Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

EQUITIES COMMENTARY

Mar 19, 2015

Short sellers target recent IPOs

2014 was the most active year for IPOs since 2000. However, short sellers profited by targeting the newly listed shares.

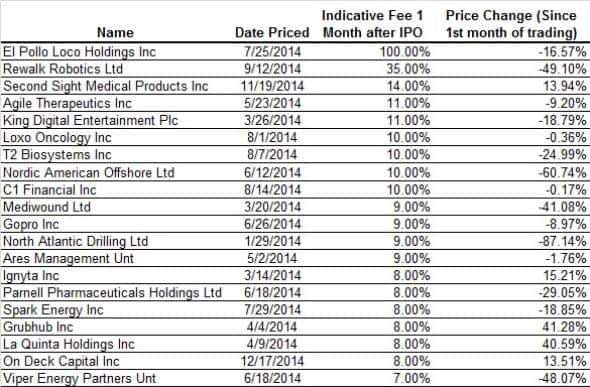

- The top 20 most expensive to borrow IPO share have declined by an average of 14.5%

- El Pollo Loco was the most expensive stock to borrow one month after its IPO; its shared have subsequently retreated by over 16%

- The most successful IPO shorts in 2014 were offshore drilling companies: Nordic American Offshore and North American Drilling

Alibaba's $22bn record breaking IPO last September, propelled the 2014 total for US IPOs to $85bn, eclipsing the previous year's tally by just under 50%. The year's 273 new listing also provided plenty of scope for short sellers who targeted several of the year's most publicised listings with profitable results.

The 20 IPOs in 2014 which were the most expensive to short one month on from their trading debut (as gauged by the Markit indicative fee, a measure of how much a hedge fund would have to pay to keep a short open), have performed significantly worse than other listings. The majority of last year's IPOs remained cheap to short.

The top 20 most expensive shorts lost an average of 14.5% from one month after the IPO to date. Conversely, the IPOs which cost the least to borrow, gained an average of 14% during the same period.

The cost to borrow reflects the relative demand and conviction that short sellers have in a company's shares declining in future. Focusing on the cost to borrow one month post IPO allows more time for recently listed shares to enter into lending programs and thus become available for short sellers to borrow.

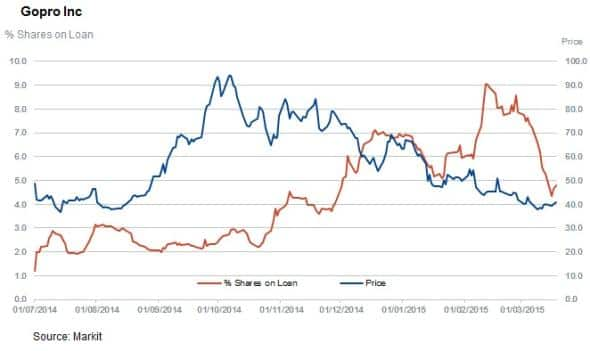

This is evidenced in GoPro, which saw very strong demand to borrow in the immediate aftermath of its IPO but only saw short interest as a percentage of the total shares outstanding break through the significant 5% mark in December, four months after listing.

This absolute amount of shares on loan masks the extremely strong demand to borrow the shares. Short sellers were willing to pay close to 100% of the borrowed value on an annual basis in order to gain short exposure to Gopro shares, which tripled from their offer price. However, Gopro shares have since gone on to underperform, rewarding the conviction of short sellers, who have recently been covering their positions.

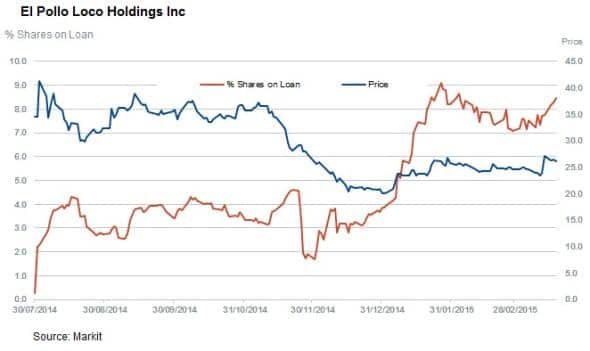

The IPO which cost the most to borrow (after one month from its trading debut) was El Pollo Loco. Short sellers were willing to pay 100% on an annualised basis to gain exposure to the company's shares, which have since retreated by over 16%.

Energy collapse plays to short sellers

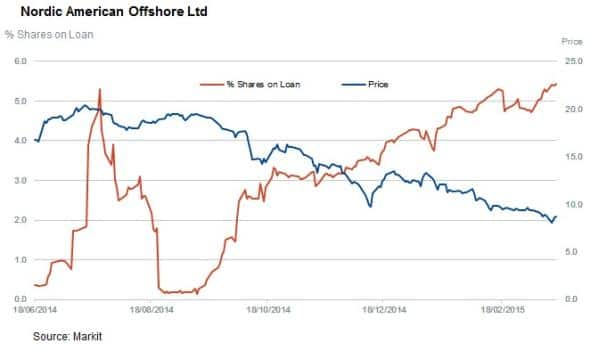

The most successful short positions of last year's IPOs were taken in largely unpublicised and arguably ill-fated listings from drilling operators: Nordic American Offshore and North American Drilling.

The former cost short sellers more than 9% to borrow one month on from listing. The recent collapsing oil prices, and the associated cutback in production has sent shares Nordic American Offshore down by 60%.

North American Drilling proved even more profitable for short sellers as its shares are now changing hands for 87% less than they did a month on from its trading debut.

Viper Energy Partners has also made the list of successful IPO short positions as its shares are down by over 48% (one month on from listing).

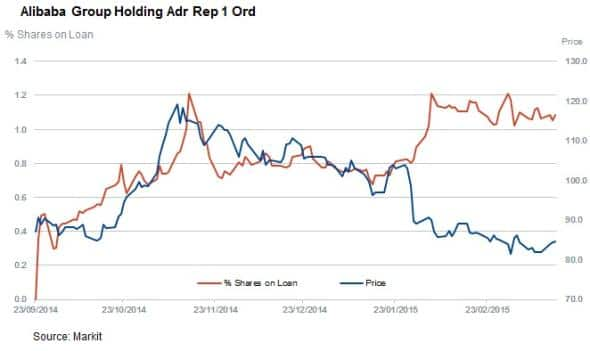

Baba not significantly shorted

As for the largest listing of the year, Alibaba's shares saw high indicative rates in the first few days of trading, which was significant for a company of its size. But the increase in lendable supply lowered the cost to borrow and the stock has since lost its "special" status in the securities lending market.

The percentage of shares outstanding on loan has slowly crept up as the stock continued to underperform since highs reached in November.

Andrew Laird | Securities Finance Analyst, Markit

Tel: +1 646-312-8990

andrew.laird@markit.com

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f19032015-Equities-2014-vintage-IPOs-fertile-ground-for-short-sellers.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f19032015-Equities-2014-vintage-IPOs-fertile-ground-for-short-sellers.html&text=Short+sellers+target+recent+IPOs","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f19032015-Equities-2014-vintage-IPOs-fertile-ground-for-short-sellers.html","enabled":true},{"name":"email","url":"?subject=Short sellers target recent IPOs&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f19032015-Equities-2014-vintage-IPOs-fertile-ground-for-short-sellers.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Short+sellers+target+recent+IPOs http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f19032015-Equities-2014-vintage-IPOs-fertile-ground-for-short-sellers.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}