S&P Global — 2 Dec, 2021 — Global

Daily Update: December 2, 2021

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

With energy prices that have ricocheted between highs and lows in recent months, a return to normalcy seems unlikely before year-end. Geopolitical and market constraints intensified by differing demand fundamentals have had effects on the cost of energy commodities including oil, natural gas, liquified natural gas, coal, and electric power. S&P Global Ratings expects prices to remain strong with possible spikes into next year, likely to moderate sometime in 2022. However, political intervention that could deter investment in energy markets, a power supply surge potentially upending stabilization, and the uncertainty of prolonged price volatility all pose risks to that outcome, according to the outlook. Recently, energy markets have tumbled. The commodities benchmark S&P GSCI declined 10.8% in November, pushed by concerns about the implications of Omicron on demand, continued global supply-chain pressures, and coordinated releases of strategic petroleum reserves, according to S&P Dow Jones Indices. High energy prices have become a key contributor to inflation and are casting a shadow over the global economy’s post-pandemic recovery—which is now confronting the Omicron coronavirus variant. High energy prices could also pose problems for immediate action on the global energy transition from fossil fuels to renewable energy by making the switch costlier. “If 2021 was the year of the big rebound, with COVID-19 vaccines fueling a robust economic recovery and steadily improving credit markets, the recent emergence of the Omicron variant has offered a stark reminder that we have not yet beaten the virus,” Alexandra Dimitrijevic, managing director and global head of analytical research and development at S&P Global Ratings, said in S&P Global Ratings’ 2022 global credit conditions outlook. “More than COVID, persistently high inflation, fueled by supply-chain disruption and soaring energy prices, could be the primary setback derailing a still fragile recovery in 2022.” Still, as we enter 2022, favorable financing conditions and a powerful economic recovery are underpinning a largely positive credit momentum—pointing to a steady overall ratings performance, with fewer downgrades and low default rates at around 2.5%, according to the outlook. “In our view, credit momentum will remain positive, with financing conditions still heavily underwritten by supportive fiscal and monetary policy, and economic growth easing back to a more sustainable pace,” Ms. Dimitrijevic said. “Nevertheless, the recovery’s foundations are relatively fragile and vulnerable to setbacks.” Today is Thursday, December 2, 2021, and here is today’s essential intelligence.

