Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Jun 16, 2015

UK pulls out of brief foray into deflation

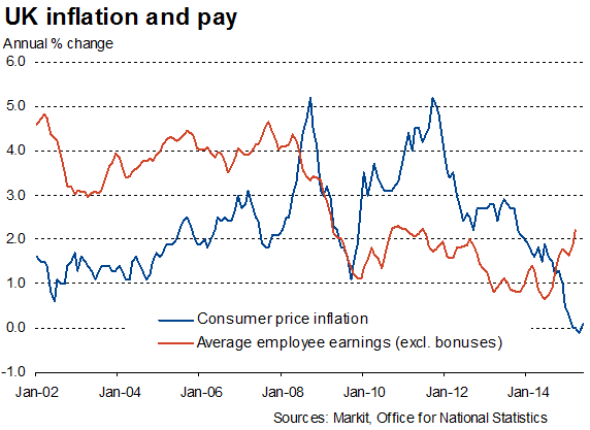

Inflation rebounded in May, bringing an end to the country's brief foray into deflation. Having dipped into negative territory in April for the first time since 1960, consumer price inflation rose to 0.1% in May, according to the Office for National Statistics.

The dip into deflation was always expected to be temporary, linked largely to the timing of Easter and a related impact on travel prices.

Price pressures are reviving mainly as a result of higher oil prices. Brent crude prices were on average 7.5% higher in May compared with April, contributing to a 1.9% increase in fuel prices during the month.

However, core inflation (excluding energy, food, alcohol and tobacco) also picked up, rising from 0.8% in April to 0.9% in May, and further upward pressure on inflation looks likely in coming months, as factory prices fell at the slowest rate since December, down a mere 1.6% on a year ago. The PMI survey's measure of factory gate prices has meanwhile risen to a nine-month high.

Oil prices have fallen back somewhat in recent days, but are well up on their lows seen at the turn of the year and therefore still expected to exert upwards pressure on inflation in coming months.

Wage growth is also showing signs of reviving, albeit only modestly, as the labour market continues to tighten.

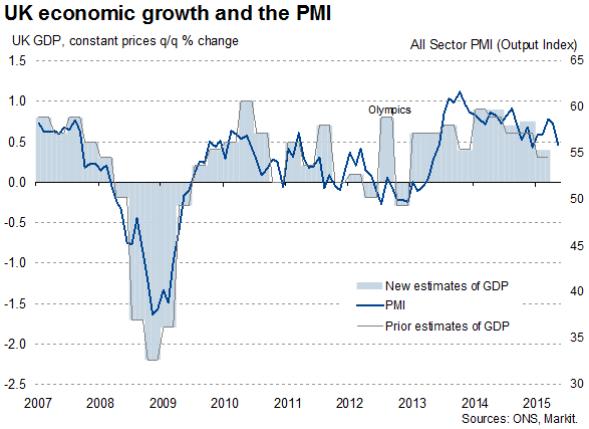

The combination of rising price and wage pressures, alongside upward revisions to recent economic growth, will add to pressure for the Bank of England to start hiking interest rates.

However, the outlook for inflation still looks benign, and the Bank's 2.0% target remains a long way off.

Importantly, the recent strengthening of sterling, which has the effect of reducing the cost of imports, will help offset the oil impact. The Bank will also be in no rush to start raising interest rates merely on the back of higher oil prices, and policy makers will want to see evidence that core inflation and wages are showing more convincing upturns.

With business survey evidence casting a shadow doubt on the health of the UK economy in the second quarter, the Bank will also want to await more evidence that the recent slowdown has been temporary, attributable to factors such as uncertainty surrounding the general election, before feeling comfortable that the economy is ready for higher borrowing costs.

A rate hike this year still looks unlikely, though it's reasonable to assume that pressure to raise rates will build as we move towards the end of the year, leading to an initial hike in early 2016.

Chris Williamson | Chief Business Economist, IHS Markit

Tel: +44 20 7260 2329

chris.williamson@ihsmarkit.com

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f16062015-economics-uk-pulls-out-of.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f16062015-economics-uk-pulls-out-of.html&text=UK+pulls+out+of+brief+foray+into+deflation","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f16062015-economics-uk-pulls-out-of.html","enabled":true},{"name":"email","url":"?subject=UK pulls out of brief foray into deflation&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f16062015-economics-uk-pulls-out-of.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=UK+pulls+out+of+brief+foray+into+deflation http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f16062015-economics-uk-pulls-out-of.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}