S&P Global — 23 Aug, 2023 — Global

Daily Update: August 23, 2023

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

War in Ukraine Drives LNG Import Demand, Restructuring of Gas Markets

In July, a ship carrying liquefied natural gas was turned away from the port of Bahía Blanca, Argentina, because it carried supplies from Russia, which has come under international sanctions since its invasion of Ukraine in early 2022.

A source from Argentinian state-owned energy company Energía Argentina told S&P Global Commodity Insights that the state-owned bank in charge of paying for the supplies, Banco de la Nación Argentina, halted the offloading of the cargo — which came from Geneva-based commodity trading company Gunvor — after discovering that the gas was from Russia.

“We took the decision in the face of international sanctions against certain Russian companies,” Argentina Economy Minister Sergio Massa said in a television interview.

The incident encapsulated the turmoil rippling through global LNG markets as the war in Ukraine continued and countries sought to secure their energy supplies while weaning themselves off fossil fuels in general, and Russian supplies specifically.

The loss of natural gas exported from Russia via pipelines represents about 3% of the global market, driving many countries, particularly in Europe, to turn to LNG to make up their heating and power generation supplies.

“Europe is responding by quickly building out its LNG processing infrastructure and regasification capacity, including floating storage,” wrote Thomas Watters, managing director and team lead for oil and gas at S&P Global Ratings.

With the addition of new LNG terminals under a crash building program, regasification capacity in the EU has reached almost 170 billion cubic meters — enough to replace lost Russian gas supplies, albeit at higher prices — according to Eurasia Group. Another 130 Bcm of new LNG import capacity is set to come online in the next few years, including more than 20 projects based on floating storage regasification units.

Japan, another country heavily dependent on imported LNG, agreed in July to collaborate with the EU on energy security by launching talks on the global LNG "architecture" and establishing a global early warning system to help ward off supply shocks and ensure stable supplies in future upheavals.

Still, with demand from Asia continuing to rise, the global spot LNG market will likely remain tight and prices will stay high until new capacity starts to come online in 2025–2026. The LNG supply shortage is not expected to subside until 2027.

The crisis has also helped facilitate a new wave of production and liquefaction capacity, particularly in the US. The US, Qatar and Australia account for approximately 60% of global LNG supply — a share expected to grow with the opening of new projects.

In the US, four large projects totaling 40 million metric tons per year are expected to be approved in 2023, including the $7.8 billion Plaquemines project and the Lake Charles project in Louisiana, and the Port Arthur and Rio Grande facilities in Texas. These additions will help US LNG capacity double by 2030 to 170 million metric tons per year, making the US the world’s largest supplier.

At the same time, some markets, particularly in East Asia, are seeking to reduce their dependence on imported LNG by building out renewable energy supplies. The governments of Japan, South Korea and Taiwan, which accounted for more than 40% of the LNG traded worldwide from 2015–2022, are focused on achieving their decarbonization goals and increasing their energy security by developing renewable sources such as wind, solar and nuclear. South Korea plans to reduce LNG's share of electricity generation to 9.3% by 2036, from 30% in 2021, while Japan‘s share of power generation from renewables has doubled to about 12% in the last six years.

All of this indicates that, whatever the outcome of the war in Ukraine, the LNG market is undergoing a fundamental restructuring — and the outlines of that market five or 10 years in the future are impossible to predict.

Today is Wednesday, August 23, 2023, and here is today’s essential intelligence.

Written by Richard Martin.

Economy

US Weekly Economic Commentary: Odds Of More Fed Tightening

A series of strong economic reports over the past week led us to significantly revise up our forecast of GDP growth in the third quarter. A surprisingly strong retail sales report for July was responsible for most of the upward revision as consumers continue to spend freely, apparently feeling financially secure in a tight labor market. Adding to households' sense of financial security, real wages have been growing again for roughly the past year, following a two-year decline related to COVID-driven mix changes in the workforce and surging prices. Over the past couple of weeks, as signs of this strength emerged, financial conditions have worsened in the form of rising interest rates and slumping stock values.

—Read the article from S&P Global Market Intelligence

Access more insights on the global economy >

Capital Markets

Window Opens For Real Estate Debt Funds As Fundraising Lags

Real estate debt fund managers touting a once-in-a-decade opportunity to lend to a finance-starved commercial real estate market face parallel fundraising challenges that limit their ability to raise dry powder. Institutional investor appetite for private credit has grown in recent months, but the real estate debt subcategory drew just $7.68 billion from investors in 24 fund closings between Jan. 1 and July 24, according to Preqin. With a broader slowdown in alternative asset fundraising, real estate debt funds are on a trajectory for their worst annual fundraising performance in at least a decade. That could still change; Preqin was tracking 268 real estate debt funds in market targeting an aggregate fundraising total of $90.2 billion.

