31 Dec 2018 | 11:30 UTC — Insight Blog

Newcastle coal rally eases but supply could stay tight in 2019

Prices of a key Australian thermal coal grade went on a rollercoaster ride in 2018 following unexpected friction during yearly contract talks with a major export market, Japan.

This hiccup in trade was shortlived and gave way to sustained high prices that could continue to shore up the sector. Following a period of cost-cutting and readjustment to new market realities over the last few years, the Australian coal sector now looks in better shape, while new coal-fired power plant builds across Asia should provide reliable demand for the fuel.

Price-setting contracts delayed

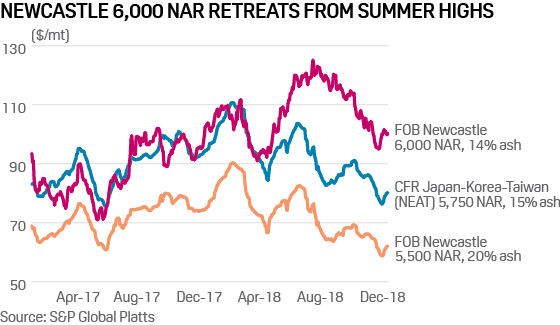

The persistent elevation in prices for the type of Australian thermal coal consumed by power plants in Japan was a key talking point in the Asia-Pacific thermal coal market during the year. Spot prices for Newcastle 6,000 kcal/kg NAR suddenly started to accelerate in April when talks to settle Japanese 2018-19 financial year term contract prices began to get bogged down, and failed to produce any settlement by the end-April deadline.

The rally carried on through May and June, and went on to peak at $125/mt FOB Newcastle in mid-July. All the while the talks in Japan failed to produce any result in terms of a price benchmark for term contracts that started delivery in April and which run through to the end of March 2019. This was unprecedented, as Japan relies on its annual April benchmark for Australian thermal coal to price most of its imports.

Eventually, there was some kind of breakthrough in Japan around August, when two lesser-known power companies stepped forward to accept an Australian coal producer’s offer price of $110/mt FOB Newcastle for JFY deliveries of 6,000 kcal/kg NAR thermal coal. Since mid-July’s spike, spot prices for the Newcastle 6,000 kcal/kg NAR grade have gently descended, and apart from a short-lived dip to $95/mt in November have remained at over $100/mt.

This eight-month period that Newcastle 6,000 kcal/kg NAR prices have spent above $100/mt FOB is the grade’s best performance since the heady days of 2011-2012 when China’s import demand was booming.

A new lease of life

To give an idea of the scale of this year’s Newcastle price rally, one only has to remember Australian thermal coal’s dark days in 2016 when spot prices collapsed to $50/mt FOB, and producers struggled to cover their production and transport costs and to pay government royalty taxes. Only by boosting production to spread their unit costs over a larger volume and embarking on severe cost-cutting programs did many Australian producers manage to survive these extremely tough times.

Looked at in isolation, and in comparison with spot market prices for other grades of Australian thermal coal, 2018’s phenomenon of elevated Newcastle 6,000 kcal/kg NAR prices looks impressive. Newcastle’s price performance this year has certainly succeeded in multiplying the earnings and profits of producers in Australia to an extent that coal companies are back as stock market darlings, and asset sales and takeovers are back in fashion.

Prices for Newcastle 5,500 kcal/kg NAR thermal coal, a sister grade to Newcastle 6,000 kcal/kg NAR that is mostly used in China’s coastal power plants, had less of a wild ride in 2018. Trading in a range of $58 to $90/mt FOB Newcastle, prices for 5,500 kcal/kg NAR spot cargoes have been in an overall downtrend all year, after China steadily tightened import controls for seaborne thermal coal arriving at its ports.

China has effectively set a limit on the amount of imports it takes from the seaborne market at 270 million mt, about two-thirds of which is thermal, in an effort to fend off competition from its relatively high-cost domestic coal industry.

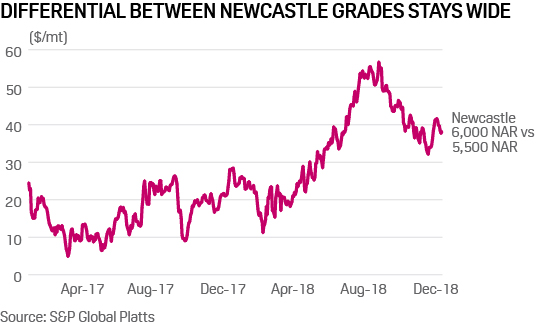

The difference between the price performance of these two grades of Newcastle thermal coal is stark – the price gap ballooned to $56.70 in August and has deflated to around $38 now – and is all the more remarkable given the recent price history of Newcastle thermal coal.

Supply-demand balance shifts

Market participants have advanced several reasons for this year’s price rally in Newcastle 6,000 kcal/kg NAR prices including:

- Low capital investment in Australia’s thermal coal industry over the past several years of low prices has constrained the growth of supply chain capacity for exports. For example, the Terminal 4 project at Newcastle port has been shelved.

- Mach Energy’s 10 million mt/year Mount Pleasant mine in New South Wales is one the few new start-ups in Australia, and begins producing thermal coal later in December. Other proposed new mines such as Posco’s Hume mine have faced rejection by planning authorities, or extensive procedural delays like Adani’s Carmichael project.

- An ongoing pipeline of new coal-fired power plant projects in Asian countries such as India, Malaysia, Pakistan, Philippines, Thailand and Vietnam which is continually adding demand for Newcastle, Australian thermal coal. China and Japan are also building new plants that use Australian thermal coal.

- Australian producers are booking more and longer-term demand from Asian customers in the form of long-life term contracts, leaving less production for spot market sales for newer market entrants.

- Shippers of Australian thermal coal have been adept at finding new markets in Chile, Egypt, Northwest Europe and Turkey, while demand in China took a dive this year, and have grown demand for their product.

In summary, after 2018’s surprise to the upside for Newcastle 6,000 kcal/kg NAR spot prices, market trends indicate that supply is only set to tighten in 2019, as more demand hits the seaborne market.