Aug 15, 2022

HPAI in the U.S.

By Adam Speck

- The progression of high pathogen avian influenza (HPAI) through US flyways and mandated commercial poultry flock depopulation has not had a discernable impact on broiler harvest or market prices to date.

- Turkey complexes continue to be the most susceptible to flock infection with the HPAI virus.

- HPAI outbreaks continue to affect the table egg production sector, particularly the egg product sector where an estimated three-quarters of that sector has been impacted to date.

HPAI Overview

HPAI, also known Highly Pathogenic Avian Influenza or H5N1, is a contagious virus that has a high mortality rate among poultry. It infects the gastrointestinal and respritory systems of the bird, causing vital organs to cease to function. HPAI spreads via infected animals that transmit the virus through their saliva, mucus, and feces, as well as through farm equipment and vehicles. Due to the densely populated nature of poultry holding facilities, HPAI tends to spread rapidly and can wipe out a large percentage of the flock in a very short period of time. This can lead to a sudden drop in supply and a sharp rise in the price of related products. As a result of the the potential economic, social and psychological damage that can be caused by the presence and threat of HPAI, the USDA has established guidelines to actively track and mitigate the impact on the industry. The recommended form of action is culling, which is a rapid depopulation of infected birds in order to minimize the spread of HPAI to healthier members of the flock. The immediate impact of HPAI in North America has been reflected across all related poultry and egg markets since its initial identification in Dec 2021.

Individual Sector Impact

Although the impact of HPAI has been prevalent in the poultry and eggs sector as a whole, the individual sector impact has varied as the spread of the virus continues.

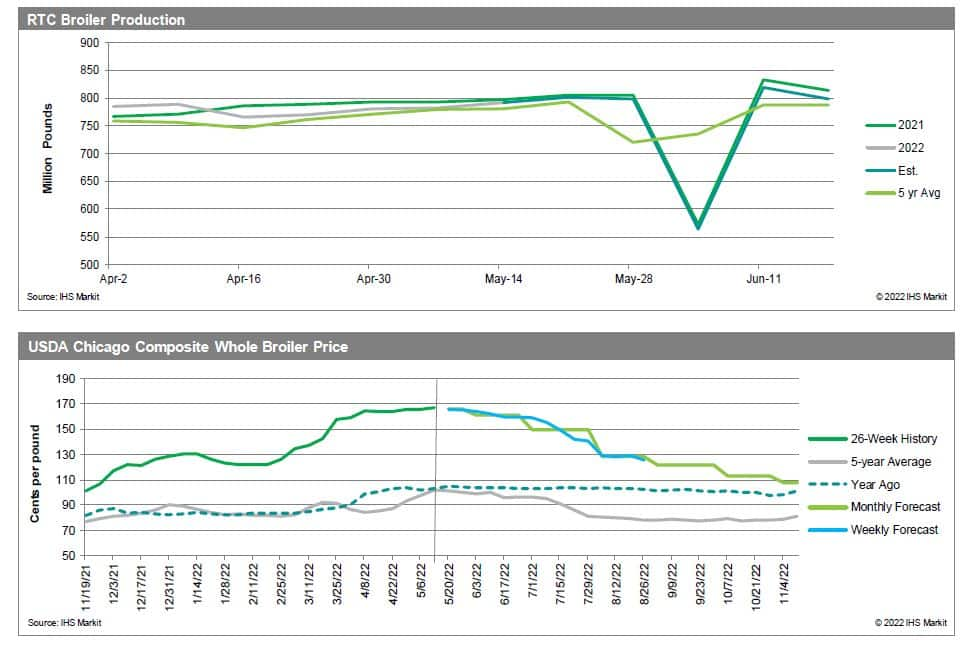

- Broilers: Broiler markets have been the least impacted by HPAI in the poultry and eggs sector.Production continues to trend in line with 2021 and the five year average. Depopulated birds due to HPAI only represent a fraction of the annual broiler harvest, and any bans of key trade partners have been offset due to solid domestic demand. Prices remain elevated from the previous year due to tight harvest supply and a depressed perception of parts/raw material. In addition, retail usage in the form of grilling has come into play in the last month, further bolstering the already strong prices with the seasonal trend.

