Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Nov 23, 2020

Flash PMI signals renewed economic decline as UK endures second lockdown

- Flash UK composite PMI falls to 47.4 in November

- Service sector business activity slumps amid new COVID-19 lockdown, though manufacturers enjoy temporary boost from pre-Brexit stockpiling

- Business optimism lifted by successful vaccine trials…

- …but employment continues to fall sharply

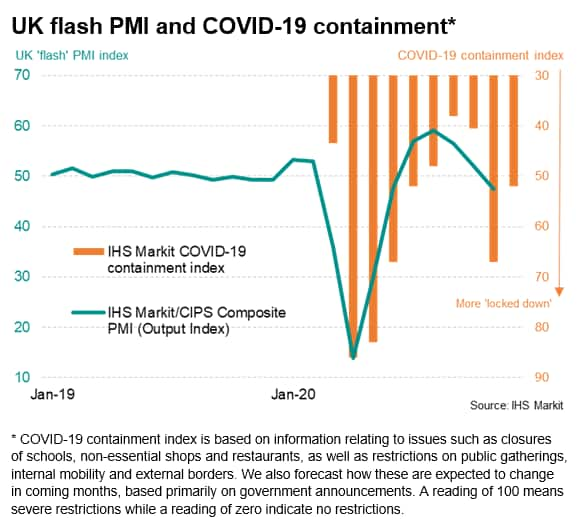

Renewed lockdown measures to contain a second wave of COVID-19 infections has caused the UK economy to slide back into contraction during November, according to the latest flash PMI data. Job losses also accelerated during the month, despite business optimism surging higher amid news of successful COVID-19 vaccine trials.

Renewed economic contraction

The flash IHS Markit/CIPS composite PMI, based on around 80% of normal monthly replies, slumped from 52.1 in October to 47.4 in November, signalling a deterioration of business activity after four months of expansion. However, the decline was considerably less severe than markets had been expecting, with a reading of 44.1 anticipated according to Reuters polling. Although hospitality sectors saw business collapse amid the new virus containment measures, some respite came in the form of a temporary boost to manufacturing from pre-Brexit stockpiling.

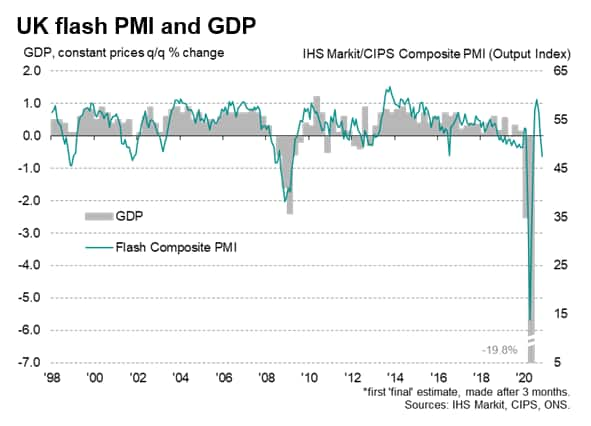

The decline takes the PMI's composite output index to a level historically consistent with GDP contracting at a quarterly rate of approximately 0.3%, but - as seen during the height of the first lockdown in the second quarter - the actual hit to GDP from enforced closures of many businesses may be considerably greater.

We are currently anticipating the economy to contract by 4.4% in the fourth quarter. While that would be considerably less than the 19.8% decline seen during the second quarter, it would be far greater than the 2.1% peak rate of contraction seen during the height of the global financial crisis.

Consumer-facing services collapse, again

Looking in the detail of the November flash PMI, the decline was led by a collapse of business activity in the hotels, bars & restaurants sector amid enforced temporary closures, with other consumer-facing services, travel and transport also suffering steep drops in activity, albeit with rates of decline not quite as severe as seen during the spring lockdown.

Financial services activity meanwhile also fell for the first time since May and business service providers reported the weakest expansion since the recovery from the first lockdown began in June.

