13 Feb 2020 | 18:01 UTC — Insight Blog

Amid rising US oil exports, Gulf Coast crude demonstrates global appeal

Unrestricted US crude oil exports recently entered their fifth year.

Each year so far has brought with it new records, milestones and developments as American oil continues to muscle its way into new markets and in greater volumes.

Last year could be remembered as the moment when US crude buyers and sellers more fully embraced a transparent spot market.

Historically, the US crude market has been characterized by unnamed bids and offers, broker-facilitated deals and weighted-average pricing indexes. But beyond US shores – while US crude supply grew but remained landlocked – a more vibrant and sophisticated spot market developed to find efficiency through clarity and specificity.

To attract attention and compete on a global scale, US crude needed to move toward the visible spot market.

Now, perhaps more than any other, US crude of WTI Midland quality has emerged as a truly global crude with three primary pricing hubs – FOB US Gulf Coast, delivered Northwest Europe and delivered Singapore – and several secondary markets developing alongside as well. The year 2019 introduced these new transparent hubs. Could 2020 see their becoming globally relevant benchmarks in their own right?

From zero to hero

The US has seen crude production growth in nine of the past 10 years, and in 2019 the country snagged the crown of the world's top oil producer.

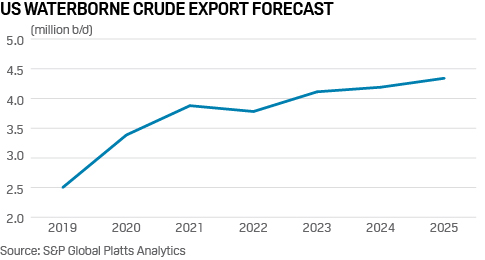

The bulk of this US crude makes its way to the Texas Gulf Coast, where it is loaded onto Aframax, Suezmax and VLCC oil tankers for export primarily to refineries in Northwest Europe, India and North Asia. S&P Global Platts Analytics forecasts US waterborne exports to be 3.4 million b/d in 2020, about one-third more than 2019, and rising to more than 4.3 million b/d in 2025.

Where US barrels flow is a numbers game. Companies around the world study S&P Global Platts price assessments of WTI FOB USGC, WTI delivered into Europe and WTI delivered into Asia, and cross-check those values against prices of competing grades and prevailing freight rates.

The interplay between new spot cargo pricing at the USGC export hub and benchmarks in major refining centers in Europe and Asia dictates to what extent, for example, a Rotterdam refinery could expect a fleet of WTI-laden crude to bring down regional sweet crude prices, while an Asian refinery consequently pulls West Africa grades that have been priced out of Europe.

Or perhaps the lack of a visible arb when comparing these price markers could result in more WTI consumption by US refiners, as a narrower Gulf Coast sweet-sour spread knocks out any advantage to running a typically cheaper barrel of Mars from the US Gulf of Mexico.

Go deeper - Explore crude grades with S&P Global Platts' periodic table of oil

In Europe, declining local production has meant regional refineries rely on imports from around the Atlantic Basin, the Mediterranean and Russia. In recent years, US crudes elbowed their way into the picture and Midland-quality WTI is now the dominant flow into Northwest Europe, often arriving at a rate of one-and-a-half Suezmax tankers per day.

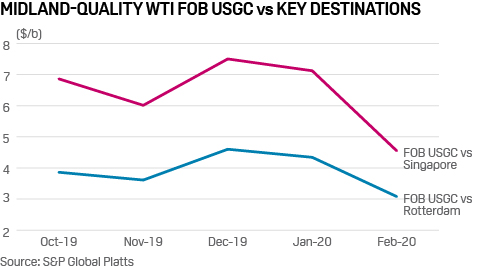

Europe took about one third of US crude exports in 2019, second only to Asia as a region, according to the latest Platts Analytics figures. That is up from about one quarter in 2018-2019 and less than 20% in 2017. The WTI FOB USGC-DAP Rotterdam price spread averaged $4/b in Q4 2019 compared with $3.70/b in 2020 to-date, according to Platts assessments. That slight narrowing has coincided with a cooling freight rate market this year so far.

If Europe lacks in domestic supply, the story in Asia is rather one of increasing demand, driven of course by China, but also US allies looking to diversify their crude supply, namely South Korea and Japan.

Platts data show the WTI FOB USGC-DES Singapore price spread averaged $6.80/b in Q4 2019 and $5.85/b in 2020 so far – a significantly wider spread than FOB USGC to Europe. However, US crude sent to Asia instead of Europe must cover greater ground – a 45-day journey rather than two to three weeks to the latter – and that brings with it additional costs.

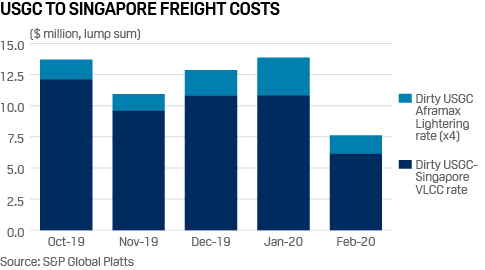

Nearly all US crude exported to Asia will be done on the largest tankers available, VLCCs, to achieve greater economies of scale. Dirty USGC-Singapore VLCC rates have averaged $8.5 million in 2020 to-date, down from a whopping $10.8 million in Q4 but significantly higher than the $5.5 million range in Q1 2019, Platts data show.

Lightering from an Aframax onto a VLCC is a necessary cost when exporting to Asia; 2020 lump sum rates are about $560,000 this year so far compared with Q4 2019’s $415,000, according to Platts figures.

Despite the higher costs compared with Europe, North Asia remains the top destination for US crude led by South Korea, Taiwan and China. South Asia – specifically India – also consumes its fair share of US crude.

Participation, liquidity rise

Rising export volume brought more market participants. That has led to increased transparency and liquidity in these developing benchmarks, starting in summer 2019, days before the US Independence Day holiday.

During the Platts Market on Close assessment process on July 2, the US crude producer Occidental Petroleum offered a 700,000-barrel cargo of Midland WTI to be loaded in Corpus Christi in late August. Occidental gradually lowered its offer to Dated Brent plus 60 cents/b, where the UK oil major BP expressed interest and bought the cargo.

It was the first trade of a delivered WTI Midland cargo in the Platts Market on Close assessment process – and a step forward for transparency. Since then, 10 more trades have been executed via the Platts MOC, the most-recent on December 19.

Beyond those trades, the MOC has seen 37 offers and 21 bids and participation from Lukoil, Vitol, Trafigura, Total and Shell, in addition to the pioneers Occidental and BP. There has also been MOC activity in Asia.

This activity should set the stage for an even more robust 2020, particularly as new IMO 2020 marine fuel rules are expected to increase demand for light sweet crudes.

This increase in transparent trading coupled with rising flows into Northwest Europe, North and South Asia and beyond will undoubtedly be discussed during Platts London Oil & Energy Forum that kicks off IP Week 2020 later this month. Ongoing benchmark development will also be a theme to follow in the months ahead.