Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Feb 05, 2016

Week Ahead Economic Overview

GDP numbers are expected to show further signs of global economic growth having weakened at the end of last year, leaving the markets to watch for a smattering of higher frequency data releases to gain an insight into the extent to which malaise has lingered into 2016.

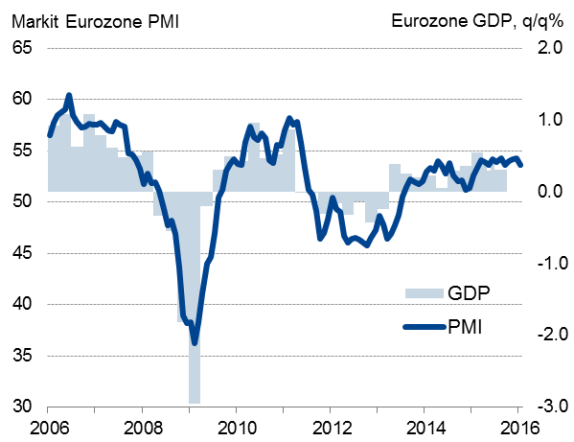

Eurozone growth figures will be updated for the fourth quarter, and are expected to confirm the ECB's view that the recovery remains disappointingly lacklustre. A 0.3-4% growth rate will round off a year in which the single-currency area grew by just 1.6%. Malaise and disinflationary pressures look to have extended into 2016, according to the region's PMI survey data, which has heightened the chances of the central bank taking further action to stimulate the economy during its March meeting.

Eurozone economic growth

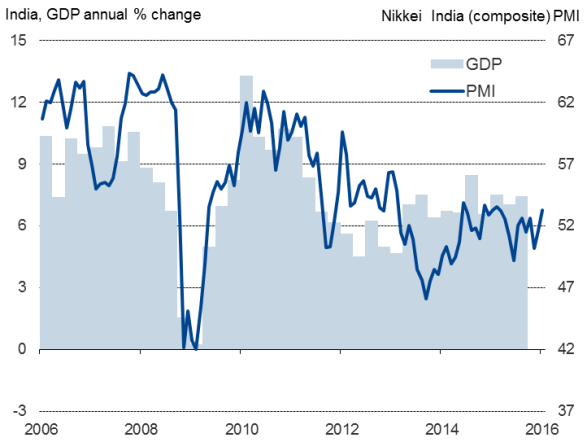

India is the focus for emerging market watchers, releasing its fourth quarter GDP data. The economy looks likely to have lost momentum after achieving growth of 7.4% in the third quarter, hit by waning global demand as well as extensive flooding at the end of the year. Although January's Nikkei PMI surveys already point to a rebound in activity, growth remained well below the pace seen a year ago, suggesting India may struggle to meet the 7.3% growth rate projected by the IMF in its latest outlook for 2015-2016.

India economic growth

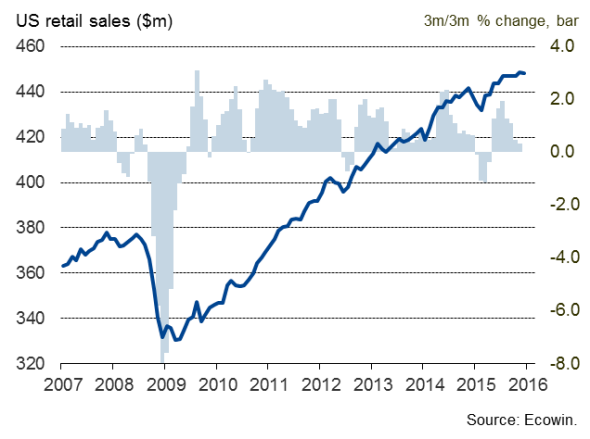

In the US, retail sales will be watched for evidence that consumers are helping to sustain the upturn. Rising sales of consumer goods and services formed an important aspect of the US's growth last year, as unemployment fell to an eight year low, wage growth crept higher and low oil prices freed up disposable incomes. However, retail sales growth slowed towards the end of the year, with spend even dipping slightly in December. January therefore looks set to see a rebound, but any signs of weakness will send another signal that the Fed will pause on further rate hikes.

US retail sales

Other key data releases include German, French, Italian and Eurozone industrial figures, as well as German trade and inflation data plus industrial production and construction output data for the UK.

Monday 08 February

The start of the week sees the release of Japanese bank lending data for January, as well as December's current account figures.

Q4 GDP figures for India will be published.

Data on Russia's foreign trade are released.

Manufacturing output figures for South Africa become available.

The eurozone Sentix Index is issued.

English regions & Wales PMI, as well as Scotland's PMI, is released.

The US publishes data on employment trends as well as its Labor Market Conditions Index.

Tuesday 09 February

Information on unemployment in South Africa are announced.

Latest industrial output figures for Germany and Greece are released alongside data on the German current account and trade balance.

The Business Optimism Index for the US is distributed.

Wednesday 10 February

In Australia, consumer sentiment figures are published.

Money supply data for China are released.

Information on the Russian budget is made available.

Industrial output numbers in France, Italy and the UK are released, along with UK manufacturing figures.

An announcement on Brazilian capital flows will be made.

Thursday 11 February

In Germany, the Wholesale Price Index will be released.

Latest unemployment rate figures for Greece become available.

Canada's New Housing Price Index is out.

The US makes an announcement on it's Federal budget on Thursday.

Friday 12 February

A busy day for Indian data releases, as figures for December's industrial output, CPI data for January, foreign reserves numbers as well as trade deficit statistics are published.

Eurozone industrial production and GDP data are made available.

Consumer price figures are meanwhile issued in Germany.

Latest data on Spanish inflation is announced.

Figures on the United Kingdom's construction output are issued by the Office for National Statistics.

Finally, the week is brought to a close with the release of US retail sales numbers.

Chris Williamson | Chief Business Economist, IHS Markit

Tel: +44 20 7260 2329

chris.williamson@ihsmarkit.com

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f05022016-Economics-Week-Ahead-Economic-Overview.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f05022016-Economics-Week-Ahead-Economic-Overview.html&text=Week+Ahead+Economic+Overview","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f05022016-Economics-Week-Ahead-Economic-Overview.html","enabled":true},{"name":"email","url":"?subject=Week Ahead Economic Overview&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f05022016-Economics-Week-Ahead-Economic-Overview.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Week+Ahead+Economic+Overview http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f05022016-Economics-Week-Ahead-Economic-Overview.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}