Uncertainty in the Global Economy

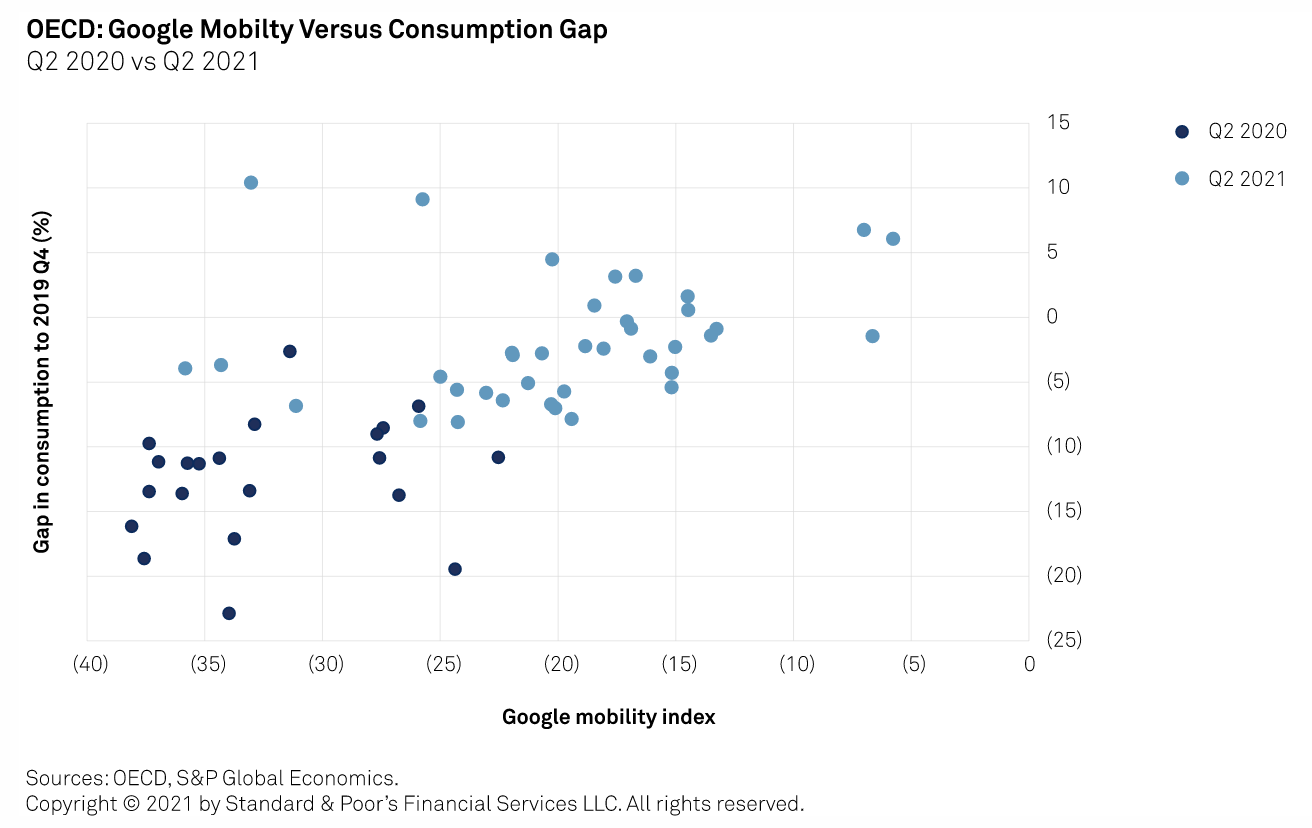

Economic Outlook Q1 2022: Rising Inflation Fears Overshadow A Robust Rebound

COVID-19 is definitely still with us, but the economic impact is fading. The pandemic continues to rage in some parts of the world, defying the comforts of high vaccination rates and confounding pronouncements that we may be nearing the exit. Europe is in the midst of its fourth COVID-19 wave, with the incidence skewed toward those countries and regions where effective vaccination is lightest; some lockdowns have been re-imposed.

—Read the full report from S&P Global Ratings

Economic Outlook Emerging Markets Q1 2022: Recovery Isn't Yet Complete While COVID-19 And Inflation Risks Remain Front And Center

Nearly two years into the pandemic, COVID-19 cases continue to ebb and flow, playing a central role in global economic activity. Nonsynchronous peaks and troughs of pandemic waves across core EMs have meant that the recovery is proceeding at varying and choppy speeds.

—Read the full report from S&P Global Ratings

Economic Research: Eurozone Economic Outlook 2022: A Look Inside The Recovery

S&P Global Ratings believes the recent rise in COVID-19 cases in some European countries will somewhat slow the recovery in consumption but still allow the eurozone economy to surpass pre-pandemic levels of activity in fourth-quarter 2021. Some governments—such as in Austria, the Netherlands, and Belgium—are imposing some restrictions to economic activity, which are dampening consumer-facing businesses.

—Read the full report from S&P Global Ratings

COVID Vaccine-Makers Race To Test Jabs On Omicron Variant Over Efficacy Concerns

COVID-19 vaccine-makers are racing to meet growing demand and address concerns about the effectiveness of their shots against the emerging omicron variant. Moderna Inc., Pfizer Inc., and BioNTech SE all said they will have data on how their vaccines fare against the new variant over the next two to four weeks, with updated vaccines targeting the new strain also in development.

