Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

May 04, 2017

PMI surveys see UK growth kick higher at start of second quarter

UK business activity growth gained momentum for a second successive month in April, according to PMI survey data. Order book and employment growth also accelerated. The improvement in the survey data indicates that economic growth has revived after having slowed sharply in the first quarter of the year.

However, consumer-facing sectors continued to struggle and prices rose at a rate not seen since the collapse of Lehman Brothers nearly nine years ago, adding to worries that rising inflation could limit the ability of the economy to sustain strong growth in coming months.

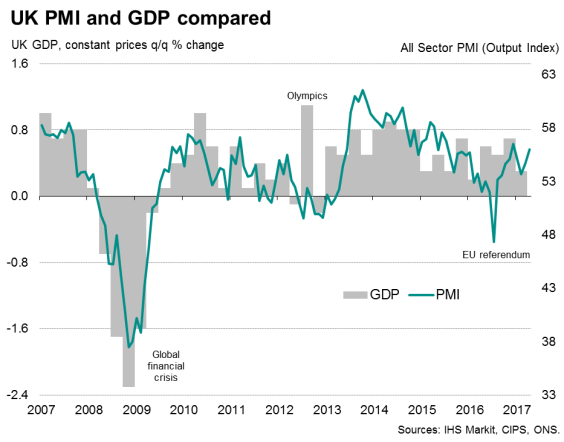

0.6% GDP growth signalled at start of Q2

The Markit/CIPS all-sector PMI rose to a four-month high of 56.0 in April from 54.6 in March. The latest reading is the second-highest in the past 21 months.

The elevated level of the PMI means the second quarter could in fact see GDP growth accelerate from the 0.3% expansion seen in the first quarter. Historical comparisons suggest that the April PMI is indicative of the economy growing at a quarterly rate of 0.6%. If sustained, the strength in the survey data pose upside risks to IHS Markit's current forecast of 0.4% GDP growth in the second quarter.

Encouragingly, April saw business activity growth accelerate across the three main sectors of the economy. Service sector and construction industry growth rates rose to the highest so far this year, while manufacturing output growth strengthened markedly to reach its fastest for three months.

The survey also found inflows of new business rising at the fastest rate for four months, accelerating in all three main sectors. Backlogs of work meanwhile accumulated to the joint-greatest extent in almost two years as firms struggled to deal with high volumes of new orders.

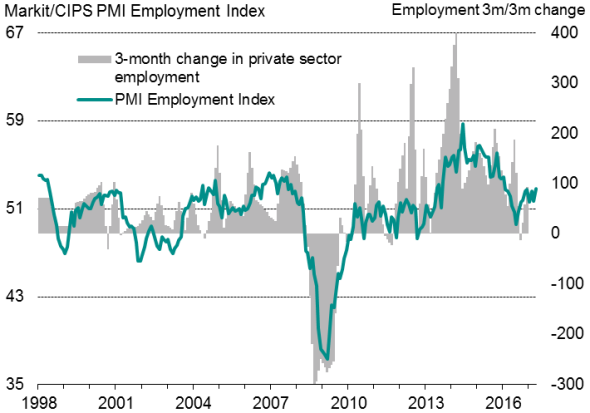

Employment was consequently raised to a degree not beaten since the start of 2016 as firms sought to boost capacity in line with the increased order book workflow.

UK employment

Policy outlook

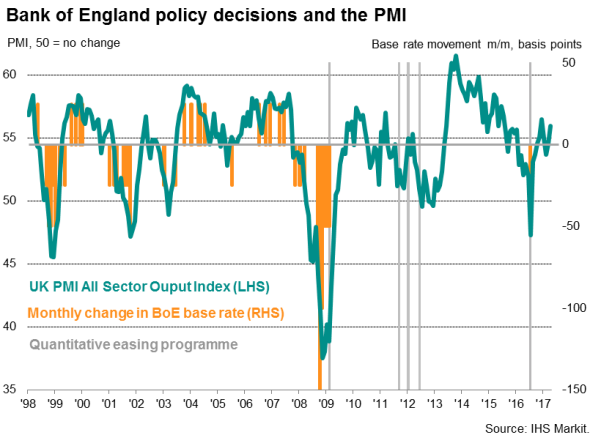

The upturn in business activity growth pushes the PMI back into territory that would normally be associated with the Bank of England turning increasingly hawkish, and will bolster the arguments of policymakers already making a case for higher interest rates.

