31 Jan 2023 | 10:58 UTC — Insight Blog

EV sales momentum to face challenges in 2023, but long-term expectations unaffected

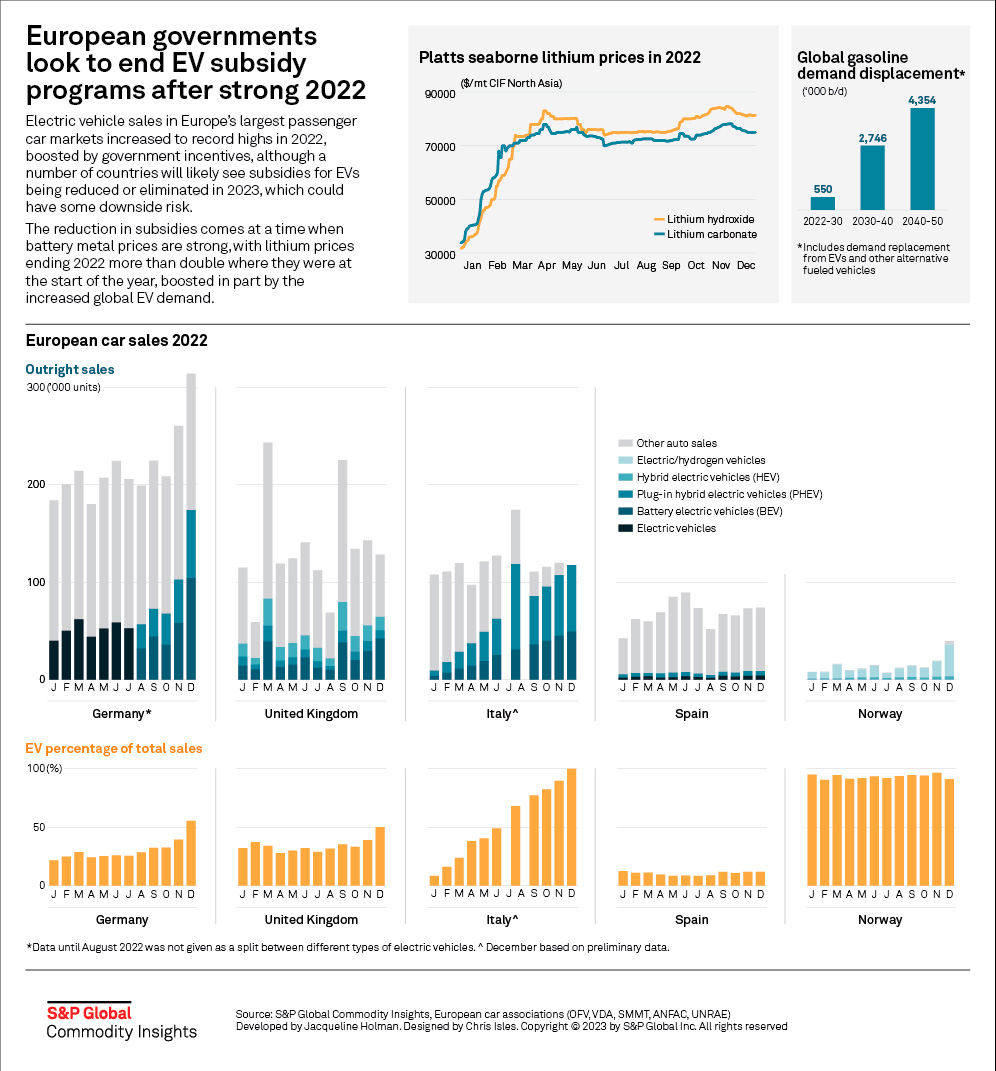

Electric vehicle sales grew about 36% on the year in 2022, according to S&P Global Mobility estimates. The momentum, however, is at risk in 2023 due to several factors: the end of China's subsidies, Europe's energy crisis and the consequent inflation, and recession fears in the US.

China is by far the largest market for EVs. The country's new energy vehicle sales should have reached 6.7 million units in 2022, more than double the figures registered in 2021, according to the China Association of Automobile Manufacturers. NEV sales accounted for 33.8% of the country's total vehicle sales in November 2022, which has remained above 20% for consecutive nine months, S&P Global calculations showed.

Some of those sales in the later portion of the year might have been in anticipation of the expiration of China's subsidies on EVs, according to market participants. As 2022 came to an end, China's subsidy for pure battery EVs had the biggest drop since 2019, declining to nil from Yuan 12,600/unit. This was more than double the reduction of Yuan 5,400/unit in 2022 and Yuan 4,500/unit in 2021.

China has subsidized EV sales since 2009 and has since established the roots for the industry. China dominates every step of the battery supply chain, except battery metals mining that depends on the minerals' natural location. This dominance has allowed Chinese OEMs to push down EV costs faster than the West, which might enable an organic growth in future regardless of subsidies.