—Read the full article from S&P Global Market Intelligence

The Credit Cycle

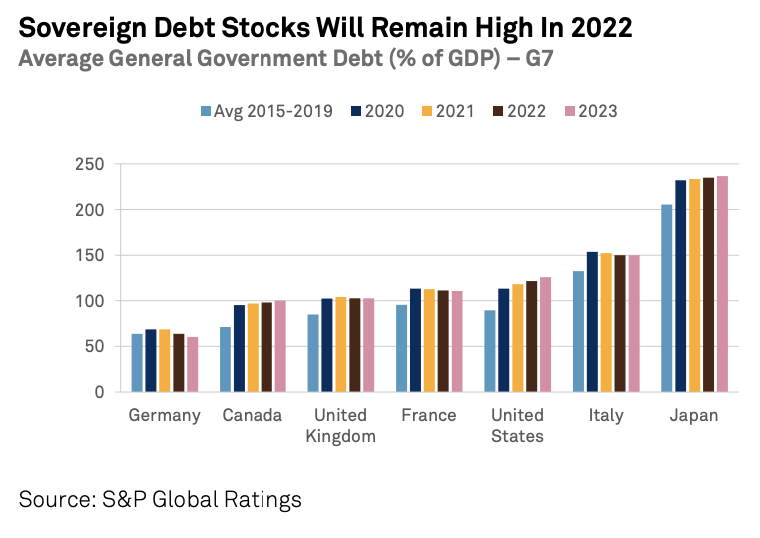

Global Credit Outlook 2022: Aftershocks, Future Shocks, And Transitions

The world enters 2022 with largely positive credit momentum, reflecting favorable financing conditions, and a powerful economic recovery. This could be derailed if persistently high inflation pushes central banks to aggressively tighten monetary policy, triggering significant market volatility and repricing risks.

—Read the full report from S&P Global Ratings

Credit Conditions: Asia-Pacific: China Slows, A Chill Wind Blows

The omicron variant threatens the reimposition of mobility and travel restrictions, just as Asia-Pacific authorities are seeking to reopen their economies. Meanwhile, China and Hong Kong’s zero-COVID policy underpins localized lockdowns and tight border restrictions. Still soft domestic consumption and dependence of exports points to uneven recovery patterns among geographies and industry sectors.

—Read the full report from S&P Global Ratings

Credit Conditions: Europe: Reining In As Full Recovery Nears

Strong demand and falling unemployment create a fundamentally positive outlook for credit in 2022, although cost pressures, monetary policy tightening, and Europe’s fourth COVID-19 wave, now compounded by omicron, are headwinds to monitor.

—Read the full report from S&P Global Ratings

Credit Conditions: North America: As Recovery Rolls On, Inflation Risks Remain

Credit conditions remain largely favorable, although risks are looming—primarily those around inflation pressures and supply disruptions (including labor shortages) that many borrowers face. The potential for coronavirus variants such as omicron adds another layer of uncertainty about the pandemic and its effects on the economy and credit.

—Read the full report from S&P Global Ratings

Fed Risks Liquidity Crisis As It Manages Withdrawal From Treasury Market

The Federal Reserve may never be able to fully extricate itself from a Treasury market that is now too big for traditional liquidity providers to meet demand in times of stress. The Fed has been a major buyer of government bonds since March 2020, when financial markets froze in the face of COVID-19.

—Read the full article from S&P Global Market Intelligence

Credit Conditions: Emerging Markets: Inflation, The Unwelcome Guest

Risks are increasing for emerging markets as inflation keeps accelerating in many key countries, adding to existing challenges. On the bright side, higher prices are partly fueled by the strong economic rebound. COVID-19's economic impact is decreasing and vaccinations are progressing, but the recent emergence of the omicron variant threatens the positive momentum.

—Read the full report from S&P Global Ratings

Banking Industry Under Pressure

German, Swiss Banks Among Least Efficient In Europe During Q3

Germany and Switzerland's biggest banks were among the least efficient in Europe in the third quarter, S&P Global Market Intelligence data shows. Of a sample of 37 European banks, Deutsche Bank AG was the least efficient as measured by its cost-to-income ratio at 86.01%, which was a 45-basis-point improvement from the year-ago 86.46%.

—Read the full article from S&P Global Market Intelligence

Banks Seek To Keep Employees Happy In Hong Kong Via Quarantine Support Plan

Morgan Stanley, JPMorgan Chase & Co., and The Goldman Sachs Group Inc. will reimburse up to about US$5,000 in quarantine expenses for employees who return from a personal trip to the city that has faced criticism for currently having one of the strictest COVID-19 control strategies in the world. Some companies in other sectors have also announced similar plans.

