Crude Oil

September 19, 2024

Crude prices boosted by US rate cut but bearish demand outlook persists

HIGHLIGHTS

China's slowing oil demand growth still underpinning price weakness

Current price rebound could be short-lived: S&P Global

Hedge funds hold record net short Brent positions

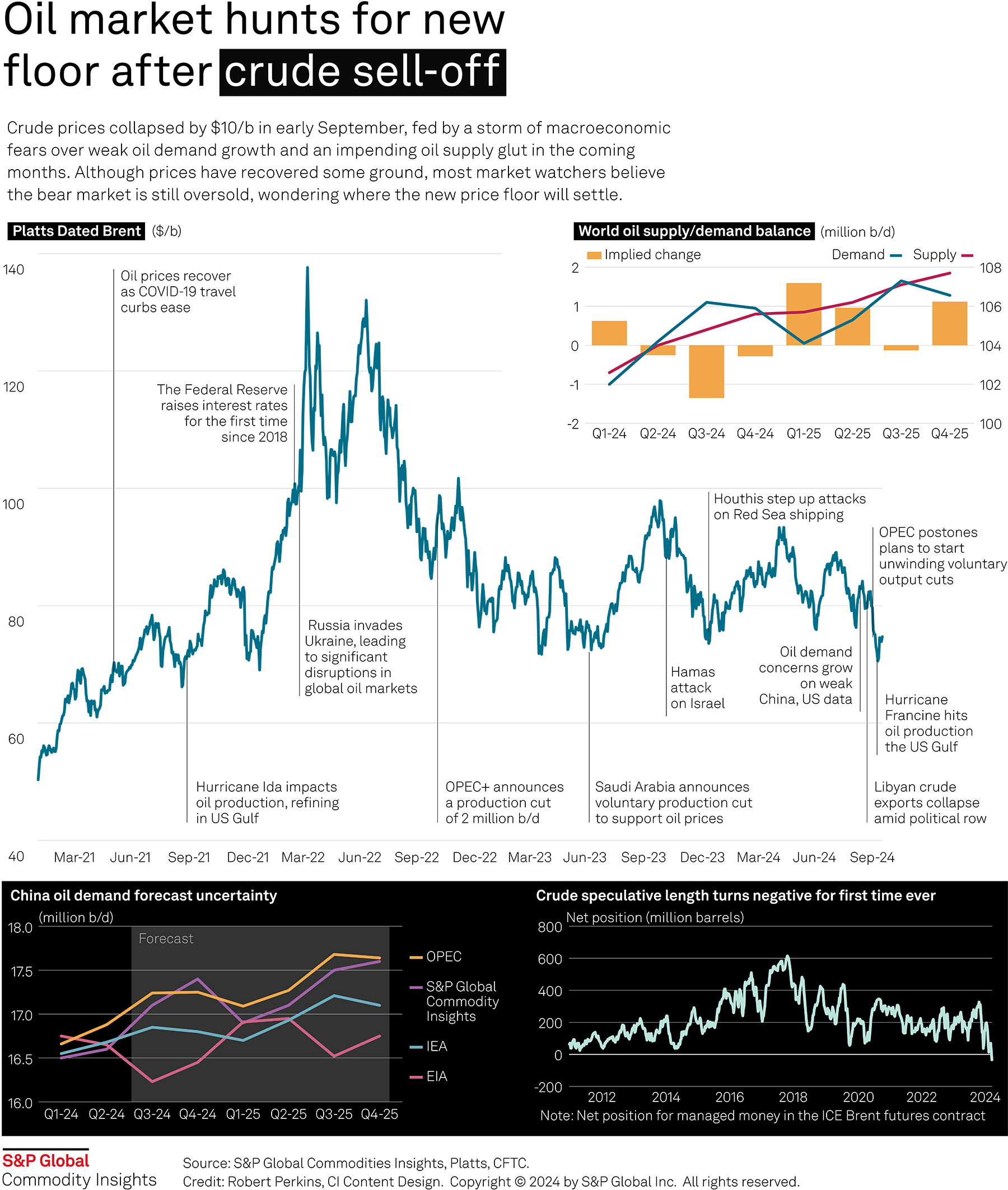

Crude prices received a shot in the arm from the US interest rate cut Sept. 19 but a bearish demand outlook continues to grip global markets and supply-side uncertainties mean traders are struggling to call a new floor on prices after oil tumbled to three-year lows.