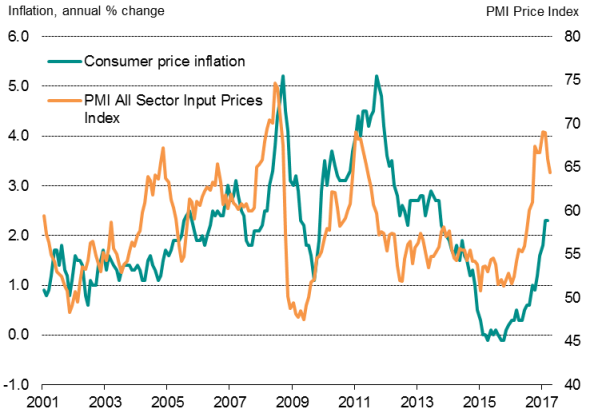

Calls for higher interest rates will also be given weight by the survey showing average prices charged for goods and services rising at the fastest rate since September 2008. Higher selling prices were widely attributed to the need to pass increased costs onto customers, in turn partly linked to the weak exchange rate driving import costs higher.

The survey data therefore suggest that consumer price inflation has further to rise from its current 2.3% pace in coming months. However, an easing in the rate of input cost inflation in April to the lowest since last September suggests that upward input cost pressures may have peaked.

UK inflation

Unbalanced growth

Despite the stronger headline numbers, the survey data also raise doubts over the ability of the economy to continue to grow at this pace. Drill down further and growth is clearly unbalanced, with consumer-facing sectors struggling amid higher prices and subduing the overall pace of expansion.

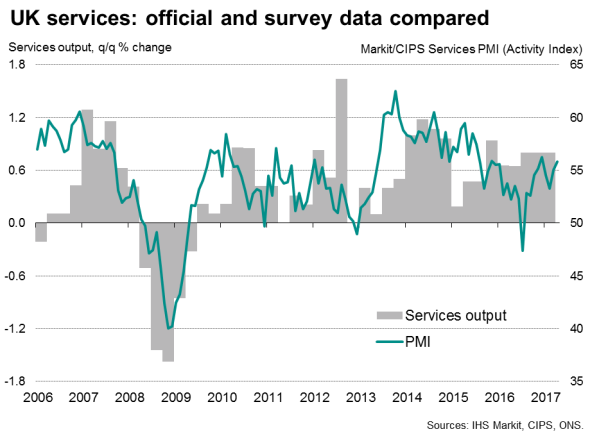

In the services survey, activity growth was subdued among hotels & restaurants and other consumer-facing service providers (based on a three-month average). These weak spots were offset by accelerating growth in computing & IT and transport, as well as ongoing robust expansion in business services. These latter business-facing companies were boosted in part by strong manufacturing sector growth.

The goods-producing sector in fact saw a marked strengthening of output growth, linked by many firms to a solid bounce in new export orders. The weak sterling exchange rate reportedly helped manufacturers benefit from stronger global economic expansion, especially in the eurozone, which is enjoying its best growth spell for six years.

Within manufacturing, it was producers of consumer goods that saw the weakest PMI reading, with producers of investment goods such as plant and machinery recording the strongest growth. However, much of the latter's gain was linked to foreign orders.

Within construction, the weakest expansion was seen in commercial building activity, suggesting that investment in fixed assets such as offices, retail space and industrial units has almost stalled.

Uncertain outlook

Perhaps most significantly, firms' expectations about future activity levels slipped to a five-month low, led down especially by weaker expectations of growth in the service sector.

While the headline April PMI surveys provide strong evidence to suggest that economic growth could pick up again in the second quarter, weak growth in the consumer sector remains a concern, and is something which could intensify in coming months as consumer prices rise further.

Chris Williamson | Chief Business Economist, IHS Markit

Tel: +44 20 7260 2329

chris.williamson@ihsmarkit.com

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f04052017-Economics-PMI-surveys-see-UK-growth-kick-higher-at-start-of-second-quarter.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f04052017-Economics-PMI-surveys-see-UK-growth-kick-higher-at-start-of-second-quarter.html&text=PMI+surveys+see+UK+growth+kick+higher+at+start+of+second+quarter","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f04052017-Economics-PMI-surveys-see-UK-growth-kick-higher-at-start-of-second-quarter.html","enabled":true},{"name":"email","url":"?subject=PMI surveys see UK growth kick higher at start of second quarter&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f04052017-Economics-PMI-surveys-see-UK-growth-kick-higher-at-start-of-second-quarter.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=PMI+surveys+see+UK+growth+kick+higher+at+start+of+second+quarter http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f04052017-Economics-PMI-surveys-see-UK-growth-kick-higher-at-start-of-second-quarter.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}