—Read the full article from S&P Global Market Intelligence

Technology & Media

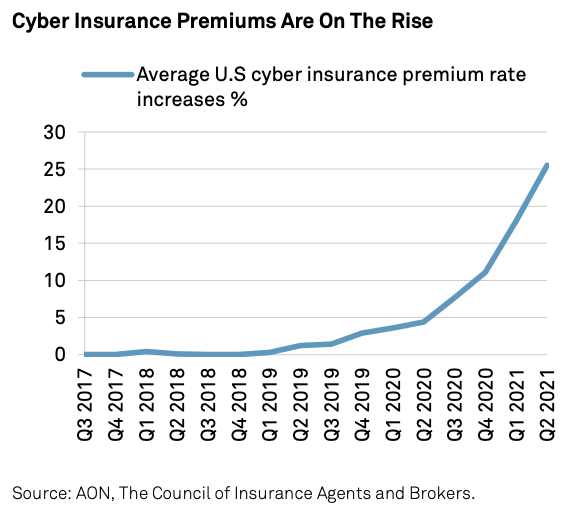

Cyber: Are Credit Markets Ready For A Systemwide Attack?

The number of credit relevant cyber-attacks will keep rising. Most of the rating actions linked to cyber risks have followed direct attacks on specific entities. Often, those attacks led to a meaningful balance-sheet event, business disruption, and a risk of long-lasting reputation damage.

—Read the full report from S&P Global Ratings

Digitalization: Will DeFi Destabilize Finance?

DeFi will continue to complement, not supplant, traditional finance in 2022. This new financial ecosystem uses smart contracts on blockchains instead of central financial intermediaries to offer financial products and services. S&P Global Ratings believes it will continue evolving in 2022 toward complementing the current financial system rather than substituting financial services companies.

—Read the full report from S&P Global Ratings

Crypto Assets: Evolution Or Revolution?

Adoption of cryptocurrencies will continue to gather pace. As of Nov. 11, 2021, their total market capitalization was around $2.8 trillion—about 6% of the U.S. equity market. Around 45 corporates have taken positions on cryptocurrencies (bitcoin and Ethereum), totaling around $24 billion.

—Read the full report from S&P Global Ratings

AT&T Exec Says Concerns Around Mid-Band Spectrum Delay 'Overblown'

With a plan in place to address the Federal Aviation Administration's concerns, an AT&T Inc. executive said the company stands ready to deploy a key portion of mid-band spectrum with no negative impact from its recent concessions. In a recent letter to the Federal Communications Commission, AT&T and Verizon Communications Inc. pledged to take additional steps to minimize energy coming from 5G base stations, especially those near public airports and heliports.

—Read the full article from S&P Global Market Intelligence

Twitter CEO Change 'Pivotal' As New Chief Confronts Stalling User Growth

After Twitter Inc. CEO Jack Dorsey confirmed his resignation from the company, investor groups and analysts said the leadership change is a net positive for the microblogging platform as it seeks to expand its user base and product offerings.

—Read the full article from S&P Global Market Intelligence

ESG in the Time of COVID-19

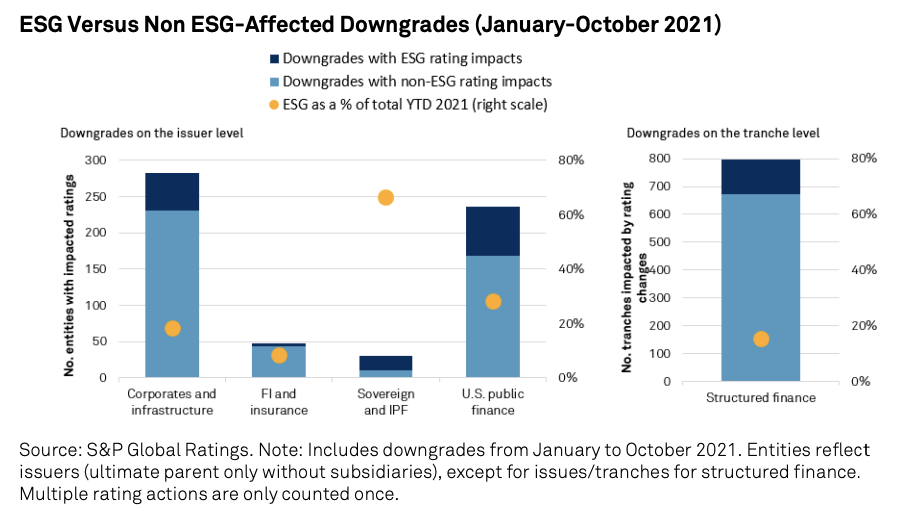

Climate Risks: How Far Will They Affect Credit?

