08 Feb 2022 | 16:02 UTC

Physical crude markets in the spotlight as Dated Brent nears $100/b

Highlights

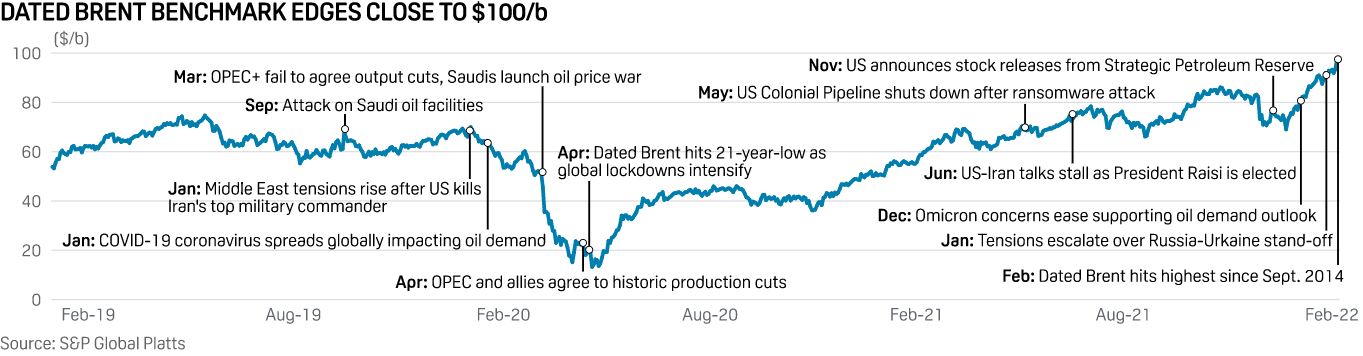

Dated Brent assessed at fresh seven-year high of $98.20/b

Forties crude at all-time highs, refiners willing to pay huge premiums

Tightest market in years sends market into steep backwardation

Demand for physical oil cargoes has reached its highest in over a decade in Europe and the Mediterranean where refiners concerned by shrinking stocks are helping push the price of prompt delivery Brent crude towards $100/b.

Dated Brent -- used to price more than half of the world's crude -- surged to $98.20/b on Feb. 7, the highest since Sept. 9, 2014, S&P Global Platts data showed Feb. 8. The last time this benchmark crossed $100/b was on Sept. 4, 2014 -- six months after the ouster of former president Viktor Yanukovych in Ukraine -- when it was assessed at $101.195/b, Platts data also showed.

The surge in physical cargoes -- which coincides with another period of geopolitical uncertainty surrounding Ukraine's future and Russia -- has created a widening gap with oil futures. The April ICE Brent futures contract, which has been trading around $90-93/b this week, stood $90.35/b at 15:50 GMT, after slipping $2.34/b on hopes that renewed talks between the US and Iran will revive a nuclear deal with the OPEC producer and signs that current tensions around Ukraine could ease. Although crude futures softened, EU carbon allowance futures --a key marker underpinning European energy prices--rose as high as Eur98.49/mt to a new intraday record Feb. 8 on the ICE Endex exchange.

S&P Global Platts Analytics sees oil prices supported by concerns over supply risks such as the tensions seen between the US and Russia over the future of Ukraine. The analytics unit of Platts currently forecasts Dated Brent averaging $88/b in August before easing back below $80/b by the end of the year.

However, many forecasters among the world's largest investment banks are continuing to double down on bets that oil futures will cross the $100/b threshold this year. These views are largely supported by the robust demand recovery, historical low inventories in the world's major industrial economies, thin spare production capacity and continued weak levels of upstream investment.

Reiterating its call for $100/b Brent futures by Q3 on Feb. 8, Morgan Stanley noted that since mid-November oil inventories in the OECD have dropped at a rate of 1.2 million b/d, following even faster stock draws described as "relentless" last year.

Massively tight

Shrinking oil inventories have led to a much tighter physical oil market, and the Brent crude complex is in its steepest backwardation on record, nearing $3/b between the front two-month contracts, according to Platts data.

With both OPEC+ and other suppliers unable to keep pace with global demand growth, booming refined product markets have sent buyers scrambling to secure prompt loadings, traders have told Platts. Dated Brent is finding strong support as refiners are willing to pay significant premiums for light sweet crudes. North Sea barrels are 'local' for many and as a result, become preferable in such a steep backwardation, traders told Platts.

"Long-haul is massively more expensive than short-haul due to the backwardation so local grades should be in the highest demand," said one North Sea crude trader.

Regionally, all the key crude grades in the region such as Oseberg, Forties, Ekofisk, Troll and Johan Sverdrup have all experienced strong demand from refiners, boosted by robust refining margins. The key UK grade Forties was assessed at a record-high of Dated Brent plus $2.40/b, Platts data showed. Ekofisk was assessed at $3.275/b premium to Dated Brent on Feb. 7, the highest since Sept. 15, 2011.

Lighter sweet grades, such as Ekofisk, have been in demand as some customers looked for alternatives to WTI Midland due to the market structure.

March-loadings of Ekofisk were trading for over a week ahead of the program release date, evidence of strong buying interest in locking in supply. Traders have told Platts the majority of the program is already sold.

Trafigura bid for both Brent blend and Forties cargoes for February loading in the Platts Market on Close assessment process on Feb. 7. These bids were at a premium of Dated Brent $2.40/b and Dated Brent $2.35/b respectively, Platts data showed, and bids were left outstanding at the 1630 London close.

Backwardation normally indicates a market in significant deficit. Unlike a contango market structure, backwardation discourages storage, with many refiners buying as prompt cargoes, according to market sources. However, this strategy comes with its own risks as those buyers left short are still left having to bid up in order to entice others to release barrels.