Sources said battery makers have been significantly reducing output since early December because demand in the coming months was not looking promising.

"A lot of EV demand has been brought forward, so I think the first half of 2023 will not look good," said a source from a China-based lithium converter.

Although the Chinese EV market should take some time to adapt to the new subsidy-free scenario, the situation is not all doom and gloom, said an Australia-based lithium producer.

"There might be a deceleration in demand due to the end of Chinese subsidies for EVs, but not a decrease – deceleration and decrease are different things," the producer added.

The reduced activity in battery and EV making has hardly hit Chinese lithium prices. Lithium carbonate DDP China fell to Yuan 457,000/mt Jan. 30 from a peak of Yuan 590,000/mt achieved Nov. 11, 2022. This was the lowest value since May 17, 2022, but still 18% higher than the price in Jan. 31, 2022.

China's lithium carbonate prices will not tumble in 2023 even though supply will see an increase, because demand will remain strong at least in the first half of this year, said a China-based analyst. China's NEV sales will reach 9 million units through the year, up 35% from 2022, CAAM estimated.

The resurgence of the pandemic in China is also considered detrimental to EV sales and battery production. Although many market participants said the impact would be restricted to the short term since the health crisis is expected to be temporary, a scenario in which the situation deteriorates over a prolonged period would significantly impact Chinese EV sales in 2023.

Economic challenges in the West

The two other bigger markets for EVs, Europe and the US, are also expected to face significant challenges this year, largely owing to macroeconomic factors and the overall outlook.

According to a report from S&P Global Ratings from Nov. 28, 2022, "economic momentum has slowed with a recession next year [2023] increasingly likely [in the US]. As extremely high prices damage purchasing power and aggressive Federal Reserve policy increases borrowing costs, we continue to expect a shallow recession for the U.S. economy in the first half of 2023. Our U.S. GDP growth forecast is 1.8% for 2022 and -0.1% for 2023, a bit weaker than our September economic update [1.6% and 0.2%, respectively]."

The Inflation Reduction Act was created with the objective to boost EV sales in the US. However, most of the positive effects are not expected to be realized until 2024, according to some market participants. Beginning in 2024, buyers will be able to use the EV tax credit value to lower the price of the vehicle directly, instead of receiving tax credits.

Contrary to its key purpose, the IRA in fact could raise some challenges related to the battery metals' and battery components' sourcing thresholds required to qualify for the $7,500 EV tax credits. In 2023, 50% of the battery components and 40% of the battery metals must be sourced within the US or a country with whom the US has a free-trade agreement for a vehicle to qualify for the full tax credits. These requirements rise progressively to 100% for battery components in 2029 and 80% for battery metals in 2027.

"A number of US automakers have warned that the sourcing thresholds could hurt EV sales due to the difficulties in shifting the supply chain in the short term to become eligible for the tax credits," according to a recent report from S&P Global's Metals and Mining Research.

In Europe, persisting inflation and surging energy costs, spurred by the ongoing war in Ukraine, also pose significant risks. "The European economy's strong momentum will almost come to a halt early next year [2023]. Sticky inflation, stunted hiring, and higher interest rates will be clear negatives. [...] We continue to expect the European economy to contract around 1 percentage point of GDP over the next two quarters [Q4 2022 and Q1 2023]," said S&P Global Ratings Nov. 28, 2022, adding that it expected nil GDP growth in the Eurozone this year.

The economic difficulties should weigh on EV sales in these regions, since "the current higher EV prices compared to internal combustion engine vehicles should not be supportive for demand," according to another lithium converter source.

Similar to China, state subsidies in Germany for plug-in hybrids expired at the end of 2022, and those for purely battery-electric passenger cars were reduced. But Germany's new electric car registrations increased 114% in December 2022 compared to December 2021, reaching a new monthly record of 174,200 units, according to the German Association of the Automotive Industry, or VDA. The record shows future EV purchases were brought forward, the VDA said.

There are also major challenges such as the availability of charging points. Although there have been significant investments in charging infrastructure, most of those are still concentrated in China, totaling over 1.4 million EV charging points as of September 2022, versus less than 400,000 in Europe and about 140,000 mt in the US, according to data from S&P Global Energy.

"The automotive market remains adrift of its pre-pandemic performance but could well buck wider economic trends by delivering significant growth in 2023. To secure that growth – which is increasingly zero emission growth – government must help all drivers go electric and compel others to invest more rapidly in nationwide charging infrastructure," said Mike Hawes, chief executive of the UK's Society of Motor Manufacturers and Traders.

According to the SMMT, the government's EV Infrastructure Strategy forecast that the UK would require between 300,000 and 720,000 charging points by 2030. Meeting just the lower number would still mean more than 100 new chargers to be installed every single day. The current rate is around 23 each day.