Elevated unmitigated exposure to climate risks will continue to affect credit quality. The past year has seen an unprecedented number of rating actions triggered by disruption and uncertainty over unexpected costs from severe climatic events, such as hurricanes, wildfires, and droughts.

—Read the full report from S&P Global Ratings

Energy Transition: How Will Climate Policies Speed Up Change?

In Europe, soon-to-be decided "Fit for 55" targets will likely yield important changes. For example, S&P Global Ratings anticipates annual renewable capacity additions will need to reach 45 gigawatts (GW) to 55 GW per annum versus 30 GW in 2020. Carbon-intensive industries, such as steel, cement, and chemicals, may need to adjust strategies and step up spending on environmentally focused projects.

—Read the full report from S&P Global Ratings

Nature Risks: At What Price?

Governments now see the decline of nature as a key policy matter. Big policy shifts, though with distant targets, could trigger regulation in 2022 to set the world on the right trajectory to arrest the decline in biodiversity. At COP 26, dubbed the “Nature COP,” global leaders announced a target of halting and reversing forest loss and land degradation by 2030.

—Read the full report from S&P Global Ratings

Platts Nature-Based Avoidance, Removals Carbon Credits Spread Reaches All-Time Low

There has been a significant narrowing of the spread between avoidance and removals carbon credits in the nature-based segment. On Nov. 30, the spread between the Platts nature-based avoidance assessment, which reflects avoidance credits, and the Platts natural carbon capture assessment, which reflects removals credits, was the narrowest ever at just 90 cents.

—Read the full article from S&P Global Platts

NiSource Sticks With Gas, Renewables In 'Balanced' Approach To Energy Transition

Members of Indiana-headquartered utility NiSource Inc.'s management team believe investments in natural gas infrastructure could prove just as critical as improvements to the electrical grid when it comes to achieving the sector's clean energy transition, advocating for a broad path to achieving the nation's climate and energy goals.

—Read the full article from S&P Global Market Intelligence

'New Global Energy Economy' Emerging As IEA Ups Clean Power Forecasts

2021 is set to be another record year for renewable energy installations, with 290 GW of new capacity expected to be built globally, the International Energy Agency said Dec. 1 in its annual Renewables Market Report.