—Read the article from S&P Global Market Intelligence

Access more insights on capital markets >

Global Trade

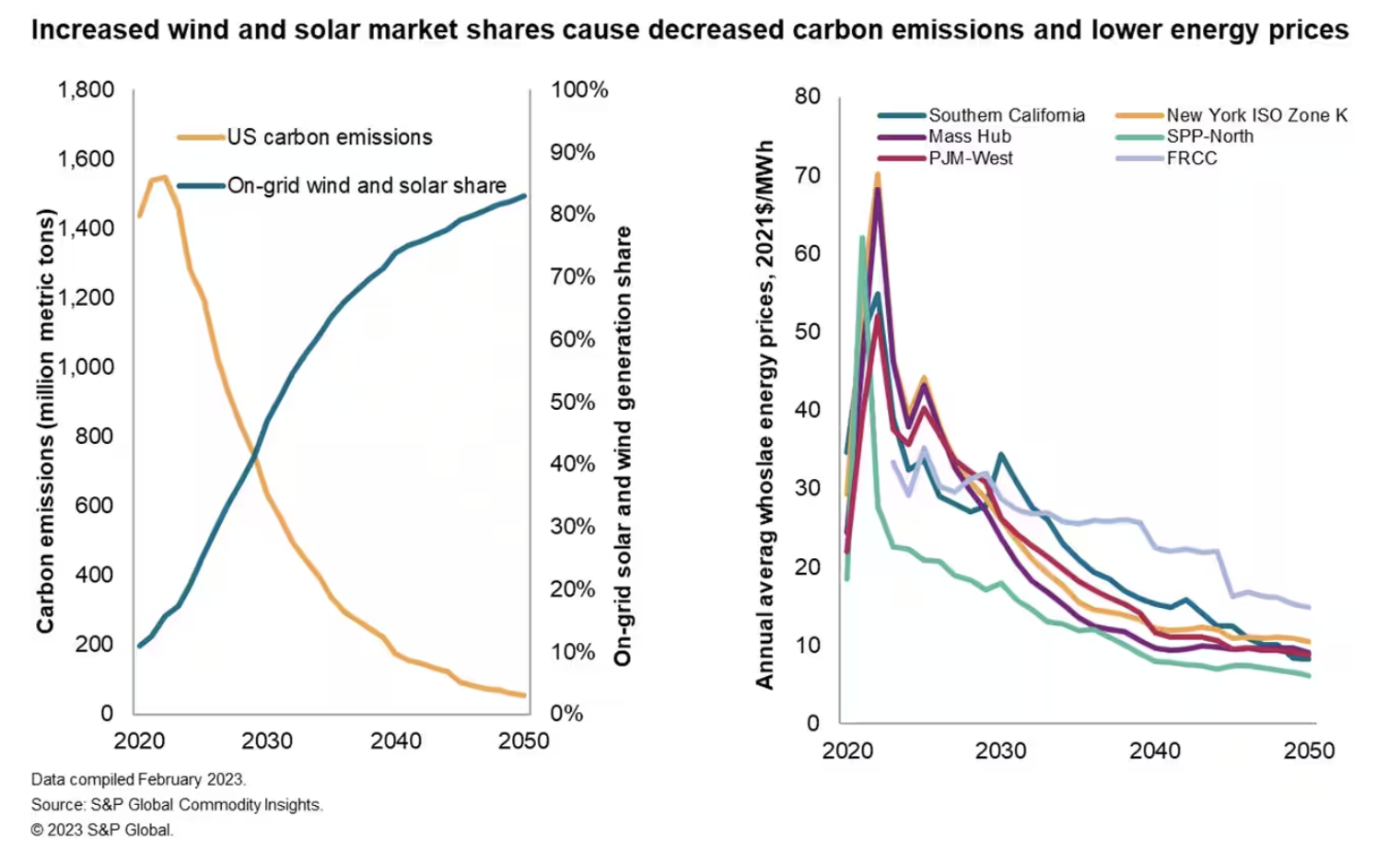

Renewable Energy’s Uncertain Financial Challenge In A Net Zero Future

Building the amount of wind and solar (and other resources) needed to achieve a US net zero power grid and a net zero economy will be a challenge on a number of logistical, supply chain and regulatory fronts. One challenge that often gets scant attention is the basic question of revenue adequacy. S&P Global Commodity Insights' research paper "Net zero's missing money challenge: US power market implications of the 2022 Fast Transition Case" dives in on that specific topic. Read the highlights in this article.

—Read the article from S&P Global Commodity Insights

Access more insights on global trade >

Sustainability

China's Crude Imports From Saudi Arabia, Russia Rebound In Aug, But Uptrend Likely To Falter

China's crude oil imports from Saudi Arabia and Russia are showing signs of a rebound in August after declines in July, but those gains are not likely to last as refineries wait for the next announcement on import quotas. Saudi Arabia's crude shipment to China are averaging 1.9 million b/d in August, up from 1.3 million b/d a month earlier, while Russia inflows are at 1.38 million b/d, up on month from 1.36 million b/d, according to Kpler shipping data. Imports from Saudi Arabia were at a 12-month low of 1.33 million b/d in July, while Russian shipments dropped to 1.91 million b/d in the month, the lowest since April, China General Administration of Customs data showed.

