Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Jun 11, 2015

Steady growth of Chinese factory output and retail sales offset by weak investment

Official data brought more mixed news on the health of the Chinese economy, with signs of steadying retail sales and factory output offset by news that fixed asset investment is growing at its slowest rate for 14 years.

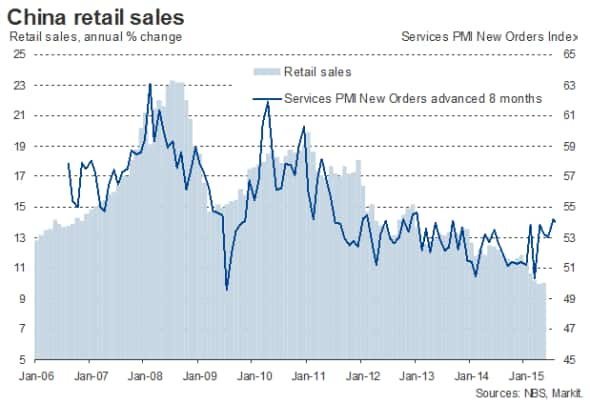

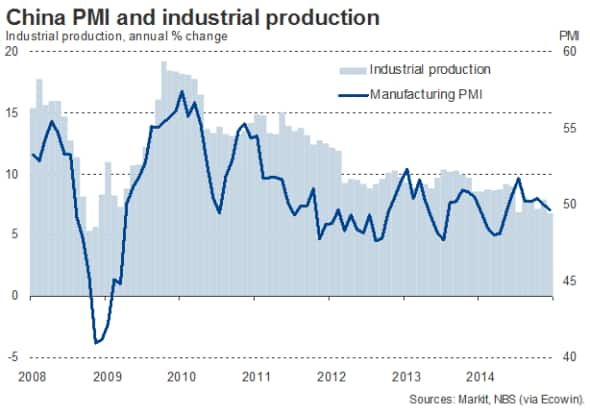

Industrial production grew 6.1% compared to a year ago in May, up from 5.9% in April and better than economists had generally been expecting. Growth of retail sales likewise picked up slightly, growing at annual rate of 10.1% in May, up from 10.0% in April.

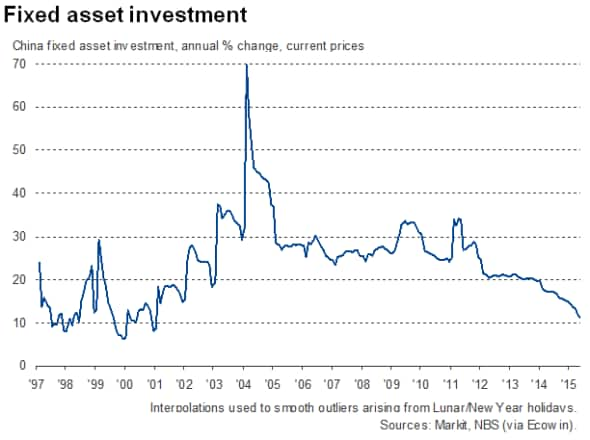

However, the official data also showed fixed asset investment growing at an annual rate of just 11.4% in the first five months of the year, the rate of increase having deteriorated markedly this year to the weakest since 2001.

Furthermore, while the trends in factory output and retail sales stabilised, growth rates remain subdued by recent standards. The trend in retail sales is the weakest since 2003 and industrial production growth is the slowest since the global financial crisis.

Economy transitioning

The weakness of the data add further to evidence that the Chinese economy looks set to grow by 7% at best this year, down from 7.4% in 2014 and the slowest expansion seen for 25 years.

Survey data suggest that the slowdown in China is having an increasing impact on other economies in the region, with Hong Kong in particular seeing a steep downturn, as exports to China fell at the fastest rate since 2008. Manufacturing across Asia ex-Japan contracted for a second successive month.

However, while the survey data for China have been weak this year by historical standards, the data paint a mixed picture by sector.

Markit's PMI data showed manufacturing output falling for the first time this year in May, having stagnated in April, but the services PMI survey indicated the fastest rate of growth of business activity for eight months.

The poor manufacturing survey results largely reflect a deteriorating export trend, while the improvement in the service sector in part reflects rising domestic demand.

The PMI survey data also bring some encouraging signs for near-term growth of the domestic economy. New orders for services - which acts as a useful advance indicator of retail sales - grew at the fastest rate for three years in May, suggesting retail sales growth should pick up further in coming months.

The survey data therefore support the view that the Chinese economy is slowly transitioning away from exports and investment towards domestic consumption, a rebalancing that many see as essential to longer term development and helping boost China's financial service sector.

The outlook remains uncertain, however, as although the PMI data indicate that recent central bank stimulus may be boosting parts of the economy, weak investment - especially in the housing market - poses a major risk to the economy.

Bleaker, but mixed, dividend outlook

This mixed picture is reflected in the corporate dividends outlook. Markit's dividend forecasting team are currently forecasting the aggregate dividend of FTSE China A50 to decrease by 3.3% year-on-year in 2015, compared to 14.1% growth in 2014. The negative projection for 2015 is due to the bleak expectation on oil & gas sectors and slowdown in the banks' dividend growth.

However, on a sector level, Chinese banks are expected to contribute approximately 60% to the index total dividends, similar to previous years. The financial services sector is expected to realise the largest dividend growth of 97.7% in 2015.

Chris Williamson | Chief Business Economist, IHS Markit

Tel: +44 20 7260 2329

chris.williamson@ihsmarkit.com

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f11062015-Economics-Steady-growth-of-Chinese-factory-output-and-retail-sales-offset-by-weak-investment.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f11062015-Economics-Steady-growth-of-Chinese-factory-output-and-retail-sales-offset-by-weak-investment.html&text=Steady+growth+of+Chinese+factory+output+and+retail+sales+offset+by+weak+investment","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f11062015-Economics-Steady-growth-of-Chinese-factory-output-and-retail-sales-offset-by-weak-investment.html","enabled":true},{"name":"email","url":"?subject=Steady growth of Chinese factory output and retail sales offset by weak investment&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f11062015-Economics-Steady-growth-of-Chinese-factory-output-and-retail-sales-offset-by-weak-investment.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Steady+growth+of+Chinese+factory+output+and+retail+sales+offset+by+weak+investment http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f11062015-Economics-Steady-growth-of-Chinese-factory-output-and-retail-sales-offset-by-weak-investment.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}