Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Jul 01, 2015

World's factories report worst quarter for two years amid Asian downturn

Global manufacturing activity slowed and edged closer towards stagnation in June. The JPMorgan PMI", compiled by Markit, fell to 51.0 from 51.3 in May, matching April's 21-month. The average PMI reading for the second quarter is the weakest seen for two years.

Global factory output growth slowed in June to the weakest since July 2013, and the rate of order book growth moderated to one of the slowest seen over the past two years, albeit with worldwide export orders picking up slightly for the first time in three months.

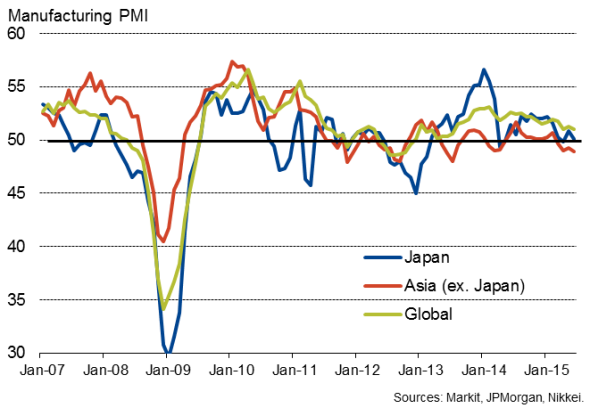

Global factory output

Asia sees steepest downturn for 2" years

Asia once again lay at the heart of global manufacturing weakness. Asian factories reported a fourth successive monthly deterioration of business conditions in June, with the rate of decline accelerating to the joint-fastest since July 2013. All Asian PMI surveys either signalled contraction or slower rates of growth. The steepening downturn in June finishes off the worst quarter for Asian manufacturing since the final quarter of 2012.

Asia subdues global growth

Despite huge stimulus and a depreciated yen, Japan's manufacturing economy remains in the doldrums. At 50.1, the Nikkei Manufacturing PMI declined from 50.9 to signal near-stagnation. Although export orders picked up, domestic demand fell at an increased rate.

The flat picture in Japan accompanied a decline in manufacturing elsewhere across Asia, where the PMI signalled the largest drop in activity for nearly two years. At 49.4, the HSBC China Manufacturing PMI was one of the lowest readings seen over the past year, but it was in Taiwan and South Korea that the most severe downturns in the world were seen, with PMI readings down to 46.3 and 46.1 respectively, their lowest since September 2012.

Indonesia's manufacturing economy also contracted, albeit at the weakest rate for five months, and rates of growth slowed to disappointingly modest rates in both India and Vietnam.

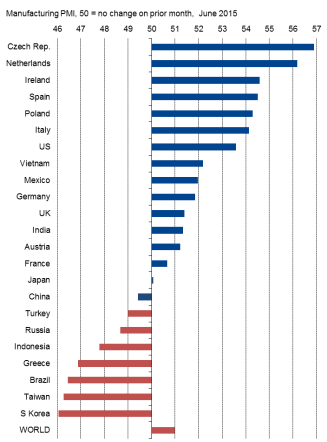

June manufacturing PMI rankings

Sources: Markit, JPMorgan, Nikkei, HSBC.

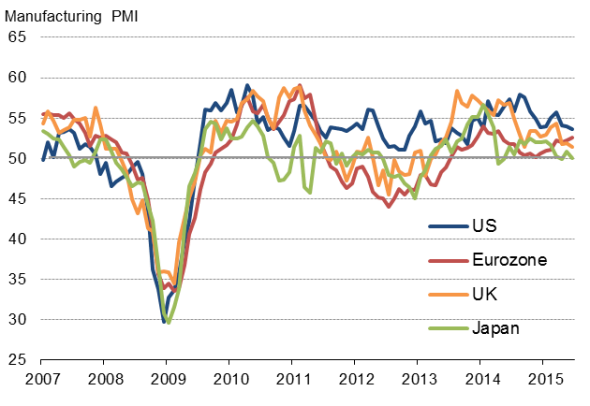

Strong exchange rates linked to US and UK factory slowdowns

The weak global PMI number for June also reflected slower growth in the US, where the Markit PMI fell to a 20-month low of 53.6, dropping for a third successive month. Robust domestic demand was offset by a third monthly fall in exports (although only modest), reflecting the loss of competitiveness caused by the strong dollar.

