Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

EQUITIES COMMENTARY

Apr 20, 2015

Short sellers ride out recent market highs

All-time high equity valuations have many market watchers wondering if the current market is ripe for short sellers, following five years of disappointing equity returns.

- The 10% most expensive to borrow names among US stocks have underperformed rest of the US equity market by 72% in the last five years

- Small cap names have provided the most fertile ground for short sellers

- April on track to be the worst performing month for short sellers in over five years

Short selling re-entered the headlines last week when Goldman Sachs released a note stating it has received growing numbers of calls from clients looking to take bearish bets on the market.

Goldman's note highlighted 19 S&P constituents as potential good short targets but came with a health warning. The Credit Suisse Dedicated Short Bias Hedge Fund Index has fallen by a cumulative 52% over the last five years. This lacklustre performance from funds which favour a bearish view of the market makes short selling the worst performing of 13 investment strategies tracked by the Credit Suisse Hedge Fund Indexes.

These poor returns from short-focused hedge funds hides the fact that short sellers on the whole have successfully managed to pick out underperforming shares over the last five years, as gauged by the performance of the shares which cost the most to borrow in the stock lending markets.

Short sales continue to perform

The 10% of US stocks which cost the most to borrow, essentially those seeing the most bearish sentiment, have underperformed the market by a cumulative 70% over the last five years, according the Markit Research Signals' Implied Loan Rate factor. This underperformance among shares which exhibit bearish investor sentiment has been fairly consistent over the last five years, with the shares most targeted by short sellers underperforming the market for over three out of four months on average.

However it is worth noting that the most expensive to borrow names have actually outperformed the market by over 3.5% so far this month.

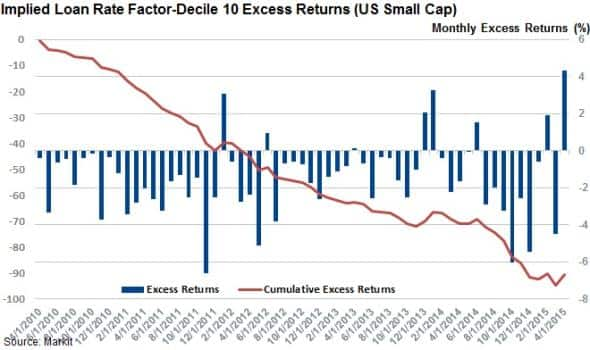

Small caps most fertile

Short sellers have had the most success when shorting small cap names over the last five years. The most shorted names among the Markit US Small Cap universe have underperformed their peers by over 90% in the last five years.

The performance among large cap short sales is much less impressive with the most shorted 10% of shares in the Markit US Large Cap universe cumulating at 18.5%.

But this underperformance is only relative as the section of shares which cost the most to borrow are still up by 60% among large cap names, showing that the runaway market is largely to blame for the lacklustre performance from short biased funds.

Sector rotation active

The composition of the most shorted group of shares within the US total cap universe has changed significantly over the last few years.

Financials used to comprise 22% of the constituents seeing the most bearish sentiment from short sellers, but this number has since fallen over the last five years by a quarter to 15%; far lower than the sector's overall representation in the Markit US Total Cap universe.

The falling demand to sell financial shares short over the last five months has been mirrored by an increased propensity to sell energy names short. Energy names now make up 19.5% of the most expensive shorts among US shares, up from 13% five years ago.

Simon Colvin | Research Analyst, Markit

Tel: +44 207 264 7614

simon.colvin@markit.com

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f20042015-equities-short-sellers-ride-out-recent-market-highs.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f20042015-equities-short-sellers-ride-out-recent-market-highs.html&text=Short+sellers+ride+out+recent+market+highs","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f20042015-equities-short-sellers-ride-out-recent-market-highs.html","enabled":true},{"name":"email","url":"?subject=Short sellers ride out recent market highs&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f20042015-equities-short-sellers-ride-out-recent-market-highs.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Short+sellers+ride+out+recent+market+highs http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f20042015-equities-short-sellers-ride-out-recent-market-highs.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}