—Read the article from S&P Global Commodity Insights

Access more insights on sustainability >

Energy & Commodities

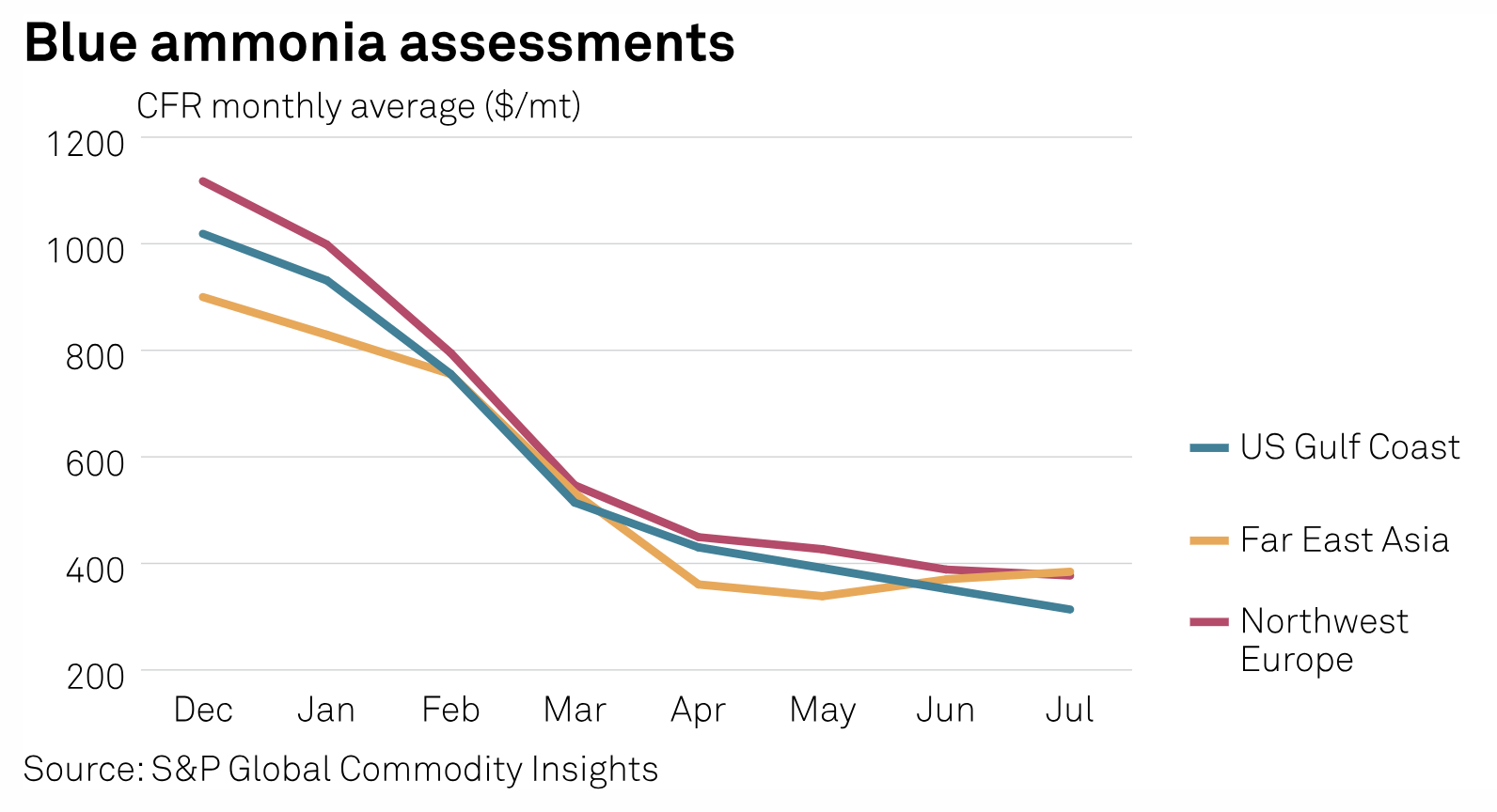

US July Blue Ammonia Prices Extend Discount To Europe, Asia

Ammonia prices in the Middle East rebounded sharply in July on tighter supply, while prices in the Atlantic Basin continued to slide as European feedstock gas prices retreated further, widening the US discount to other regional pricing hubs. However, the market firmed as the month progressed, with tightening supply outweighing slow demand. Platts Ammonia Price Chart illustrates monthly averages of daily assessments for gray, blue and green ammonia across a range of geographies and delivery options.

—Read the article from S&P Global Commodity Insights

Access more insights on energy and commodities >

Technology & Media

ASEAN Sales & Production Commentary — August 2023

Light-vehicle sales in the Association of Southeast Asian Nations (ASEAN) recorded about 266,000 units in July 2023, marking an increase of 5.8% compared with July 2022. For the year-to-date performance, the market increased 1.5% to about 1.85 million units. The ASEAN market will likely decrease 0.2% to 3.34 million units in 2023. Thai light-vehicle sales in July 2023 decreased 7.5% year over year to about 57,200 units. The current high household debt, tighter auto loan approval, poor export performance from global softened demand and rising political uncertainty have delayed consumer purchasing on automotives.

—Read the article from S&P Global Mobility

Content Type

Language