Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Sep 09, 2016

Week Ahead Economic Overview

The week sees important updates on price and industry trends in the eurozone and the US, while retail sales and production data are the focus in China. Attention also turns to the Bank of England as it announces its latest monetary policy decision.

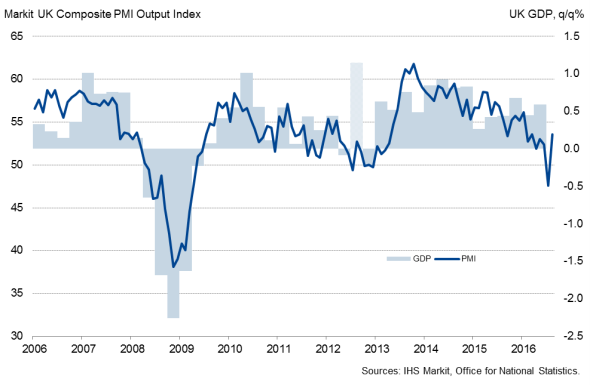

The Bank of England announces its latest monetary policy decision on Thursday. After cutting interest rates to a new historic low of 0.25% at its prior meeting, there has been some criticism that the Bank was too aggressive in supporting the economy after the Brexit vote, especially after business survey data pointed to a rebound in economic activity in August following the sharp decline seen in July. However, Bank Governor Mark Carney said that he was "absolutely comfortable" with the Bank's decision adding that it is "welcome there is a rebound" in the economy. Although it is widely expected that the Bank will not introduce further stimulus in September, rates could well be cut again later in the year if political and economic uncertainty prevail.

UK GDP and the PMI

UK policymakers will also keep an eye on retail sales and labour market data for July for signs of Brexit-related shocks to consumer spending and hiring decisions. The unemployment rate remained at an 11-year low of 4.9% in the three months to June, but there were clear signs of a shift in labour market conditions in July.

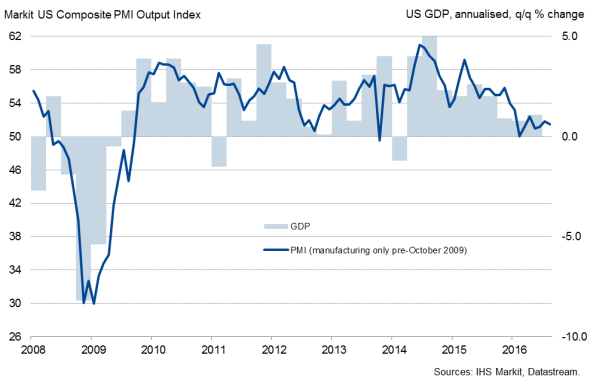

Over in the US, it looks unlikely that the Fed will pull the trigger again in September by raising interest rates after US job creation cooled and survey data pointed to only lacklustre growth in the third quarter. Nevertheless, some policymakers including John Williams, president of the San Francisco Fed, favour a rate rise "sooner rather than later", arguing that "the economy has climbed back to full strength". The release of latest inflation and industrial production numbers is therefore likely to add important fuel to the policy debate at the "data-dependent" Fed.

US GDP and the PMI

In July, US annual consumer price inflation rose to 0.8%, down from 1.0% in June, and further tame inflation readings in coming months would add to the case of deferring the next rate hike. Meanwhile, latest PMI data suggest official data will signal only moderate growth of manufacturing output in August.

Industrial production and retail sales numbers will meanwhile add to the policy debate in China. Although overall economic growth was steady during the first half of the year, IHS Markit expects a slowing in the second half of 2016. While latest official data showed a 6.0% rise in industrial production, there is a strong likelihood that growth will slow in coming months, with latest PMI data from Caixin signalling a stagnation of the manufacturing sector in August.

As Beijing is looking to transition the Chinese economy away from a reliance on exports and investment spending to consumer demand, policymakers will also keep a close eye on retail sales numbers. IHS Markit predicts a further slowing of retail sales growth in coming months, with the rate of increase likely to drop below 10%. If the data flow continues to disappoint, the central bank may introduce more measures to boost growth.

The European Central Bank left monetary policy unchanged at its September meeting, but will continue to follow the data flow carefully, with inflation, industrial production and trade data released during the week.

Latest PMI survey results suggest that a moderate growth trend in eurozone industry continued into the third quarter. However, official data for Germany showed the sharpest drop in industrial output for nearly two years, thereby clearly adding some downside risks for the eurozone July figure.

Meanwhile, the latest ECB staff macroeconomic projections foresee HICP inflation at 0.2% for 2016, with September data released on Thursday.

Monday 12 September

Machinery orders figures are released in Japan.

India sees the publication of current account numbers.

UK regional PMI results for August are out.

Tuesday 13 September

NAB business conditions data are released in Australia.

Business confidence figures are meanwhile issued in Japan.

In India, consumer price numbers are out.

China sees the release of industrial output and retail sales data.

Current account numbers are updated in South Africa.

Eurostat releases latest employment numbers for the currency union.

In Germany, Spain and the UK, inflation figures are out, with the former also seeing the release of latest ZEW economic sentiment results.

Italy sees the publication of industrial production data.

Retail sales numbers are updated in Brazil.

The latest NFIB Business Optimism Index is out in the US.

Wednesday 14 September

Australia sees the release of consumer confidence data.

In Japan, industrial production and capacity utilisation numbers are out.

M3 money supply and wholesale price data are issued in India.

Retail sales figures are published in South Africa.

Industrial production numbers are released in the eurozone.

Inflation figures are meanwhile out in France and Italy.

UK labour market data are released by the Office for National Statistics.

Mortgage application numbers are published in the US.

Thursday 15 September

In Australia, unemployment and car sales numbers are published.

The latest Reuters Tankan Diffusion Index is released in Japan.

Industrial production figures are meanwhile updated in Russia.

Eurostat publishes inflation and trade data in the euro area.

The Swiss National Bank and the Bank of England announce their latest monetary policy decisions. Moreover, retail sales numbers are issued by the Office for National Statistics.

In the US, initial jobless claims, current account, retail sales and industrial production data are released.

Friday 16 September

The Bank of Russia announces its latest monetary policy decision.

Labour costs data are issued in the eurozone.

In Italy, latest trade numbers are published.

Brazil updates activity data for its service sector.

Manufacturing sales figures are issued in Canada.

In the US, consumer price and real earnings data are updated alongside the latest Reuters/Michigan Consumer Sentiment Index.

Oliver Kolodseike | Economist, Markit

Tel: +44 14 9146 1003

oliver.kolodseike@markit.com

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f09092016-economics-week-ahead-economic-overview.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f09092016-economics-week-ahead-economic-overview.html&text=Week+Ahead+Economic+Overview","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f09092016-economics-week-ahead-economic-overview.html","enabled":true},{"name":"email","url":"?subject=Week Ahead Economic Overview&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f09092016-economics-week-ahead-economic-overview.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Week+Ahead+Economic+Overview http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f09092016-economics-week-ahead-economic-overview.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}