Dated Brent --the physical crude benchmark though which most of the world's oil is priced-- slumped to $70.56/n on Sept. 10, its lowest level since December 2021, despite OPEC+ postponing a production increase by two months and continuing stock draws.

US outages from Hurricane Francine and a large US interest rate cut on Sept. 18 have helped reverse some of the losses but markets remain fixated on macroeconomic headwinds. Stocks draws have also been supportive with OECD commercial stocks dropping in the week to Sept. 12, continuing a seven-week draw streak.

But the oil market's demand concerns have focused on China, the world's biggest oil importer, with a growing market consensus that Beijing is no longer the same engine driving global oil demand growth.

Weak industrial activity has dented GDP forecasts, while a struggling property market, an aging population, and booming clean energy spending is clouding China's oil demand outlook. Chinese oil demand estimates from major forecasters differ by more than 1 million b/d in the second half of 2025. The International Energy Agency now expects demand will rise by less than 1 million d/d in both 2024 and 2025. OECD Europe oil demand resilience is also in question and the even seasonal US summer oil demand boom failed to meet expectations.

"Weaker interest rates will ultimately support the economy and, therefore, gasoline and diesel demand, but seasonal demand weakness remains present and will cap any near-term upside," oil analysts at S&P Global Commodity Insights said in a Sept. 19 note.

Oil price calls

Commerzbank on Sept. 18 cut its spot Brent crude forecast to $75/b by the end of 2024 and $80/b in 2025, down by $5/b and $10/b, respectively citing a worsening demand outlook.

Goldman Sachs estimates that the market has downgraded oil demand expectations by nearly 1 million b/d over the next six months. Cutting its Brent oil price forecast in early September, the investment bank currently sees downside risks to its forecast for Brent averaging $77/b in Q4. Leading trading houses were heard discussing prices as low as $60/b at APPEC 2024, a far cry from the $100/b forecasts of less than six months ago.

PVM, an oil brokerage, set a price floor at $67/b in a Sept. 11 note, blaming the "relentless move lower" on evidence of decelerating demand growth after OPEC downgraded its own global oil demand forecasts for 2024.

In the first week of September, oil analysts at S&P Global Commodity Insights expected the physical Dated Brent benchmark to average $80/b by the year's end, before falling into the mid- $70's by late 2025. Platts, part of S&P Global Commodity Insights, assessed Dated Brent at $75.08/b on Sept. 18 after recovering from a three-year low of $70.56/b on Sept. 10. Dated Brent has averaged $74.21/b so far in September and $83.15/b since the start of the year.

On the supply side, a key uncertainty remains whether OPEC+ still intends to gradually withdraw voluntary production cuts of 2.2 million b/d from December. Perceived geopolitical risks to supply had also been falling with a partial resumption of exports of light, sweet crude from Libya. But the recent targeting of Hezbollah militants in Lebanon with exploding devices could reignite fears of a wider Middle East conflict.

"As long as the production increase hangs over the oil market like the sword of Damocles, the oil price is not likely to recover significantly," Commerzbank said in its note.

Japan's MUFG bank sees the key question in the current oil markets as the price level that would prevent, or prompt, OPEC+ from increasing (or further lowering) its oil production. A key OPEC+ monitoring committee is set to convene on Oct. 2 to reassess oil market conditions.

Click here for the full-size infographic

Net short

The rapid sell-off in crude futures markers since August has also witnessed unprecedented net short positions by hedge funds on Brent crude. After the sell-off, bearish bets on Brent by money managers exceeded Brent bullish bets for the first time ever, meaning Brent crude's speculative length turned negative for the first time in history.

Oil analysts at Standard Chartered believe the recent sell-off also fed momentum-following trading algorithms which exacerbated the price fall.

"The negative feedback loop seems to have been reinforced by an unusually high degree of groupthink among hedge funds and other speculative flows led by a market narrative of a current or impending supply glut," Standard Chartered said in a Sept. 19 note. "The overwhelming bearishness among money managers has taken positioning in crude oil and oil products to the most bearish extreme since the start of the Global Financial Crisis."

The future curve for oil has also become more bearish in recent weeks, with backwardation weakening since August, pointing to less interest in prompt barrels. With likely inventories builds in the coming weeks and demand for prompt barrels easing, S&P Global expect the structure to keep easing further.

"Oil risks remain gravitationally to the downside," MUFG said. "Beyond, Chinese malaise and an impending loosening in physical fundamentals, hedge funds' unprecedented net short positions on Brent crude and refined products (especially, diesel and gasoil), reinforce the bearishness."