Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Sep 03, 2015

Eurozone growth hits four-year high despite stalling French economy

The final Markit Eurozone PMI" rose to 54.3 in August, up from 53.9 in July, and above the earlier flash estimate. The data signalled the fastest pace of expansion since May 2011.

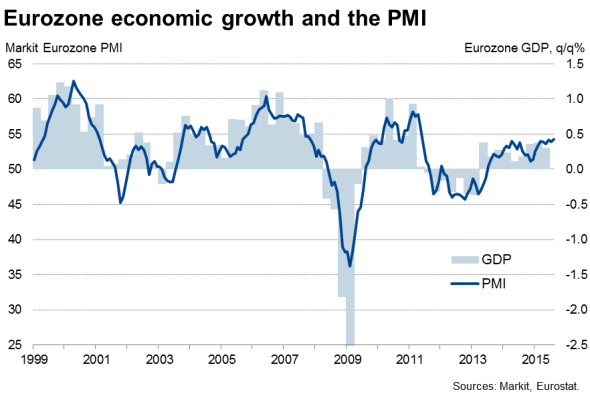

Growth at four-year high

The survey data suggest that, although global economic worries have intensified in recent weeks, the calming of "Grexit" fears has led to an improvement in the business environment across the eurozone, pushing the pace of economic growth to its fastest for over four years in August. The PMI is indicating euro area GDP growth close to 0.4% in the third quarter, a solid, albeit unspectacular rate of expansion.

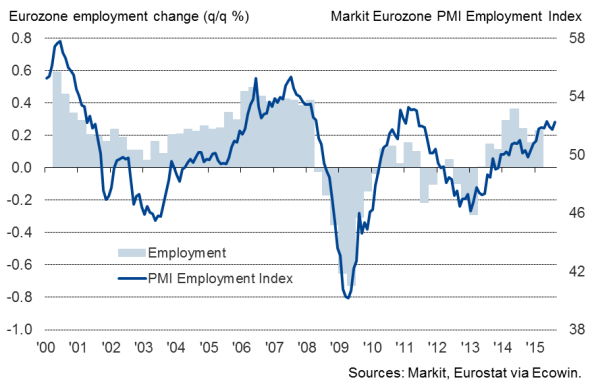

The rate of job creation across the eurozone also accelerated to one of the fastest seen over the past four years as companies prepared for further growth in coming months, adding to signs of an increasingly sustainable-looking upturn.