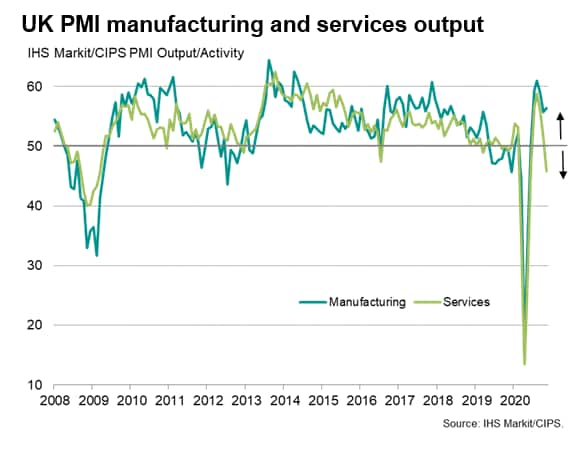

Total service sector activity consequently fell sharply, dropping for the first time since June. The sector's business activity index deteriorated from 51.4 in October to 45.8 in November. Although signalling a steep decline, that compares with a low of 13.4 plumbed during the height of the first lockdown in April to suggest that the impact of the lockdown has not been as severe as seen in the spring.

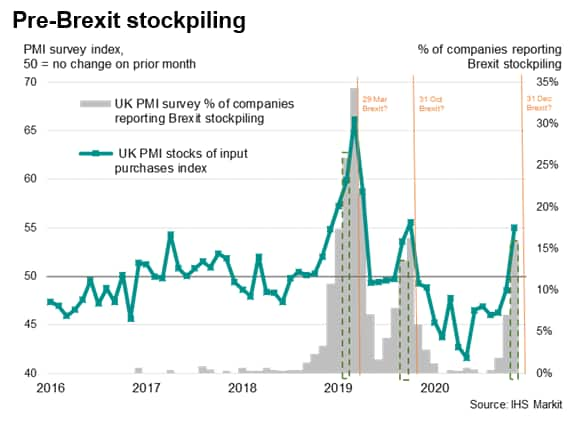

Manufacturers report pre-Brexit boost

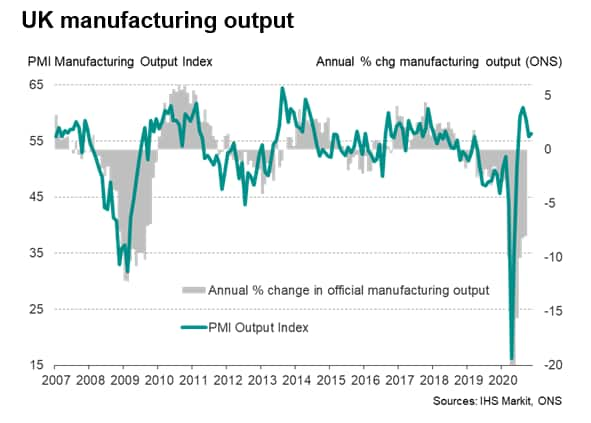

In contrast to the steep loss of output in the services sector, manufacturers reported faster production growth during November, albeit with the expansion often linked to a temporary boost from stockpiling ahead of the end of the UK's Brexit transition period on 31st December. Output rose for a sixth straight month, with the rate of increase picking up slightly, though remaining below the highs seen during the summer. The factory output index rose from 55.8 to 56.3, helping push the headline PMI up to 55.2, it's joint-highest in nearly three years.

Export gains boost manufacturing

The manufacturing upturn was fuelled by a further marked increase in new export orders, which showed the largest monthly rise since January 2018. These export gains were linked to a combination of rising global trade flows, as economies continued to revive from COVID-19 lockdowns, but also to a temporary rise in purchases from EU customers ahead of the UK's departure from the EU free trade area on 31st December. Although just over one-in-four manufacturers reported higher exports in November, almost half of these firms attributed the improvement to pre-Brexit stockpiling by customers.

Worryingly, despite the better export performance, overall new orders rose at a slower rate in November, further underscoring the recent weakening of domestic demand, often attributed to the renewed lockdown measures.

