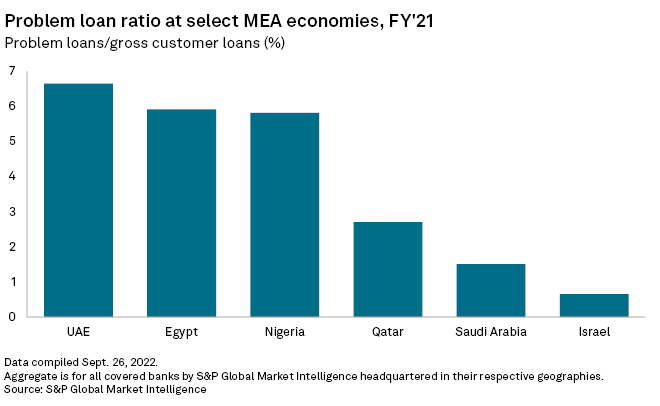

| The UAE has some of the highest nonperforming loan levels among major Middle East and Africa economies, in part due to its high exposure to the construction industry. |

Bank sales of nonperforming loan portfolios in the United Arab Emirates will become more common as lenders prioritize cleaning up their books and improving regulations increase the attractiveness of such deals to buyers, according to market observers.

Abu Dhabi Commercial Bank PJSC, or ADCB, is selling about $1.1 billion of bad debt, including personal and corporate loans and real estate assets, Bloomberg News reported in September. This would be the largest nonperforming loan, or NPL, portfolio sale of its kind in the UAE, said Jaap Meijer, managing director of research at Dubai-based Arqaam Capital.

Local subsidiaries of international banks have made some moderately sized sales of NPL portfolios, while transactions relating to individual borrowers have been taking place for some time, said James Dervin, managing director of Alvarez & Marsal Middle East.

Yet few of these deals, some of which involved international investment firms, have been made public. One exception was UAE-based asset manager and investment bank SHUAA Capital PSC's January 2021 acquisition of 1.13 billion UAE dirhams of debt owed by Stanford Marine Group to various lenders.

"It's not a deep market and trades are few and far between, which is why the ADCB sale is of such significance," said Michael Rainey, partner at law firm King & Spalding in Dubai.

Loan-book cleanse

ADCB's mooted loan sale will benefit the bank by giving it "a lower headline NPL number without a negative impact on the income statement, as the loans had been either fully written off or are fully provisioned on a net basis," said Meijer. It will also free up management time to drive the business forward instead of dealing with legacy positions, as ADCB was hit by several corporate failures over recent years, he said.

The most notable of these failures was Abu Dhabi's NMC Health PLC, which in 2020 admitted to having made a "significant misrepresentation of its debt position in its financial accounts," according to ADCB's annual report. The bank supported a motion to place NMC Health into administration and attributed the company and associated entities for much of its impairments. ADCB declined a request for comment.

