Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Aug 10, 2018

UK economy rebounds in second quarter, but shows signs of losing momentum

- Economy rebound in second quarter but shows loss of momentum in June

- PMI surveys hint at softer start to third quarter

- Bank of England rate hike in question

The UK economy rebounded from a weak start to the year in the second quarter, according to official data, but the latest survey data hint at the pace of growth cooling again in the third quarter.

Growth rebound

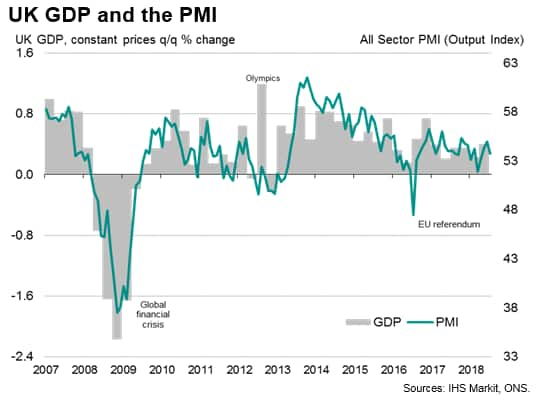

Gross domestic product rose 0.4% in the three months to June, according to the Office for National Statistics. The rise was in line with expectations and double the rate of growth seen in the opening quarter of the year. The rebound means that, after the cold snap earlier in the year, growth returned back in line with the pace of expansion seen in the second half of last year.

The service sector grew 0.5% in the second quarter and construction output jumped 0.9%, but these gains were offset by industrial production falling 0.8% during the quarter.

The breakdown of data through the quarter showed, however, that the pace of growth slowed from 0.3% in May to just 0.1% in June, caused by a stagnation of service sector activity alongside weaker rates of expansion of both manufacturing and construction.

Lower speed limit

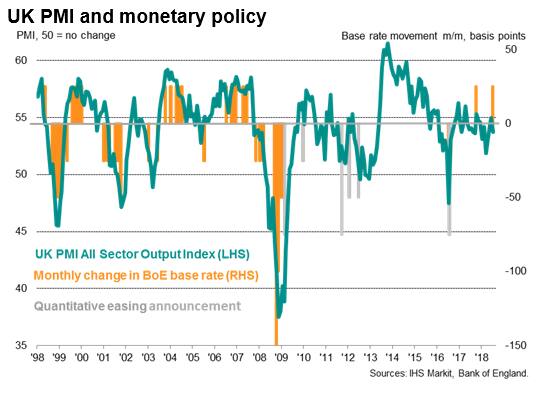

The second quarter rebound was in line with expectations from the Bank of England, which raised interest rates for the second time in ten months at its August meeting. The hike pushed the policy rate up to 0.75%, its highest for nearly a decade though clearly still low by historical standards.

Barring surprises, the Bank sees the economy growing at a steady 0.4% rate in coming quarters, but there are already signs that the third quarter has started on a softer footing.

The PMI surveys collectively indicated a rate of expansion of just over 0.3% in July. The index measuring output of the manufacturing, services and construction sectors fell from 55.0 in June to 53.8 in July, its lowest for three months. Only the construction sector recorded faster growth.

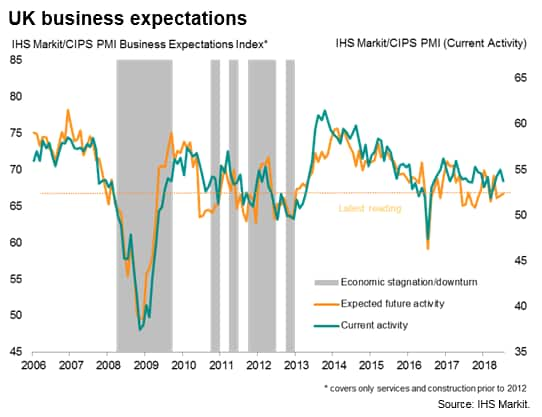

Other indicators from the PMI surveys also hinted at a weakening trend. Inflows of new orders grew at a slower rate than in June and job creation eased to the joint-lowest for nearly two years. Although future expectations rose slightly, the level of business optimism remains stubbornly subdued by historical standards, largely reflecting widespread concerns relating to Brexit.

Rate hike controversy

The dip in the PMI in July makes the Bank's decision to hike interest rates looks unusual. First, prior to last November's rate hike, previous interest rates hikes (since 1999) have only occurred when the all-sector PMI has been above 56.5. It could be argued that the UK economy now has a lower 'speed limit' at which it can grow without stoking inflation, estimated by the Bank to be around 1.5%. However, the pace of growth signalled by a PMI of 53.8 would be below the Bank's new 'speed limit' (more like 1.3% according to our model).

Furthermore, while the November hike had been widely seen as a reversal of the emergency 'insurance' rate cut made in the immediate aftermath of the EU referendum, the August hike should be seen as the first properly 'hawkish' tightening of policy, something which should be justified by improving economic data and rising 'core' inflationary pressures. However, not only did the PMI lose ground in July, but recent inflation indicators have fallen, hence fuelling criticism that it may have been more appropriate to postpone a rate hike when genuine signs of the economy strengthening had appeared, rather than just a rebound from extreme weather.

Next week's labour market data, including employee earnings data, will provide the next test of the economy's health and the Bank's judgement.

Chris Williamson, Chief Business Economist, IHS

Markit

Tel: +44 207 260 2329

chris.williamson@ihsmarkit.com

© 2018, IHS Markit Inc. All rights reserved. Reproduction in

whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI™) data are compiled by IHS Markit for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fuk-economy-rebounds-in-second-quarter.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fuk-economy-rebounds-in-second-quarter.html&text=UK+economy+rebounds+in+second+quarter%2c+but+shows+signs+of+losing+momentum+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fuk-economy-rebounds-in-second-quarter.html","enabled":true},{"name":"email","url":"?subject=UK economy rebounds in second quarter, but shows signs of losing momentum | S&P Global &body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fuk-economy-rebounds-in-second-quarter.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=UK+economy+rebounds+in+second+quarter%2c+but+shows+signs+of+losing+momentum+%7c+S%26P+Global+ http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fuk-economy-rebounds-in-second-quarter.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}