The loss of US growth momentum is a concern, as the world's largest economy has been acting as the main engine of global economic expansion over the past two years. Clear knock-on effects were reported in both Brazil and Mexico, where PMI surveys signalled an ongoing steep contraction and slower growth respectively.

The UK is another country that has outperformed in recent years but, like the US, saw growth slide in June. The Markit/CIPS PMI fell to 51.4, its lowest for just over two years. Companies commonly reported the appreciation of sterling to have hit exports, which showed the joint-largest monthly fall since January 2013.

Main developed economies

Sources: Markit, Nikkei, CIPS.

Eurozone brightens

The Asian downturn and slower growth in the US and UK contrasted with an upturn in the euro area, where factories reported the largest upturn in activity for over a year. At 52.5, the Markit Eurozone PMI hit a 14-month high.

All euro area countries expanded (including France, for the first time in over a year) with the notable exception of Greece, where the escalating debt crisis has led to the steepest downturn in activity for two years over the second quarter as a whole.

The recent improvement in euro area business conditions was further highlighted by four of the top six fastest growing manufacturing economies all sitting within the euro zone, led by the Netherlands, followed by Ireland, Spain and then Italy.

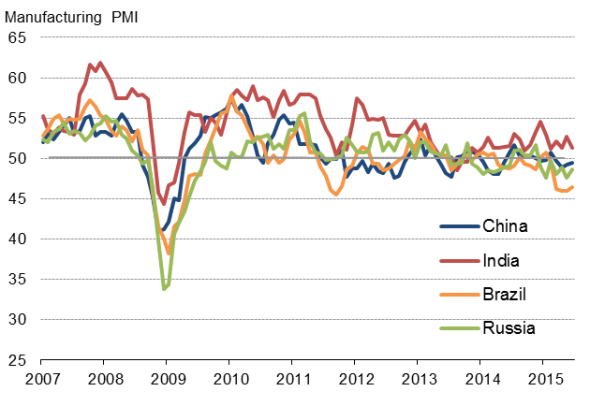

Eastern Europe benefits from Eurozone

The gathering euro area upturn is also benefitting neighbouring countries, helping push the Czech Republic to the top of the global manufacturing rankings, with Poland in fifth place. However, growth in eastern Europe as a whole remained only modest, restrained by a further downturn in Russia, where the PMI reading of 48.7 signalled a seventh successive monthly downturn in activity.

Main emerging markets

Sources: Markit, JPMorgan, Nikkei, HSBC.

Chris Williamson | Chief Business Economist, IHS Markit

Tel: +44 20 7260 2329

chris.williamson@ihsmarkit.com

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f01072015-Economics-World-s-factories-report-worst-quarter-for-two-years-amid-Asian-downturn.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f01072015-Economics-World-s-factories-report-worst-quarter-for-two-years-amid-Asian-downturn.html&text=World%27s+factories+report+worst+quarter+for+two+years+amid+Asian+downturn","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f01072015-Economics-World-s-factories-report-worst-quarter-for-two-years-amid-Asian-downturn.html","enabled":true},{"name":"email","url":"?subject=World's factories report worst quarter for two years amid Asian downturn&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f01072015-Economics-World-s-factories-report-worst-quarter-for-two-years-amid-Asian-downturn.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=World%27s+factories+report+worst+quarter+for+two+years+amid+Asian+downturn http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f01072015-Economics-World-s-factories-report-worst-quarter-for-two-years-amid-Asian-downturn.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}