Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Jul 22, 2016

Japan flash manufacturing PMI signals intensifying export and deflation woes

Japan's manufacturing economy saw business conditions deteriorate for a fifth successive month in July, suggesting the industrial downturn has extended into the third quarter.

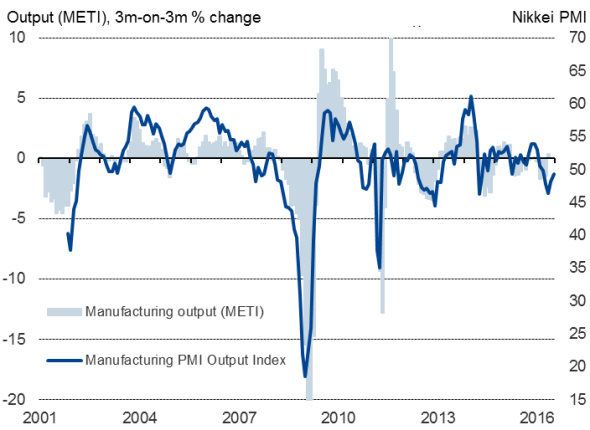

Japan manufacturing output

Factory output and overall order books fell at slower rates than prior months as the impact of April's earthquakes abated, though the elevated yen continued to exert pressure on exports, which fell at the steepest rate since 2012.

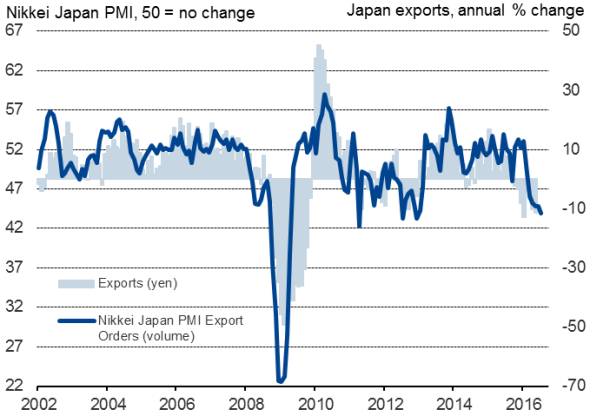

Japan's goods exports

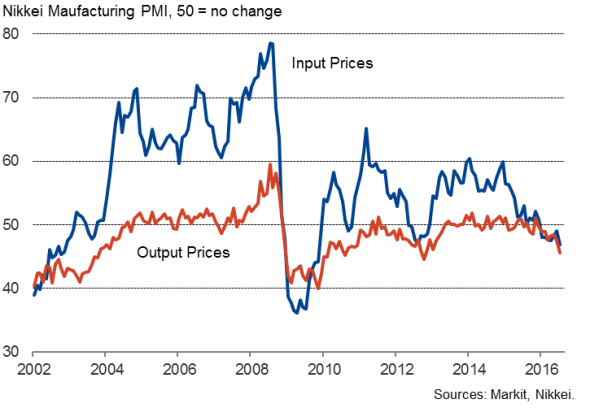

The flip side of the yen's strength was a drop in import prices, which helped drive input costs down at the fastest pace since 2009, providing further bad news for a government seeking to beat deflation.

Downturn extends into third quarter

The Nikkei Manufacturing PMI* rose from 48.1 in June to 49.0 in July, according to the preliminary 'flash' reading, running below the neutral level for the fifth consecutive month but rising to signal an easing in the rate at which the sector's health is deteriorating for a second successive month.

The latest decline signalled was the smallest since March, after which earthquakes disrupted manufacturing in parts of the country and contributed to the steepest downturn in production for over three years in the second quarter. The easing in the rate of decline seen in the past two months therefore in part reflects a process of business returning to normal at affected companies.

* The headline manufacturing PMI is a composite indicator derived from survey questions on output, new orders, employment, inventories and suppliers' delivery times. As such, the PMI gives a broad indication of the health of the manufacturing economy each month but also gives a reliable steer on the performance of the wider economy.

However, while production showed the smallest decline since March, new export orders (measured in volume terms) fell in July at the sharpest rate since December 2012, attributed by producers to a combination of weak global demand and a lack of competitiveness arising from the yen's ongoing strength. Although the currency traded 2% lower compared to the US dollar on average in July, the yen is still 20% higher than a year ago.

Deflationary pressures intensify

The strength of the yen benefited manufacturers by reducing the cost of imported goods, especially energy. Average input costs showed the largest monthly fall since November 2009, a time when commodity prices plunged in the face of the global financial crisis.

Lower costs were often passed on to customers as firms sought to boost sales, with average prices of goods leaving the factory gate dropping to the greatest extent since October 2012.

Producer prices

Pressure builds for further stimulus

The ongoing decline of manufacturing, the steeper slide in export sales and the intensification of deflationary pressures in July bodes ill for third quarter GDP. Any rebound from earthquake-related disruptions therefore seems limited at best, adding to the suggestion that 2016 economic growth will moderate from the already weak 0.6% expansion seen in 2015 and pile further pressure on policymakers to avert a downturn.

Email economics@markit.com for access to the data.

Chris Williamson | Chief Business Economist, IHS Markit

Tel: +44 20 7260 2329

chris.williamson@ihsmarkit.com

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f22072016-Economics-Japan-flash-manufacturing-PMI-signals-intensifying-export-and-deflation-woes.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f22072016-Economics-Japan-flash-manufacturing-PMI-signals-intensifying-export-and-deflation-woes.html&text=Japan+flash+manufacturing+PMI+signals+intensifying+export+and+deflation+woes","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f22072016-Economics-Japan-flash-manufacturing-PMI-signals-intensifying-export-and-deflation-woes.html","enabled":true},{"name":"email","url":"?subject=Japan flash manufacturing PMI signals intensifying export and deflation woes&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f22072016-Economics-Japan-flash-manufacturing-PMI-signals-intensifying-export-and-deflation-woes.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Japan+flash+manufacturing+PMI+signals+intensifying+export+and+deflation+woes http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f22072016-Economics-Japan-flash-manufacturing-PMI-signals-intensifying-export-and-deflation-woes.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}