Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Aug 23, 2023

Eurozone downturn deepens according to flash PMI but inflation pressures tick higher

Eurozone business activity contracted at an accelerating pace in August, according to the latest flash PMI survey data, as the region's downturn spread further from manufacturing to services. Both sectors reported falling output and new orders, albeit with the goods-producing sector registering by far the sharper rates of decline.

Hiring came close to stalling as companies grew more reluctant to expand capacity in the face of deteriorating demand and gloomier prospects for the year ahead, the latter sliding to the lowest seen so far this year.

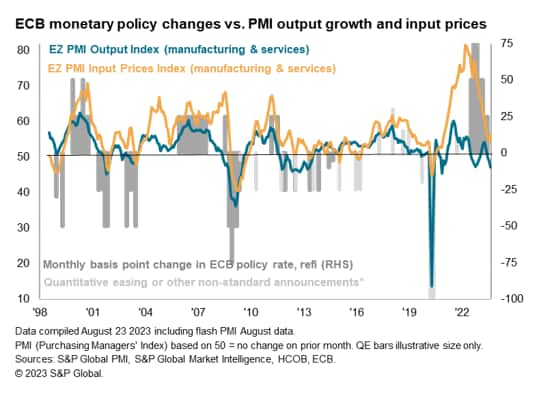

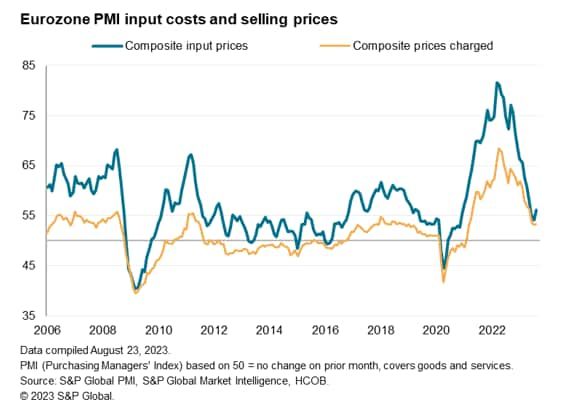

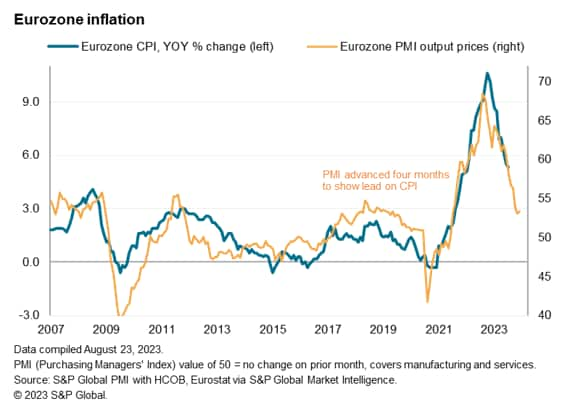

While inflationary pressures continued to run far lower than seen over much of the past two-and-a-half years, led by falling manufacturing prices, August saw headline rates of input cost and selling price inflation tick higher due in part to upward wage pressures. However the overall rate of input cost inflation and selling prices remained indicative of consumer price inflation running at an annual rate of 3% in the coming months.

Output fall gathers pace

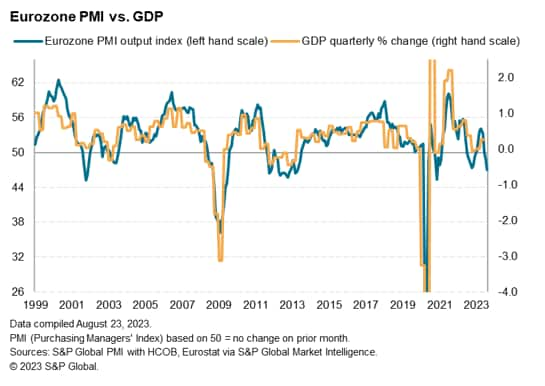

The eurozone economy slipped deeper into decline in August, raising the likelihood of GDP falling in the third quarter. At 47.0, down from 48.6 in July, the seasonally adjusted HCOB Flash Eurozone Composite PMI Output Index, compiled by S&P Global and based on approximately 85% of usual survey responses, fell to its lowest since November 2020. If pandemic months are excluded, the latest reading was the lowest since April 2013.

The August reading is indicative of GDP falling at a quarterly rate of 0.3% which, combined with the July reading sets the scene for GDP contracting by 0.2% in the third quarter.

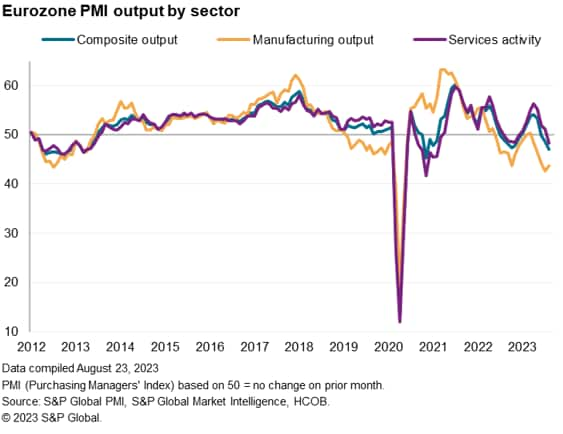

Output has now fallen for three consecutive months, led by a fifth successive monthly decline in manufacturing output. Although the rate of decline of factory output eased slightly in August, it remained the second-strongest recorded by the survey over the past 11 years barring only the initial COVID-19 lockdowns.