Employment

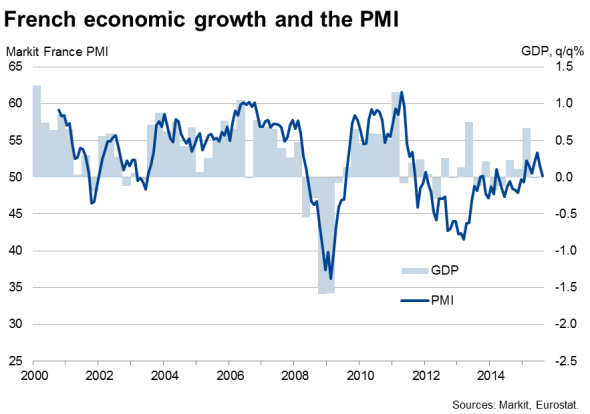

France left behind in upturn

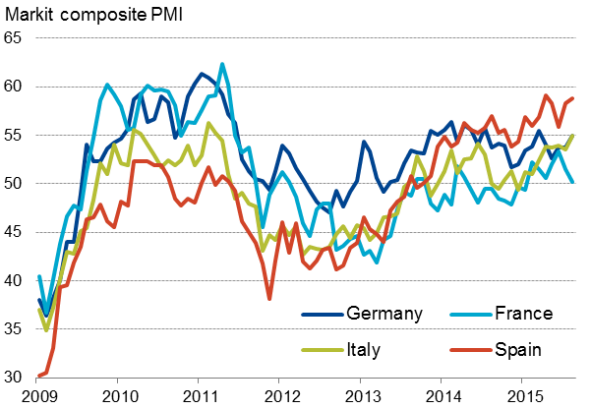

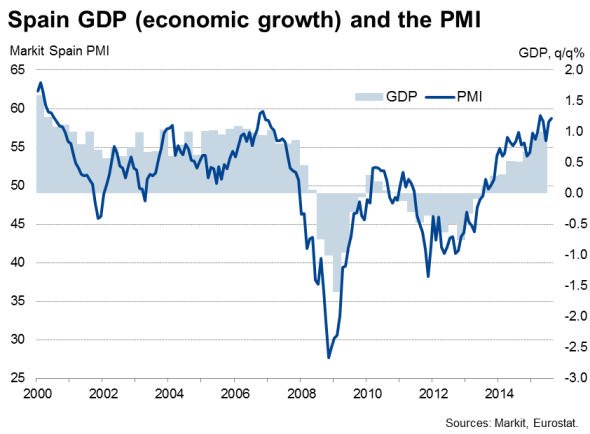

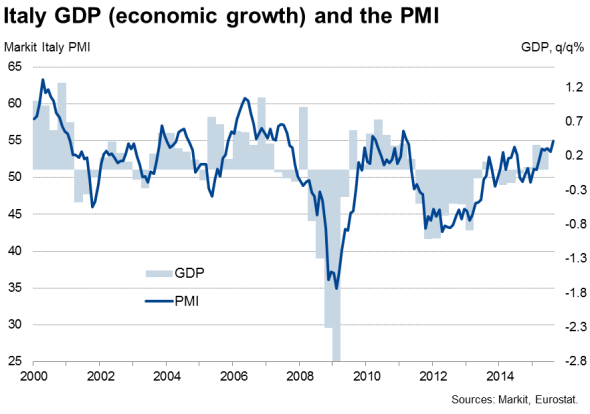

The upturn was stronger than estimated by the flash reading, thanks mainly to stronger growth in Germany and the best performance for over four years in Italy, where PMIs of 55.0 are pointing to 0.5% GDP growth in the third quarter in both cases. But it is Spain that remains the star performer among the largest eurozone countries, with a PMI of 58.8 adding to signs of another 1.0% GDP growth spurt in the third quarter.

Eurozone "big four'

A worrying deterioration of growth in France highlighted a major concern about the lack of demand in the region's second-largest economy. The French PMI dropped below the earlier flash reading to just 50.2, signalling a near-stagnation of the economy in the third quarter.

Lower inflation outlook

The ECB will probably be reassured by the ability of the eurozone economy as a whole to withstand recent headwinds. That said, policymakers have little scope for complacency, however, as slower growth in the emerging markets, recent financial market volatility and a stronger euro have the potential to hit the economy's performance in coming months and will also keep inflation lower then the ECB had been anticipating. The PMI survey's measure of firms' selling prices stabilised, the first time since March 2012 that prices have not been cut. However, the gauge of input costs was down to a six-month low in August, with manufacturers' input prices falling, suggesting pipeline inflationary pressures have eased again.

Chris Williamson | Chief Business Economist, IHS Markit

Tel: +44 20 7260 2329

chris.williamson@ihsmarkit.com

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f03092015-Economics-Eurozone-growth-hits-four-year-high-despite-stalling-French-economy.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f03092015-Economics-Eurozone-growth-hits-four-year-high-despite-stalling-French-economy.html&text=Eurozone+growth+hits+four-year+high+despite+stalling+French+economy","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f03092015-Economics-Eurozone-growth-hits-four-year-high-despite-stalling-French-economy.html","enabled":true},{"name":"email","url":"?subject=Eurozone growth hits four-year high despite stalling French economy&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f03092015-Economics-Eurozone-growth-hits-four-year-high-despite-stalling-French-economy.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Eurozone+growth+hits+four-year+high+despite+stalling+French+economy http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f03092015-Economics-Eurozone-growth-hits-four-year-high-despite-stalling-French-economy.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}