Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Apr 23, 2015

China flash manufacturing PMI hits one-year low

The HSBC Manufacturing PMI for China slid to a one-year low in April, according to the preliminary 'flash' reading, signaling an increased rate of decline in the world's largest goods-producing economy and raising the possibility of further stimulus from the government.

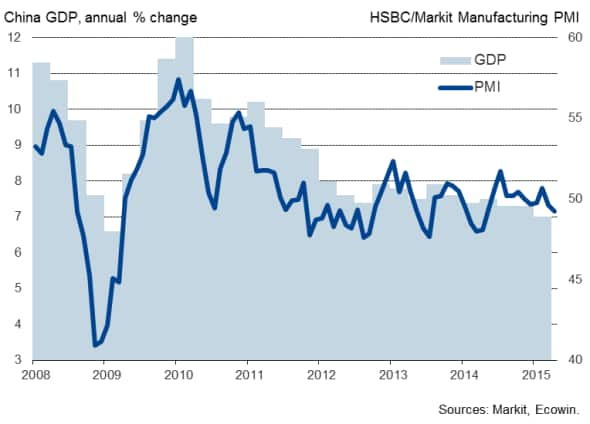

At 49.2 against 49.6 in March, the PMI (compiled by Markit) signalled a deterioration in business conditions for the second successive month and the largest manufacturing downturn since April of last year.

China economic growth and the PMI

Factories reported a second consecutive month of falling volumes of new orders, causing production to more or less stagnate.

The weakening order book trend signalled an increased downturn in domestic demand. New export orders, in contrast, rose slightly for the first time in three months, providing a glimmer of good news.

However, the upturn in exports was insufficient to prevent companies from cutting their headcounts again as factories sought to reduce operating capacity. Volumes of inputs bought also fell, showing the largest monthly decline since March of last year, as firms pared-back production requirements in the face of weaker demand.

Slumping global commodity prices meanwhile led to another marked drop in prices paid for inputs, which in turn fed through to another steep drop in average selling prices. Although the falls in both input prices and factory gate prices were weaker than seen at the start of the year, the marked rates of decline point to ongoing deflationary pressures in China's industrial sector.

Further policy loosening ahead

The drop in the PMI in April clearly represents a disappointing start to the second quarter, raising the possibility of economic growth having lost further momentum compared to the already-weak rate seen in the opening quarter of the year.

Gross domestic product grew at an annual rate of just 7.0% in the first three months of the year, its weakest rise since the height of the global financial crisis in early-2009 and threatening the government's growth target of "around 7%" for the year.

The slowing in the pace of economic growth so far this year has consequently already prompted further stimulus from the authorities, and further stimulus should not be ruled out in coming months. The central bank cut its reserve requirement ratio by a full percentage point to 18.5% on 15th April - the largest such trimming in the amount of capital that banks have to leave with the central bank when making loans to the private sector since November 2008.

The latest action follows two interest rate cuts and one RRR cut since last November. The monetary loosening has been accompanied by a relaxation of housing market measures, previously designed to hold back house price growth, as well as increased infrastructure spending by the government.

Whether the latest cut has the desired effect of boosting bank lending remains doubtful, as demand for loans also needs to rise. However, the fact that the ratio remains at 18.5% indicates that the central bank still has plenty of ammunition if it wishes to provide further stimulus. Given the weak start to the second quarter, it would be wise to expect further stimulus in coming months.

Darker corporate outlook

In the absence of more aggressive stimulus, the corporate outlook has likewise deteriorated compared to last year. Markit's dividend forecasting team are currently expecting the aggregate dividend of FTSE China A50 companies to decrease by 3.3% year-on-year in 2015, compared to 14.1% growth rate in 2014.

The negative dividend growth projected for 2015 is due to the bleak expectation on oil & gas sectors and a slowdown in the banks' dividend growth. On a sector level, Chinese banks are nevertheless expected to contribute approximately 60% to the index total dividends, similar to previous years. The financial services sector is expected to realise the largest dividend growth of 97.7% in 2015, benefitting from the recent positive sentiment on the mainland capital market.

Chris Williamson | Chief Business Economist, IHS Markit

Tel: +44 20 7260 2329

chris.williamson@ihsmarkit.com

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f23042015-Economics-China-flash-manufacturing-PMI-hits-one-year-low.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f23042015-Economics-China-flash-manufacturing-PMI-hits-one-year-low.html&text=China+flash+manufacturing+PMI+hits+one-year+low","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f23042015-Economics-China-flash-manufacturing-PMI-hits-one-year-low.html","enabled":true},{"name":"email","url":"?subject=China flash manufacturing PMI hits one-year low&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f23042015-Economics-China-flash-manufacturing-PMI-hits-one-year-low.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=China+flash+manufacturing+PMI+hits+one-year+low http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f23042015-Economics-China-flash-manufacturing-PMI-hits-one-year-low.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}