The eurozone service sector meanwhile also fell into decline in August, with activity contracting for the first time since last December, albeit at a much softer rate compared to the goods-producing sector.

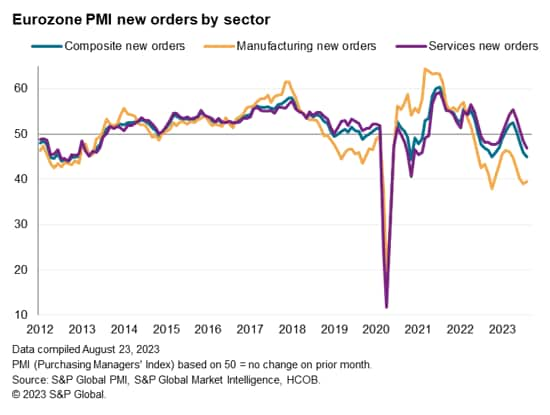

Demand conditions continued to worsen across both sectors. New business inflows fell overall for a third straight month, with the rate of decline accelerating to the fastest since November 2020. Excluding the pandemic, the drop in new business was the steepest since October 2012. New orders for goods continued to fall at one of the sharpest rates since the global financial crisis, accompanied by a second month of deteriorating demand for services. The latter contracted in August at a pace not seen since May 2013 if COVID-19 lockdown months are excluded.

The data therefore hint at a marked cooling of the demand revival seen in the spring for consumer-oriented services such as travel and tourism, which had boomed in early 2023 amid loosened COVID-19 containment measures compared to the prior three years. Anecdotal evidence suggests that this resurgence of activity has been thwarted in part by the increased cost of living and recent hikes in interest rates, combined with concerns over future financial well-being and spill-over effects from a weakened manufacturing economy.

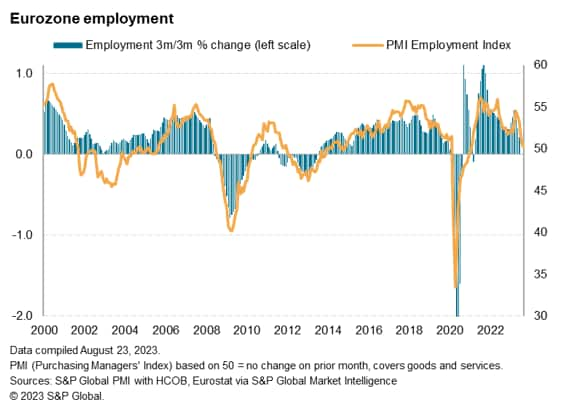

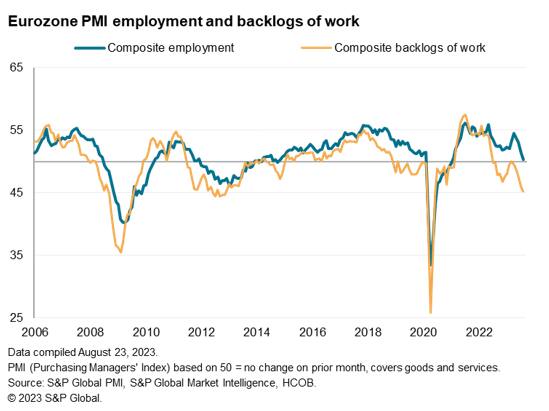

Job gains falter

Employment meanwhile came close to stalling, with the August flash PMI survey registering the smallest rate of job creation since headcounts began rising after the pandemic lockdowns in February 2021. A marginal loss of manufacturing jobs was recorded for a third successive month, while hiring in the larger service sector continued to slow from April's recent peak to register only a marginal rise, signalling the smallest net job gain in the sector since February 2021.

The near stalling of hiring reflected an increasingly sharp decline in companies' backlogs of work, which points to the development of excess capacity relative to demand. The drop in backlogs was the largest since November 2012 if the initial COVID-19 lockdown months are excluded. While manufacturing backlogs fell sharply again, dropping for a fifteenth consecutive month, service sector backlogs fell for a second month running; the rate of decline the sharpest since February 2021.

The deteriorating order book situation played a key role in further denting business confidence in prospects for the year ahead. Companies also cited concerns over broader economic slowdowns at home and in export markets, as well as worries over the impact of higher prices.

Companies' expectations of output levels in the coming year consequently fell for a sixth month in a row, dropping to their lowest since last December and descending further below the survey's long-run average to thereby signal subdued optimism by historical standards.