—Read the full article from S&P Global Market Intelligence

The Future of Energy & Commodities

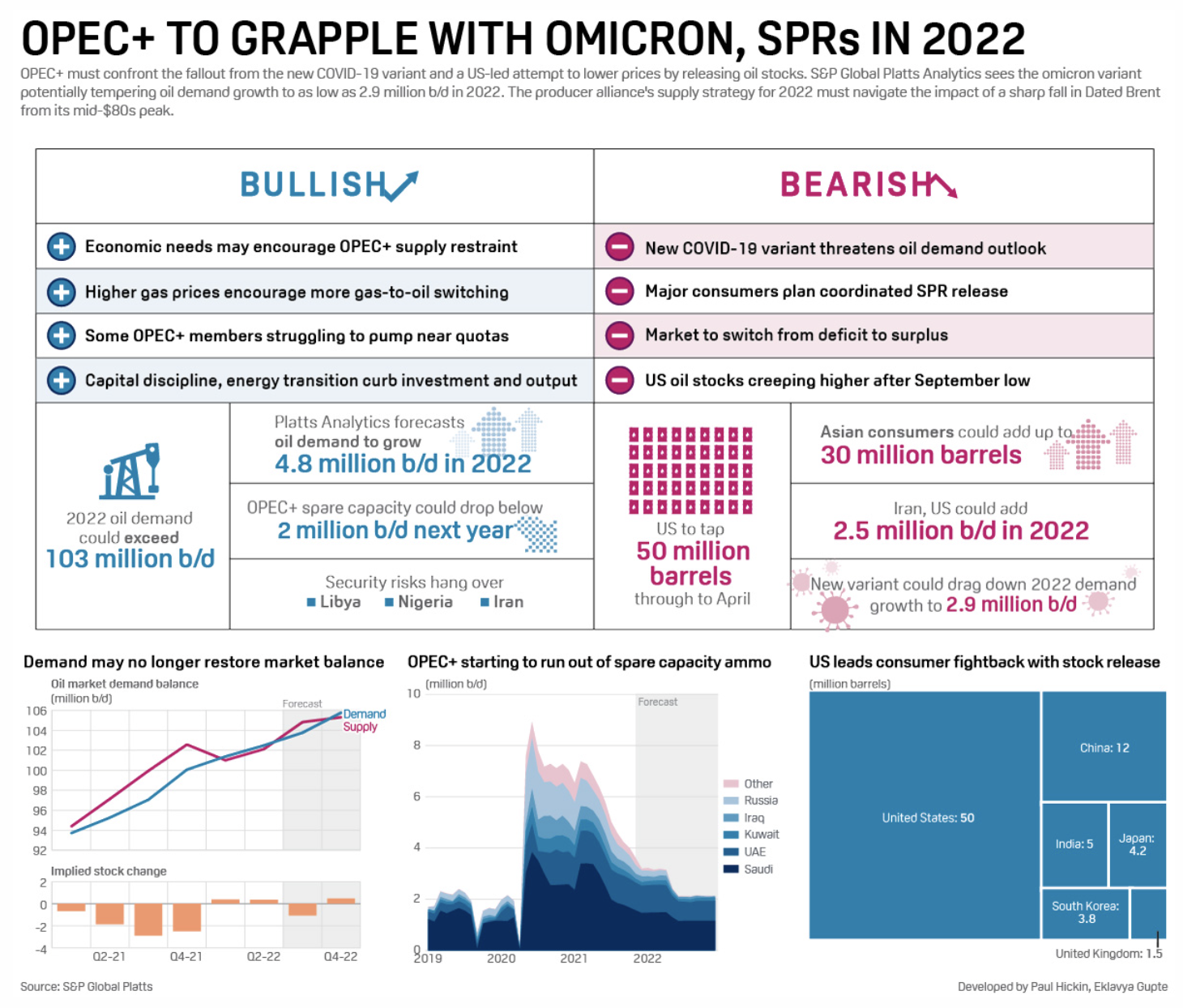

Infographic: OPEC+ To Grapple With Omicron, SPRs In 2022

OPEC+ must confront the fallout from the new COVID-19 variant and a U.S.-led attempt to lower prices by releasing oil stocks. S&P Global Platts Analytics sees the omicron variant potentially tempering oil demand growth to as low as 2.9 million b/d in 2022. The producer alliance's supply strategy for 2022 must navigate the impact of a sharp fall in Dated Brent from its mid-$80s peak.

—Read the full article from S&P Global Platts

OPEC+ Deliberates On January Oil Output Targets As U.S. Lays On Pressure

For months, OPEC and its Russia-led allies have stuck firm to a measured easing of production quotas, even amid a surge in oil prices and a chorus of complaints from the U.S. and other key customers calling for more crude. Now, with winter set to flip the market into surplus and coronavirus concerns weighing on the global economy, OPEC+ ministers are assessing whether to pause the alliance's next scheduled increase of 400,000 b/d for January.

—Read the full article from S&P Global Platts

Feature: Brazilian Biodiesel Spot Prices Will Fall On Reduced Blending Mandate

On the first working day after the Brazilian biodiesel blending mandate was reduced from 13% to 10% for 2022, the biodiesel spot price was unchanged, though market participants expect lower offers in the coming days. Market participants said the biodiesel spot price could drop nearly Real 150/cu m, or $26.79/cu m, in the near future.

—Read the full article from S&P Global Platts

Written and compiled by Molly Mintz.

Content Type

Location

Language