns could claw back to positive from the year-to-date return of negative 4.56%, and the negative 12.37% return in March.

The consensus view here calls for a positive return of 0.49% for year-end 2020. Ninety percent of responses were within a range of negative 1.0% to positive 1.5%.

|

Historically, the loan market has posted negative annual returns only twice in the past 23 years — a loss of 0.69% in 2015, on the back of tumbling oil prices, and the devastating 29.1% setback of 2008.

Returning to default expectations, thanks to the unprecedented policy measures, refinancing and amendments of bank lines, and record primary issuance over the past few years, most expect a shallower peak this time, even in the context of the recent shutdowns. However, given the lack of company guidance thus far, the true magnitude of the impact will only start to become clear in the second-quarter reporting season.

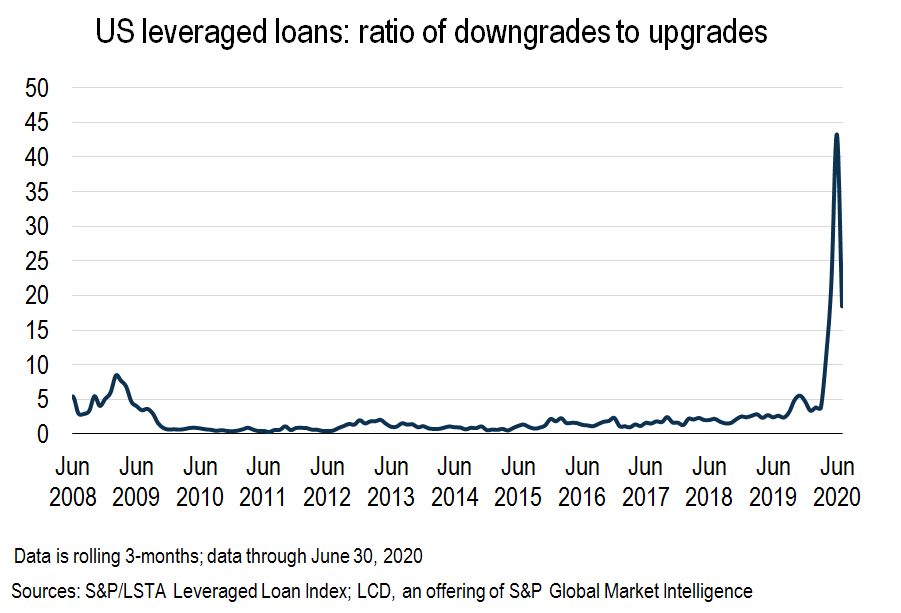

For now, the crisis has already been reflected in the record speed of ratings downgrades this year, specifically in recent months. Through June, 35% of the loan market by par amount outstanding at the facility level had received a ratings downgrade, representing $411.1 billion of the $1.169 trillion of rated loans at the end of 2019. At its peak, the downgrade count of loan facilities in the S&P/LSTA Leveraged Loan Index outpaced the rate of upgrades by a staggering 43:1, on a three-month rolling calculation, in May.

|

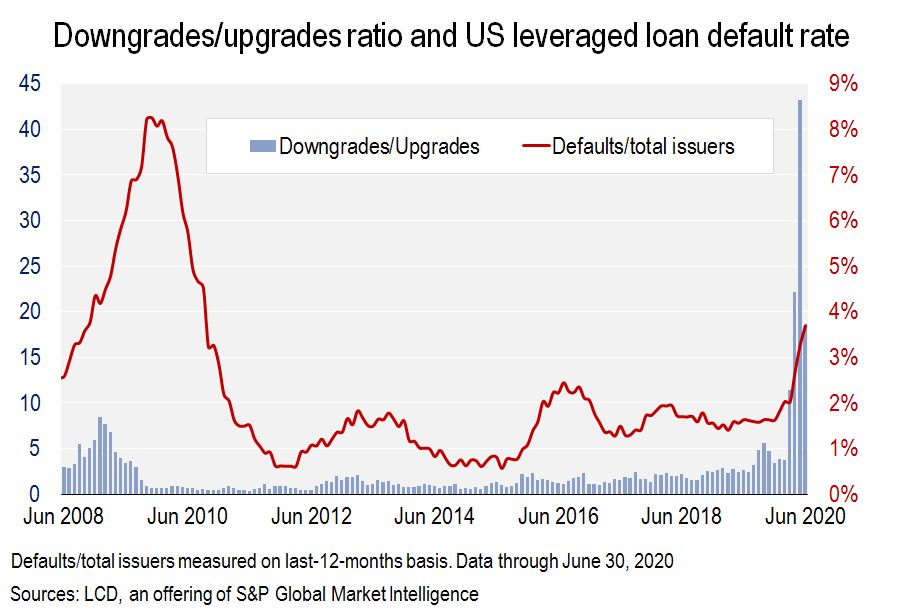

Rising downgrades typically precede a period of rising defaults. The below chart shows how the default rate and the downgrade/upgrade ratio have cycled historically. The downgrade/upgrade ratio averaged 2.7x in the six months before the November 2009 default peak of 8.25%, on an issuer basis.

|

In terms of potential risks on the horizon, a second coronavirus wave, a delay or reversal of reopening from lockdowns, a resumption of tensions between the U.S. and China, and the U.S. presidential elections are all on investor radar screens.

— This analysis was written by Rachelle Kakouris, of LCD Research.