09 Jan 2020 | 22:53 UTC — Denver

US working natural gas in underground storage decreases by 44 Bcf: EIA

Highlights

Henry Hub futures stagnant following report

Another bearish draw likely for week in progress

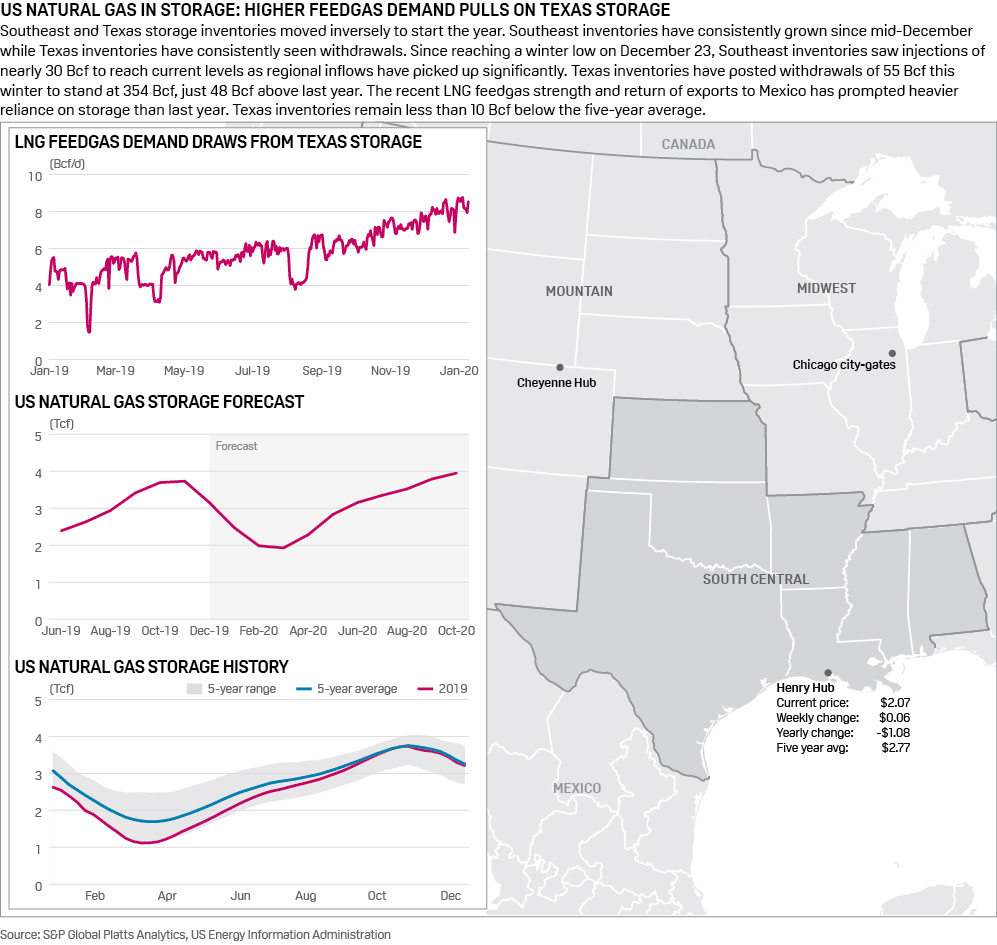

Denver — US working gas stocks fell at rate less than one-third the five-year average last week as NYMEX Henry Hub winter futures remain in the doldrums with more bearish draws likely in the weeks ahead.

Storage inventories fell by 44 Bcf to 3.148 Tcf for the week ended January 3, the US Energy Information Administration reported Thursday morning.

The pull was less than an S&P Global Platts' survey of analysts calling for a 50 Bcf draw. Responses ranged from a draw of 41 Bcf to a draw of 63 Bcf.

The withdrawal was much weaker than the 94 Bcf pull reported during the corresponding week in 2019, as well as the five-year average draw of 184 Bcf, according to EIA data. As a result, stocks were 521 Bcf, or 20%, more than the year-ago level of 2.627 Tcf and 74 Bcf, or 2.4%, more than the five-year average of 3.074 Tcf.

The draw was weaker than the 58 Bcf pulled from working gas in storage reported for the week ended December 27.

Total demand fell by 3.4 Bcf/d to average 100.9 Bcf/d, after a combined 5.5 Bcf/d drop in the Northeast and Southeast was partly offset by a notable 1 Bcf/d increase in the Rockies, an impressive jump of more than 30% for the relatively low-demand region, according to S&P Global Platts Analytics.

Upstream, supplies were down 0.4 Bcf/d to an average 95.7 Bcf/d. Continuing the theme from the past several weeks, almost all of the change in the supply stack came from Canadian imports, which fell by 0.6 Bcf/d, while onshore production remained rigid, falling by only 42 MMcf/d, or less than 0.05%, week over week.

Price weakness is by now seemingly locked-in at the fundamental level, and near-term NYMEX Henry Hub contracts have shown no signs of improving in recent weeks. The balance of winter February-March strip is trading at $2.12/MMBtu during Thursday trading, flat to yesterday's close and flat to a week ago as well.

The transition from an inventory deficit to a surplus this week no doubt does little to assuage concerns of a market in oversupply, though. With the first quarter just getting underway, producers are entering the new decade with a considerably more capital-disciplined approach and potentially a primed grip on the lever. A pullback in production growth, or even a decline in supplies outright, could help rebalance the market, and prices have plenty of room to increase.

Looking ahead to the week ending January 10, total US demand is on the upswing, currently averaging close to 4.2 Bcf/d higher than the week prior, according to Platts Analytics. Also, lower production in the Northeast and Texas is affecting supplies, which are averaging roughly 400 MMcf/d lower week over week.

A forecast by Platts Analytics' supply and demand model calls for a draw of 79 Bcf for the week ending January 10, which would increase the surplus to the five-year average by more than 100 Bcf.

Click here for full-size storage infographic

{kind=link}