Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

EQUITIES COMMENTARY

Sep 06, 2018

Monthly model performance report – August 2018

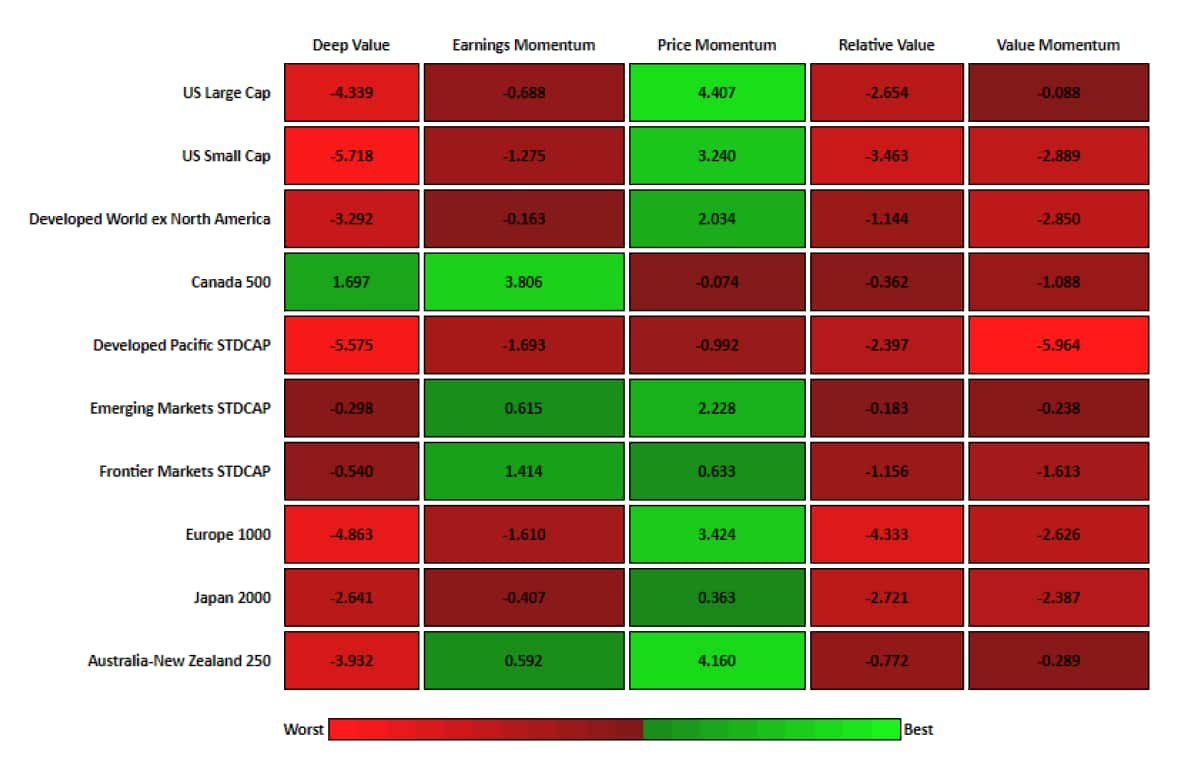

US: Within the US Large Cap universe the Price Momentum model had the strongest one month decile return spread performance returning 4.41% during the month while the Deep Value model lagged. Over the US Small Cap universe our Price Momentum model also outperformed, returning 3.24%, while the Deep Value model lagged. For both universes, the performance of the Price Momentum model was driven by the long portfolio.

Developed Europe: Within the Developed Europe universe our Price Momentum model was the top performer on a one month decile return spread basis, returning 3.42%, while the Deep Value model trailed.

Developed Pacific: Our models struggled over the Developed Pacific universe during the month. The Price Momentum model's one year cumulative performance is currently 9.82%.

Emerging Markets: Within the Emerging Markets universe our Price Momentum model had the strongest one month decile return spread performance, returning 2.23%. The Price Momentum model's one year cumulative performance has improved to 16.90%.

Sector Rotation: The US Large Cap Sector Rotation model returned 0.90%, while the US Small Cap Sector Rotation model struggled returning -5.10%. And our Developed Europe Sector Rotation model performed well, returning 2.60%.

Specialty Models: Within our specialty model library the Oil and Gas and the Semiconductor models had the strongest one month quintile return spread performance returning 2.99% and 2.39%, respectively, while the Bank and Thrift 2 and the Technology models struggled.

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fmonthly-model-performance-report--august-2018.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fmonthly-model-performance-report--august-2018.html&text=Monthly+model+performance+report+%e2%80%93+August+2018+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fmonthly-model-performance-report--august-2018.html","enabled":true},{"name":"email","url":"?subject=Monthly model performance report – August 2018 | S&P Global &body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fmonthly-model-performance-report--august-2018.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Monthly+model+performance+report+%e2%80%93+August+2018+%7c+S%26P+Global+ http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fmonthly-model-performance-report--august-2018.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}