Prices

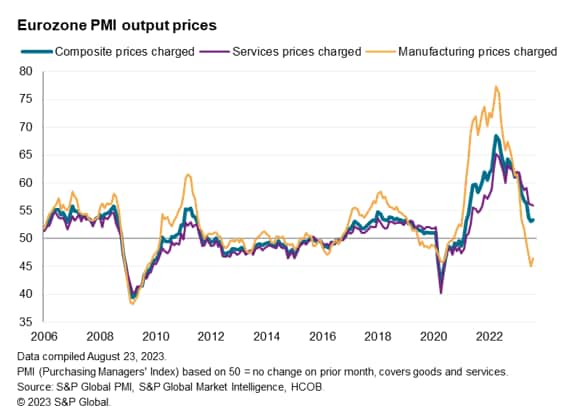

Inflationary pressures meanwhile picked up in August, both in terms of average selling prices and input costs, albeit with both measures signalling far weaker inflation rates than seen throughout the two years prior to the summer.

Average prices charged for goods and services rose at an increased rate for the first time in seven months, pushing the rate further above the survey's long-run average albeit registering the second-slowest rate since March 2021. Goods selling prices fell for a fourth month running, though the rate of deflation moderated. Service sector charges meanwhile rose at the slowest rate since October 2021.

Measured across both sectors, the overall rate of selling price inflation - although up slightly on July - remains consistent with consumer prices rising at a rate of just under 3%, down from the 5.3% rate seen in July. However, note that there is roughly a four-month lead of the PMI on consumer prices.

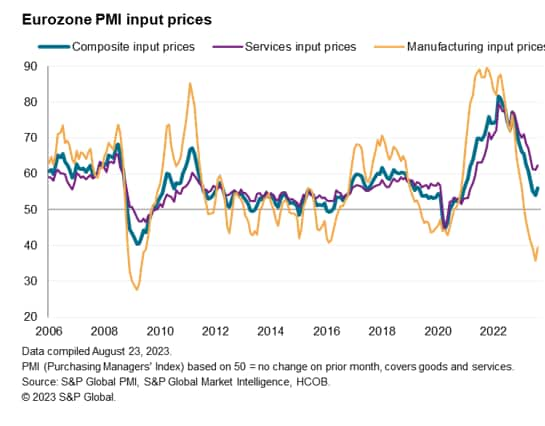

The rate of input cost inflation across both sectors edged higher for the first time in 11 months, though remained marginally below the survey's long-run average. A steep fall in manufacturers' costs, albeit at a reduced rate of deflation compared to July, was accompanied by a slight upturn in service sector input cost inflation, the latter commonly linked to rising wage pressures.

National trends

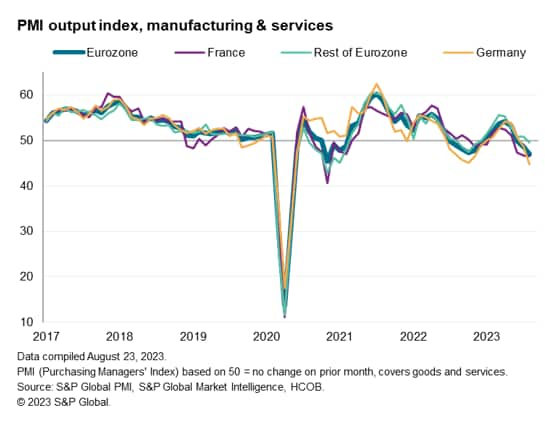

Looking at growth across the euro area, the steepest downturn was recorded in Germany, where output across both goods and services fell for a second month and at a rate not seen since May 2020 (and since June 2009 if the pandemic is excluded). A severe and steepening decline in manufacturing output was accompanied by the first fall in German service sector activity since last December.

France reported a third successive monthly drop in output, the rate of decline unchanged on July, which had seen the sharpest decline since May 2013 barring only four months of pandemic lockdowns. The rate of contraction moderated in manufacturing, though remained sharp, and meanwhile accelerated in services.

The rest of the region suffered a moderate decline in output compared to France and Germany, yet the reduction was notable in being the first recorded since December amid an ongoing loss of manufacturing output alongside a near stagnation of activity in the service sector.

Access the Flash Eurozone PMI press release here.

Chris Williamson, Chief Business Economist, S&P Global Market Intelligence

Tel: +44 207 260 2329

© 2023, S&P Global. All rights reserved. Reproduction in whole

or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2feurozone-downturn-deepens-according-to-flash-pmi-but-inflation-pressures-tick-higher.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2feurozone-downturn-deepens-according-to-flash-pmi-but-inflation-pressures-tick-higher.html&text=Eurozone+downturn+deepens+according+to+flash+PMI+but+inflation+pressures+tick+higher+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2feurozone-downturn-deepens-according-to-flash-pmi-but-inflation-pressures-tick-higher.html","enabled":true},{"name":"email","url":"?subject=Eurozone downturn deepens according to flash PMI but inflation pressures tick higher | S&P Global &body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2feurozone-downturn-deepens-according-to-flash-pmi-but-inflation-pressures-tick-higher.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Eurozone+downturn+deepens+according+to+flash+PMI+but+inflation+pressures+tick+higher+%7c+S%26P+Global+ http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2feurozone-downturn-deepens-according-to-flash-pmi-but-inflation-pressures-tick-higher.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}