27 May 2020 | 17:01 UTC — Insight Blog

Oil is down but not out: signs of recovery as lockdowns ease

Giant pillars holding up oil markets have suffered cracks since the COVID-19 pandemic sent shockwaves through the global economy.

Demand has collapsed and prices have tumbled, but there are reasons to believe the worst of these tremors have passed. Crude has survived the seismic shock waves and can fuel the recovery.

Dated Brent – the physical benchmark used to price two-thirds of the world’s oil – has more than doubled in value since hitting a 21-year low in April.

The measure of high-quality North Sea crudes is now trading at around $34/b, enough to keep the industry functioning. Prices have recovered as major consuming nations begin to ease lockdowns and producers reduce supplies to rebalance wobbly markets.

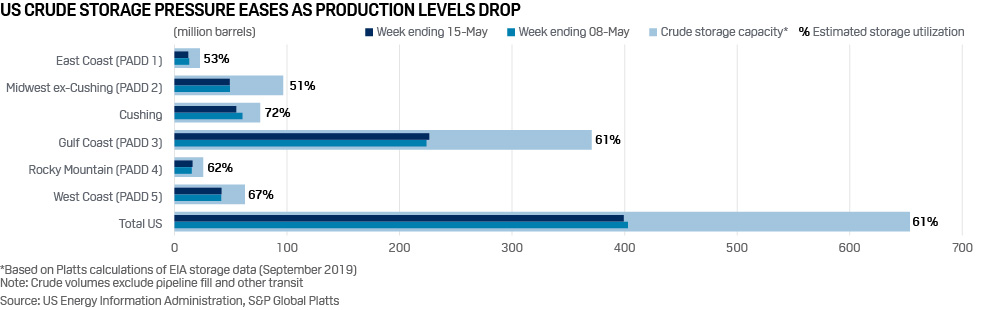

The feared exhaustion of global storage capacity, which briefly contributed to some niche headline US inland oil prices turning negative last month, has abated.

VLCC freight rates have fallen back to around $50,000 per day, from a peak of $200,000 per day this year at the height of the crisis as storage demand as eased.

Click to expand

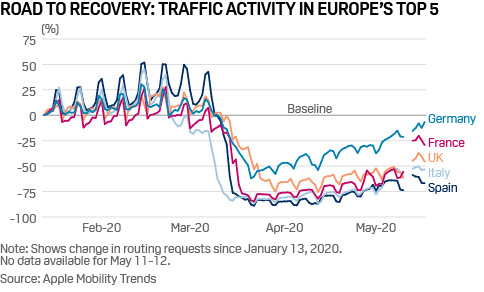

Motorists are helping to restart demand. According to Apple Maps data based on routing requests, road traffic in Britain has doubled since the peak of the travel restrictions enforced in early April.

In the US – the world’s largest oil-consuming nation – the same data shows road journeys beginning to approach pre-pandemic levels as more states open up ahead of the summer driving season. Road congestion in Beijing is back to normal.

The price of US Gulf Coast 87 octane CBOB – the most liquid wholesale gasoline grade traded in the US – had increased by around 133% as of May 14, from its lowest point this year, according to S&P Global Platts assessments. With most of the global aviation industry remaining grounded and consumers still reluctant to use crowded public transport, the internal combustion engine may enjoy a renaissance.

Saudi Arabia and Russia have played their part in averting disaster by agreeing to call off their ruinous price war by agreeing to cut production. Oil supply is now on course to drop by up to 13 million b/d in the second quarter, according to S&P Global Platts Analytics.

Go deeper: Explore commodities and energy insights, online events and more on Platts LIVE

Saudi Arabia – which needs prices to trade above $80/b normally to fund its budget – doubled down this month on its commitment to do whatever it takes to rebalance the oil market by announcing its intention to cut another 1 million barrels from its daily supplies starting in June.

The willingness of Riyadh and the Kremlin to compromise after much cajoling by US President Donald Trump could signal a new era of even closer collaboration with OPEC to manage global oil markets.

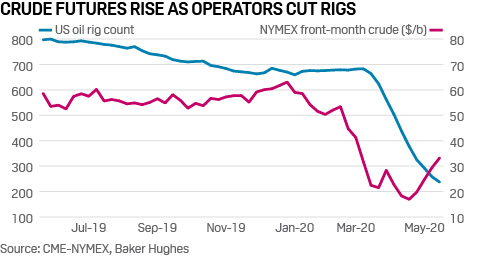

Meanwhile, the US shale revolution has temporarily been put on hold. The number of rigs operating in America has dropped by 65% and more workers on fracking sites have joined the swelling numbers of America’s almost 39 million unemployed. Crude output has fallen by 1.6 million b/d from March to a total of 11.5 million b/d, according to the US Energy Information Administration.

“Today’s price reflects optimism in the market, but further upside will most likely be limited due to higher oil stocks and logistics constraints in US supply, leading to some discounting,” said Chris Midgley, global head of Platts Analytics. “Demand is partially recovering, as people return to cars, but other areas such as aviation will see much longer U-shaped recoveries.”

Of course, oil markets remain fragile. Travel quarantines and consumer reticence could hamper the chances of a recovery for airlines. Global refinery runs are down approximately 13 million b/d year-on-year due to the severe demand contraction seen over the last couple of months, according to Platts Analytics. The outbreak of a new trade war between the US and China could also hit trade and shipping.

In the post-Covid-19 world, governments may also seek to reduce their dependence on fossil fuels in the long term to reduce emissions and protect the environment.

However, oil remains the most cost-efficient way to fuel global growth. Despite the unprecedented economic shocks of recent months, the world has still been consuming more than 70 million b/d of crude. Provided a catastrophic second wave of the pandemic and subsequent lockdowns are avoided, there is no reason to believe that the new normal for oil markets won’t closely resemble the old.

This article was previously published as a column in The Telegraph