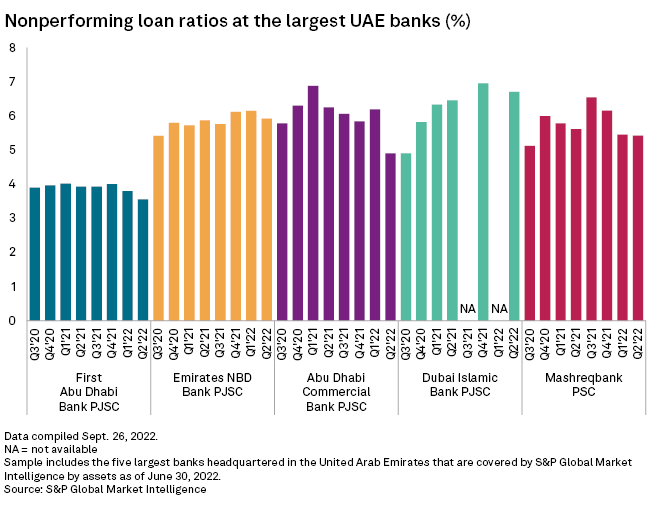

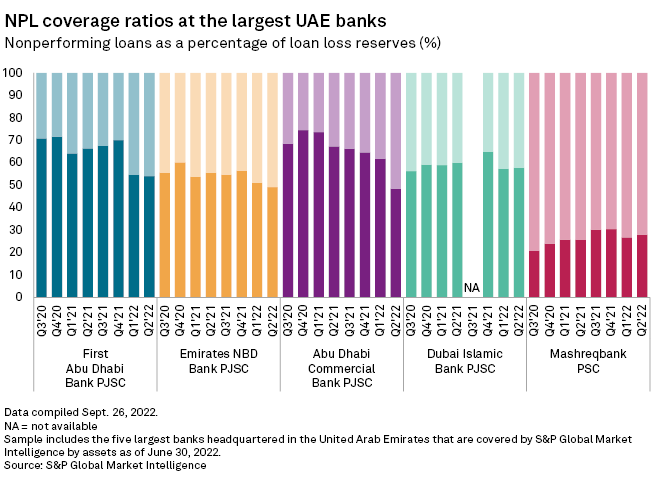

ADCB's NPL coverage ratio of 48.5% in the second quarter was lower than that of peers First Abu Dhabi Bank PJSC, Emirates NBD Bank PJSC and Dubai Islamic Bank PJSC. Of the five largest UAE banks, only Mashreqbank PSC had a lower NPL coverage ratio than ADCB for the period at 27.9%.

Heightened risk

The UAE's problem loan ratio is higher than many major Middle East and Africa economies, Market Intelligence data shows.

UAE banks are exposed to very high credit risks given the industry's aggressive lending and underwriting practices and structurally high concentration to the real estate and construction sectors, according to S&P Global Ratings. Lending portfolios are typically concentrated in a single name, and banks also have significant exposure to some struggling government-related entities, the agency wrote in a July report.

Credit losses have historically been higher among UAE banks than in the rest of the Gulf Cooperation Council, Meijer said, though the strength of the economy means new NPL formation is fairly limited. Ratings forecasts UAE banks' Stage 3 — or nonperforming — loans will be 5.8% to 6.2% in 2022-23 versus 6.1% at the end of last year.

The commercial case for banks selling NPLs is compelling, according to Dervin. "Assuming a sale price above written-down value, not only do you get an improvement in financial performance, but you're also released from the capital restrictions associated with the nonperforming loans," he said.

The likely discount that buyers can expect to receive on the face value of NPLs depends on the specifics of the loan or loans in question, as well as external factors such as the jurisdiction and strength of enforcement mechanisms in that jurisdiction, said Dervin.

Regulatory challenges

A "historically unhelpful legal regime" and "negative attitudes toward financial distress often resulting in a mere reshuffling of deckchairs" have been key factors in the slow development of the UAE's distressed debt market, according to a July note by law firm Mayer Brown.

The UAE's recent mortgage law and civil code allows for the concept of assignment — a third party taking ownership of an existing debt — but it has not been used often, and the requirements are not "especially clear," Mayer Brown wrote.

Instead, distressed debt buyers lacking local lending licenses typically act in the market by means of "a participation" in which the buyer acquires the rights to the debt but the seller remains its legal owner.

"That as a mechanism isn't unique to the region. This is a feature in developed markets when the seller and buyer transact in such a fashion simply because they don't want to make it public," said Dervin, adding that in some cases a lender's ability to exit the position may be constrained by the original loan documentation or other regulatory considerations.

Distressed debt funds based in the U.S. or Europe considering buying NPL portfolios in the Middle East must analyze all regulatory challenges before they even think about doing a deal, said Rainey.

"If you were to buy a nonperforming loan, there's a potential regulatory issue around whether you can even hold such a loan because the business of lending, including holding loans originated by a third party, is in general viewed as a regulated activity," said Rainey.

Mayer Brown notes that considerable advances have been made in recent years to overcome these issues, including the introduction of a new regime for corporate insolvency.

In early 2020, India and the UAE agreed to make UAE court verdicts on loan defaults enforceable in India. Historically, loans in the UAE have been secured with guarantees and post-dated checks commonly asked for, but recent legal changes enable creditors to take security over a debtor's floating assets such as bank accounts and inventory receivables, said Rainey.

For the ADCB sale, the lender may look to get the UAE central bank's blessing before completing the trade, Rainey noted. A positive outcome could give other banks and investors greater confidence in pursuing similar deals in the future.

"As regulation, recognition and the legislative regimes improve, recovery prospects increase and therefore the potential attractiveness and viability of a market increases," said Dervin.

As of Oct. 25, US$1 was equivalent to 3.67 UAE dirhams.