Similarly, exports of services fell at an increased rate in November, posting the steepest decline since June, reflecting virus containment measures both at home and abroad.

Brexit stockpiling reported by 16% of manufacturers

A rising number of manufacturers meanwhile reported that worries over Brexit led to increased stockpiling of inputs, which also temporarily boosted demand at firms supplying these inputs to other companies. Roughly 16% of manufacturers citied Brexit as the cause of higher stocks of inputs, which rose in November to the greatest extent since October 2019, ahead of the first Brexit 'deadline' which was subsequently postponed.

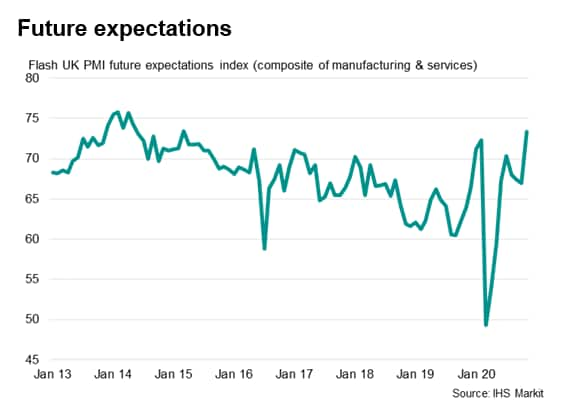

Future expectations at highest since 2015

More encouragingly, although business activity was hit in November by the fresh efforts to contain a second wave of COVID-19 infections, business expectations picked up to the highest since March 2015, buoyed in part by encouraging news during the month on the development of effective virus vaccines. Sentiment about the year ahead perked up in both manufacturing and services, with the latter not surprisingly seeing an especially marked improvement in the hotels, bars & restaurants sector.

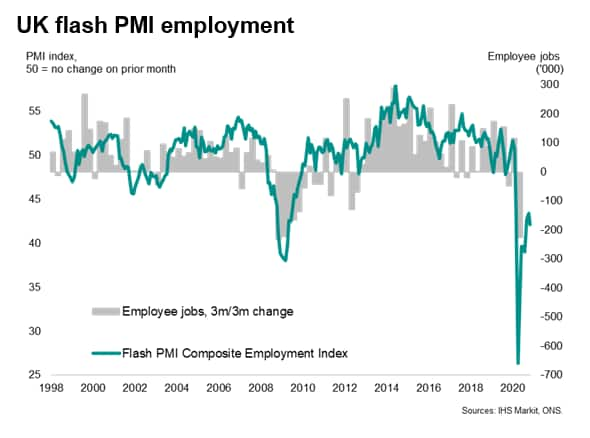

Job losses accelerate

Disappointingly, the upturn in sentiment about the year ahead was not matched by increased hiring. In fact, job losses accelerated during the month to the fastest since August. Job losses in manufacturing eased to a nine-month low but remained high by historical standards, while headcounts were cut at an increased rate in the service sector.

Job cuts were blamed on a combination of weak demand, excess capacity and the anticipation of reduced government support via the furlough scheme, the termination of which was advertised as the 31st October but extended at the last minute alongside the announcement of the renewed lockdown measures.

Chris Williamson, Chief Business Economist, IHS Markit

Tel: +44 207 260 2329

chris.williamson@ihsmarkit.com

© 2020, IHS Markit Inc. All rights reserved. Reproduction in whole

or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI™) data are compiled by IHS Markit for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-pmi-signals-renewed-economic-decline-Nov20.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-pmi-signals-renewed-economic-decline-Nov20.html&text=Flash+PMI+signals+renewed+economic+decline+as+UK+endures+second+lockdown+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-pmi-signals-renewed-economic-decline-Nov20.html","enabled":true},{"name":"email","url":"?subject=Flash PMI signals renewed economic decline as UK endures second lockdown | S&P Global &body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-pmi-signals-renewed-economic-decline-Nov20.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Flash+PMI+signals+renewed+economic+decline+as+UK+endures+second+lockdown+%7c+S%26P+Global+ http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-pmi-signals-renewed-economic-decline-Nov20.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}