Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Jul 08, 2016

US employment surge helps allay short-term growth worries

US employment growth rebounded with a vengeance in June, but the underlying trend remains one of a slowdown in hiring, and it's far from clear whether June's bumper non-farm payroll increase reflects a renewed appetite among companies to hire staff.

For sure, today's data add to scope for interest rates to be nudged higher before the year is out. But the bigger picture remains one in which the Fed is likely to err on the side of caution, with policymakers viewing the better than expected hiring in the perspective of a more uncertain longer-term outlook.

More volatility, this time in hiring

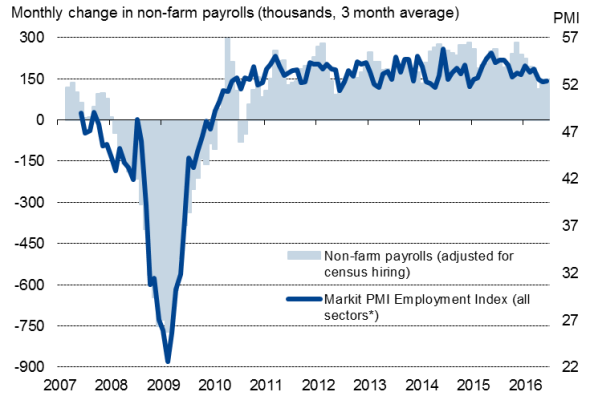

Non-farm payrolls rose by 287,000 in June, rebounding in spectacular fashion after increasing by a mere 11,000 in May (downwardly revised from 38,000). The data smashed consensus expectations of a 175,000 increase and was the largest monthly rise since last October.

Non-farm payrolls v Markit PMI Employment Index

However, it's clear that the jobs data have been distorted in recent months, not least by an extended strike by Verizon employees. So it's more important than ever to look at the trend in the payroll numbers rather than any single month. Here the shine comes off the latest report. Over the second quarter, non-farm payrolls rose at an average monthly rate of just 147,000. That's down from 196,000 in the first quarter and the lowest since the second quarter of 2012, but still a healthy pace of job creation, especially for an economy at, or near, full employment.

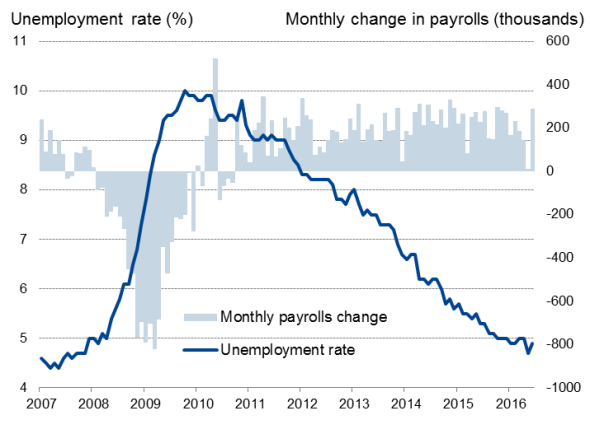

Although the unemployment rate rose to 4.9%, having slipped to 4.7% in June, this was not altogether bad news. The increase was driven in part by more people entering the labour market, which is often a sign of people gaining more confidence in the economy.

US labour market

* Manufacturing only pre-October 2009.

On the other hand, the household survey also showed unemployment rising by 347,000 in June, taking some of the wind out of the 484,000 decline seen in May and means unemployment fell by a mere 91,000 in the second quarter.

Pay disappointed again, rising just 0.1% in June, though the annual rate crept up to 2.6%. This was its highest since December, but clearly still relatively subdued by historical standards.

Cautious Fed

Prior to the labour market update, Fed fund futures were not pricing in any rate hikes until the end of 2016, and even then with only an 18% likelihood of a further quarter point rise.

With the Fed watching the high frequency data to get a better perspective whether to hike rates again, today's report will therefore up the odds of a rate hike this year. The recent slowdown in hiring prior to June was singled out by the Fed as a key factor creating uncertainty about the US economic outlook, so the brighter employment report for June will help allay some of the fears about the short-term growth profile for the US.

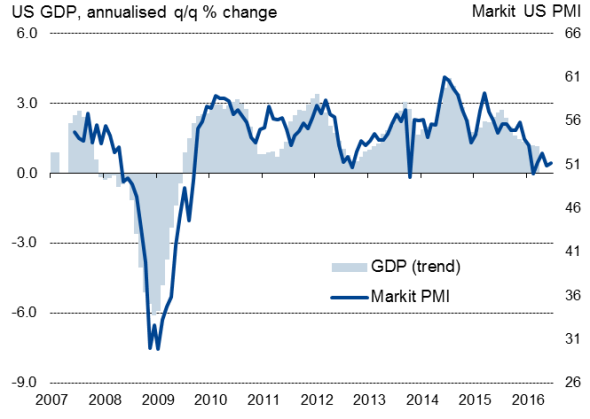

Recent data are also suggesting the economy picked up speed again in the second quarter, with GDP growth expected to rebound to an annualised rate of 2.5% after the slowdown to 1.1% seen in the first quarter.

But not all indicators are pointing to such robust health. Markit's PMIs, which have provided an accurate view of the underlying trend in GDP growth, cutting through the volatility in the official data, were signalling only around 1% growth again in the second quarter.

Economic growth indicators

Sources: Markit, Datastream, Bureau of Labor Statistics.

Policy also clearly won't be based on one set of good numbers, and today's report will be looked at within a bigger picture of economic uncertainty. Recent Fed meeting minutes have highlighted the extent to which policymakers are worried about downside risks to the outlook from external shocks, one of which was a vote for the UK to leave the EU.

The uncertainty and financial market volatility created by the Brexit vote is therefore perhaps the strongest argument for the Fed to hold off with any further tightening that might intensify the unsettled mood currently being seen in the markets.

Chris Williamson | Chief Business Economist, IHS Markit

Tel: +44 20 7260 2329

chris.williamson@ihsmarkit.com

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f08072016-economics-us-employment-surge-helps-allay-short-term-growth-worries.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f08072016-economics-us-employment-surge-helps-allay-short-term-growth-worries.html&text=US+employment+surge+helps+allay+short-term+growth+worries","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f08072016-economics-us-employment-surge-helps-allay-short-term-growth-worries.html","enabled":true},{"name":"email","url":"?subject=US employment surge helps allay short-term growth worries&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f08072016-economics-us-employment-surge-helps-allay-short-term-growth-worries.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=US+employment+surge+helps+allay+short-term+growth+worries http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f08072016-economics-us-employment-surge-helps-allay-short-term-growth-worries.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}