Lithium prices may follow downtrend

The bearishness regarding EV sales in 2023 has directly affected the lithium market. Spot prices have been falling, particularly in China, and the short-term expectations are not positive. The latest Platts Battery Metals Outlook Survey found that more 50% of the companies surveyed expect Chinese lithium prices to average below Yuan 500,000/mt in 2023, and north Asian lithium prices to average below $70,000/mt.

Even though the recent downtrend in Chinese spot prices was driven by a genuine drop in demand, a factor that needs to considered is that of traders willing to destock material purchased previously at lower prices to avoid the risk of selling at loss. This possibly deepened the recent price reduction since December but should therefore only be momentary, if so.

Fundamentally, the lithium market remains tight. S&P Global's Metals and Mining Research forecasts lithium chemical supply at 858,000 mt of lithium carbonate equivalent (LCE) in 2023, up from the 668,000 mt forecast for 2022, while LCE demand was forecast at 856,000 mt, up from 684,000 mt in 2022. This would put the market in a marginal surplus of 2,000 mt in 2023, improving from a deficit of 15,000 mt in 2022.

If any of the capacity expansions tabled for this year are delayed, or if quality requirements prove to be too difficult to achieve quickly (which historically has been common among lithium projects), the tiny surplus can easily turn into another year of supply deficit, assuming demand is not delayed by the potential slowdown in EV sales.

As market activity resumes normalcy after the Lunar New Year holidays, the gaps in supply should progressively emerge that could halt the bear run. Pricing trajectory for the rest of the year will depend on how the supply-demand balance evolves and on the general market sentiment, which does not always capture the outlook effectively, often failing to realize the fundamental supply-demand balance. This was evident in the beginning of the bear run in late-2020 as several participants were surprised since they believed the industry was still sitting on three to six months of inventory, which was the case earlier in that year but had been absorbed.

Regardless of the uncertainties for 2023, a price crash seems unlikely in most of the physical market – not only this year but also through the decade, due to the delayed investments in new capacity that are likely to take years to be realized. According to the International Energy Agency, it typically takes 16.5 years on average to move mining projects from discovery to first production. In the particular case of lithium chemicals, there are also additional complexities that do not exist in typical mined commodities, such as protracted qualification processes and necessity to ensure customer battery-grade requirements are fully achieved.

Long-term EV fundamentals remain strong

Despite the several risks for EV sales growth in 2023, the long-term shift away from internal combustion engine vehicles remain unaffected. S&P Global Mobility projects that the share of battery electric vehicles, plug-in hybrid electric vehicles and fuel-cell electric vehicles in new light vehicle sales in Europe, mainland China and the US will rise to 70%, 49%, and 47% in 2030, respectively, from an estimated 19%, 18% and 8% in 2022.

"The past two years have witnessed – included from policy, industry and market perspectives – what in retrospect may be the seeds of an 'EV revolution'," S&P Global Mobility said in a recent report.

The most critical aspect supporting EV adoption is regulation: all of the key regions for automotive sales have witnessed policies being implemented – by both governments and OEMs alike – to drive the adoption and growth of EVs.

In July 2022, China issued a proposal for automakers' new energy vehicle quotas that would increase to 28% in 2024 and 38% in 2025 from 18% in 2023. In the US, even before the IRA, the Environmental Protection Agency finalized greenhouse gas emissions standards for vehicles for the 2023-2026 period with a roughly 8% annual average increase in stringency. Furthermore, the EU is currently finishing new rules on CO2 emissions that would effectively ban sales of ICE vehicles in 2035.

These policy directives have led automakers to announce ambitious plans for additional EV capacity, including the launch of new models.

"Today, nearly all automakers have put zero emissions vehicles at the heart of their long-term strategies – and, perhaps more importantly, their medium-term investment plans," according to S&P Global Mobility. The report emphasized that in some markets such as China, Germany, France and the UK, EVs are no longer a niche option and have already become mainstream.

The shift to electrification of transportation seems to be an irreversible trend, but the transition could slow down due to raw material supply challenges, S&P Global Mobility said. Battery-grade lithium, cobalt and nickel will all likely be in deficit in the coming years, supporting prices as demand outstrips supply. Higher battery costs, which increased in 2022 for the first time in over a decade, could delay electric vehicles' run to reach cost parity with ICE vehicles. This would intensify the difficulties generated by near-term global economic weakness, as well as limit the utilization of installed capacity for battery makers and automakers.

With Jacqueline Holman and Analyst Lucy Tang

In the latest Platts Future Energy podcast, we uncover the potential roadblocks facing the EV market in 2023. From lithium prices to government subsidies, learn how these factors may impact EV sales and the battery metals market: