Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Jul 22, 2016

Week Ahead Economic Overview

Preliminary second quarter GDP results in the eurozone, the UK and the US will provide policy makers with more guidance to monetary policy in a week during which the Bank of Japan and the Fed announce their latest interest rate decisions. Moreover, inflation and unemployment numbers are released in the currency union.

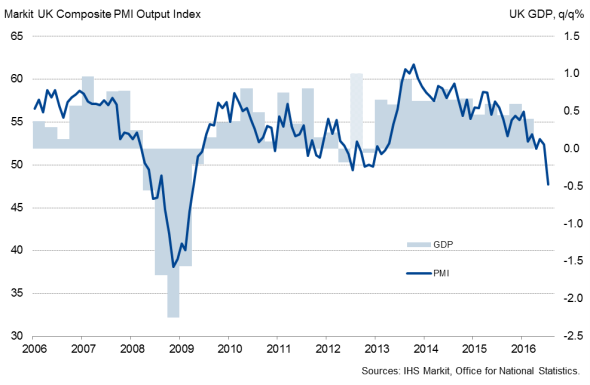

In the month following the UK's decision to leave the EU, the Office for National Statistics publishes its preliminary second quarter GDP results. There is a strong likelihood that growth will have slowed from the already meagre 0.4% expansion seen at the beginning of the year. Based on the PMI, we should expect growth of just 0.2%, with latest flash results pointing to a contraction at the start of the third quarter.

UK PMI and GDP

The 4.7-point drop in the Output Index (which measures the combined output of both manufacturers and service providers) will worry policy makers at the Bank of England who will meet again on August 4th. A cut in interest rates and the introduction of non-standard measures are now firmly on the table, despite the unemployment rate falling further.

There will also be a big focus on the US during the week with the Fed announcing its latest monetary policy decision and the US Bureau of Economic Analysis publishing second quarter GDP data.

The US economy grew 1.1% (annualised) during the opening quarter and IHS estimates that real US GDP increased at a 2.3% annual rate in the second quarter, up from 2.2% growth in the last US Macro forecast, released on 6 July 2016. Stronger consumer spending, government wages, export growth, residential investment, and inventory building were partially offset by weaker federal government spending and stronger import growth.

The Fed won't be able to see the second quarter GDP numbers before they meet on Wednesday, however. Although expectations have risen that the Fed remains on course to hike US interest rates at least one more time in 2016, it is unlikely that this will happen in July, despite employment surging in June.

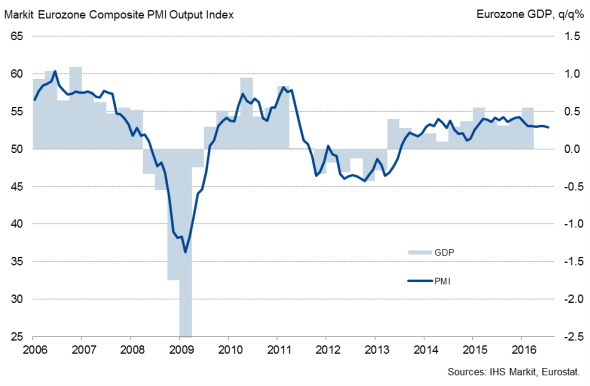

Second quarter GDP results also out in the eurozone, with Eurostat releasing a flash estimate on Friday. Survey data are pointing to robust growth of around 0.5%, but official data suggest that the figure could be more in the region of 0.3-0.4%. Our GDP Nowcast model therefore signals growth of around 0.4%, with a slight downside risk. The currency union also sees updates on inflation and unemployment numbers which will provide analysts with important information on price and labour market trends. A preliminary estimate for inflation showed consumer prices rose 0.1% in July.

Eurozone PMI and GDP

Over in Asia, eyes will be on the Bank of Japan which is expected to introduce further fiscal stimulus. The Nikkei flash Japan Manufacturing PMI remained in contraction territory at the start of the third quarter, thereby adding to worries that the Japanese economy is weakening further. Although Bank of Japan Governor Haruhiko Kuroda rejected the idea of helicopter money, he added that "At this moment, the Bank of Japan has three options with quantitative and qualitative easing with negative interest rates." Forecasts for 2017 economic growth in Japan have been revised down, revealing the lacklustre outlook. With a planned sales tax hike now deferred from late 2017 to 2019, an anticipated increase in spending ahead of the tax rise will no longer take place.

Monday 25 July

Trade data are out in Japan.

Ifo releases its latest Business Climate Index for Germany.

The Confederation of British Industry publishes industrial orders numbers.

In Brazil, consumer confidence figures are released.

Tuesday 26 July

In Germany, retail sales and import price numbers are updated.

BBA mortgage approval figures are issued in the UK.

Meanwhile, current account data are out in Brazil.

Latest S&P/Case-Shiller home price data are out in the US. Moreover, Markit releases flash PMI results for the US service sector, while the Conference Board issues consumer confidence numbers.

Wednesday 27 July

In Australia, inflation numbers are updated.

M3 money supply information are released in the eurozone.

Consumer confidence figures are out in France, Germany and Italy.

Spain sees the publication of retail sales data.

Second quarter UK GDP numbers are issued by the Office for National Statistics.

Bank lending data are meanwhile released in Brazil.

In the US, building permit, mortgage applications and durable goods orders figures are published. Moreover, the FOMC announces its latest monetary policy decision.

Thursday 28 July

Trade price figures are released in Australia.

In South Africa, producer price numbers are out.

Economic sentiment data are published in the euro area.

Unemployment figures are updated in Germany and Spain, while wage inflation figures are out in Italy.

Nationwide house price data are published in the UK.

Initial jobless claims and trade balance figures are issued in the US.

Friday 29 July

In Australia, producer price and private sector data are issued.

Japan sees the release of household spending, inflation, industrial production, retail sales, housing starts and construction orders numbers.

Meanwhile, the Bank of Japan and the Bank of Russia announce their latest monetary policy decision.

M3 money supply and trade balance figures are out in South Africa.

Eurostat releases its preliminary second quarter GDP estimate for the currency bloc, Moreover, inflation and unemployment figures are updated.

Consumer spending numbers are released in France, while current account data are out in Spain.

The Bank of England publishes mortgage data, while GfK issues consumer confidence figures.

Monthly GDP and producer price numbers are updated in Canada.

Preliminary second quarter GDP results are out in the US.

Oliver Kolodseike | Economist, Markit

Tel: +44 14 9146 1003

oliver.kolodseike@markit.com

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f22072016-Economics-Week-Ahead-Economic-Overview.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f22072016-Economics-Week-Ahead-Economic-Overview.html&text=Week+Ahead+Economic+Overview","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f22072016-Economics-Week-Ahead-Economic-Overview.html","enabled":true},{"name":"email","url":"?subject=Week Ahead Economic Overview&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f22072016-Economics-Week-Ahead-Economic-Overview.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Week+Ahead+Economic+Overview http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f22072016-Economics-Week-Ahead-Economic-Overview.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}