Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

EQUITIES COMMENTARY

Jun 14, 2016

Short covering hits securities lending profitability

The appetite to short sell in the US equities has fallen from the fever pitch of the opening months of the year, which has taken some of the shine off securities lending revenues.

- High conviction shorts trading special have fallen in both proportion and fees this year to date

- Return to lendable has fallen by one-third from the March highs of 6bps

- Aggregate balances are still up $100bn in the last 12 months, helping drive revenues higher

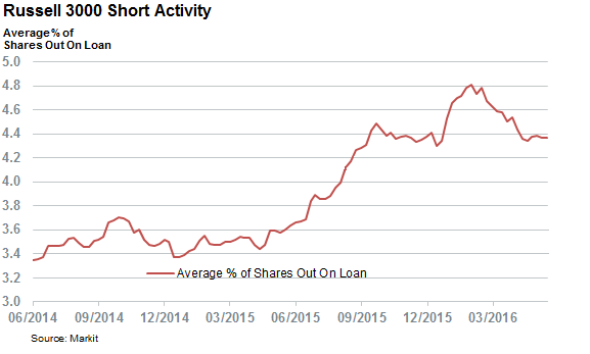

Short selling activity has cooled off from the fever pitch of the opening two months of the year, which has seen the fees commanded by and proportion of Russell 3000 constituents trading "special" fall significantly. The average short interest among the index's constituents, which is responsible for over 95% of the US shorting activity by volume, has dropped by 10% from the highs seen in April.

This short covering has seen the number of Russell 300 constituents trading "special" in the securities lending world, defined by short interest greater than $5mn and a stock loan fee above 100bps on annualised basis, fall significantly from the highs seen earlier in the year. Over 10.2% of the Russell 3000 constituents traded special as far back as April, that number has since shrunk by 15% with 8.7% of the index's current constituents now meeting the special criteria.

This trend means that there are fewer Russell 3000 index shares trading special than at any time since last October, which speaks volumes of the decreased appetite to sell short in light of the recent market rebound.

Energy names shorts, which have been at the core of the recent market rebound and associated covering, have felt this trend most acutely. This has taken the number of energy shares commanding a special fee to 29, down from 33 at the start of the year.

Healthcare firms, which regularly feature prominently among top short selling targets, have continued to be popular high conviction short plays with more healthcare names now trading special than at the start of the year. The sector is now responsible for one-third of the shares trading special in the Russell 3000 index, which is nearly the same as the three next most highly shorted sectors combined.

No longer that special

Another indicator of the falling short seller demand is the fact that the fee to borrow these special names has fallen significantly from the highs seen at the start of the year. The weighted average specials fee, which was over 650bps as far back as April, has now settled in the 500-550bps range.

Impacting return

The falling number and cost to borrow specials as well as the recent short covering is starting to hit securities lending profitability. The aggregate fee generated from US equity stock loan was in the region of 70bps for much of the last six months, but the slip seen in special shares means that the aggregate US stock loan fee is now 50bps; the lowest amount since October 2013.

However, the situation is not as dire as these fees would indicate as there are now many more short bets being taken in the market as the aggregate balance of stock loan trades has remained above the $500bn mark despite the recent covering.

This has helped keep aggregate daily revenues generated by stock loan trades around the $6m mark, up from $5m in 2013.

Simon Colvin | Research Analyst, Markit

Tel: +44 207 264 7614

simon.colvin@markit.com

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f14062016-Equities-Short-covering-hits-securities-lending-profitability.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f14062016-Equities-Short-covering-hits-securities-lending-profitability.html&text=Short+covering+hits+securities+lending+profitability","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f14062016-Equities-Short-covering-hits-securities-lending-profitability.html","enabled":true},{"name":"email","url":"?subject=Short covering hits securities lending profitability&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f14062016-Equities-Short-covering-hits-securities-lending-profitability.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Short+covering+hits+securities+lending+profitability http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f14062016-Equities-Short-covering-hits-securities-lending-profitability.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}