17 Sep 2020 | 19:02 UTC — New York

US oil and gas rig count up 6 at 293; Permian slightly slides: Enverus

Highlights

Permian rig count down 2 to 128

Midcontinent gas supply under pressure amid drilling decline

BP to increase focus on US upstream

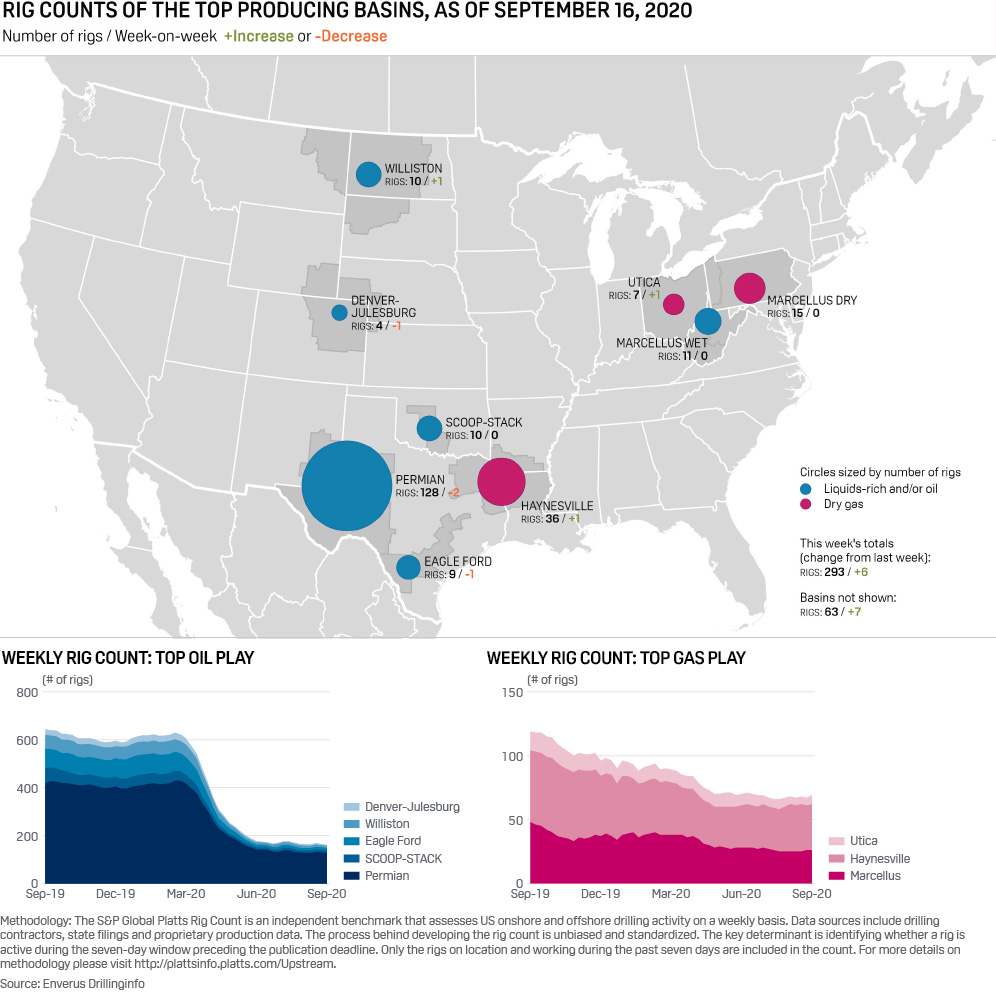

New York — The US oil and gas rig count climbed six in the week ended Sept. 16 to an eight-week high 293, rig data provider Enverus said Sept. 17, but drilling activity across the major named basins edged lower.

The number of oil-focused rigs climbed four to 200, while the number of rigs chasing mostly gas edged up two to 93, the highest since the week ended July 1.

The uptick marked a fourth straight week of rising US drilling activity, potentially signaling rig counts are set to break out of the recent doldrums that have held nationwide totals in the 280-290 range since July. But aggregate activity in the major named basins moved lower on the week.

Rig counts in the west Texas Permian Basin were lower for a second straight week, falling two to 128. The decline left the basin's rigs counts comfortably within their recent range of 127-131 that has persisted since August.

Operators in the Eagle Ford basin idled one rig, leaving a total of nine, and the Denver-Julesburg play shed a single rig, putting the total number active there down to four, an eight-week low.

These declines were partially offset by a one-rig uptick in the Haynesille, Bakken, and Utica plays, putting total rig counts there at 36, 10, and seven, respectively.

Rig counts were static on the week at 26 in the Marcellus play and at 10 in Oklahoma's SCOOP/STACK basin.

Across these eight named basins, the total oil and gas rig count was down by just one on the week at 230.

Click here for full-size image

{kind=link}

Midcontinent gas supply under pressure

Continued production weakness in the SCOOP/STACK basin could push US Midcontinent natural gas prices sharply higher this winter as regional markets struggle to keep pace with demand.

So far in September, SCOOP/STACK gas production has averaged about 3.6 Bcf/d. While output has rebounded more than 12% from summer lows recently, it has also struggled to return to levels above 4 Bcf/d seen in the first quarter of the year, data compiled by S&P Global Platts Analytics showed.

For the fourth quarter, current Platts Analytics forecasts show total Midcontinent gas production hovering around 6.1 Bcf/d, about 1.9 Bcf/d, or nearly 24%, lower than a year ago.

Although winter season heating and power demand in the Midcontinent are expected to decline this year, along with net outflows to neighboring markets, the region is still likely to face greater supply tightness this winter compared with last.

BP to increase focus on US upstream

BP expects to sell off around 600,000 boe/d of oil and gas production capacity over the next five years as part of its ambitious transition from an integrated hydrocarbons producer to become a global energy major, its upstream head, Gordon Birrell, said Sept. 16.

Although selling off higher-cost, carbon-intensive resources, Birrell said BP still plans to grow its production in high-margin regions such as the US shale.

In the US shale portfolio, ongoing "high-grading" will focus on the Permian and east Eagle Ford basins. BPX Energy, its US shale unit, plans to see breakeven oil and gas prices average $35/b WTI and $3/MMBtu Henry Hub in 2021, and is targeting projects with at least 30% post-tax returns at $45/b WTI and $2.50/MMBtu Henry Hub.