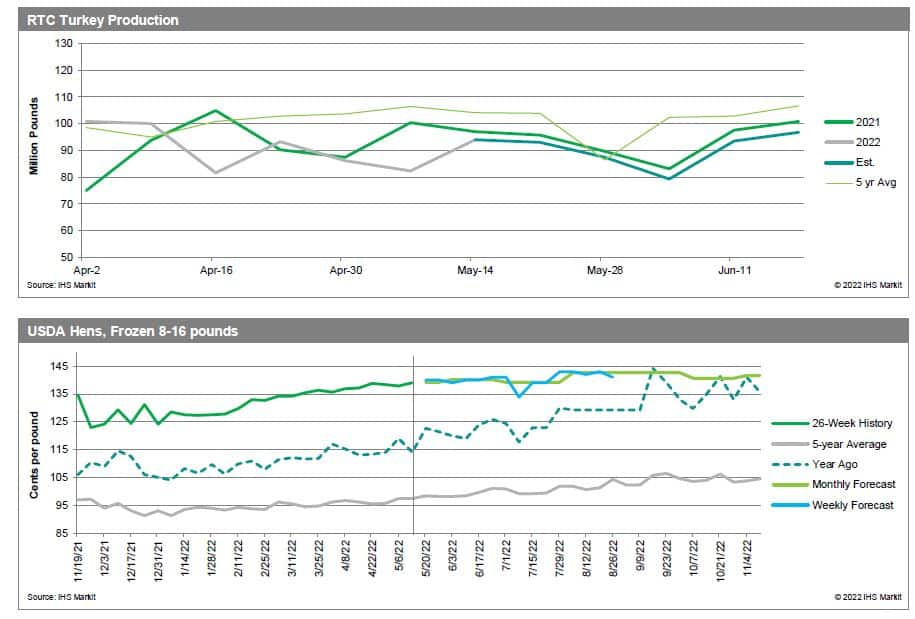

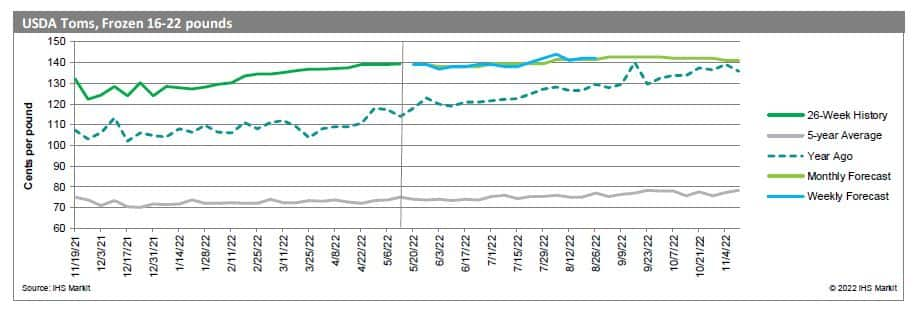

- Turkey: Conversely to broiler prices, turkey markets have been significantly impacted by HPAI. YTD production was 5.4% below the 2021 period, and the most recent six weeks were 1.4% below the same period. Prices have been trending higher as limited supply, export constraining trade bans, and unplanned depopulated continue to weigh on the market. In addition, depopulation further tightens availability, continuing to push up high prices. Even when farms are restocked, it is likely that product banned from export would be reallocated to cold storage in order to minimize the impact of potential harvest shortfalls. However, there has been little discernable domestic price pressure from import bans on export clearance.

- Eggs: Similar to turkey, eggs have also been profoundly impacted by the onset of HPAI, particularly the shell egg product sector. Retailers are concerned over product availability and have limited featuring of shell eggs as a result. Egg product demand remains strong, as manufacturers aggressively source ingredients to offset the impact of HPAI. Consumer level shell egg demand remains steady despite elevated prices.

2014-2015 HPAI

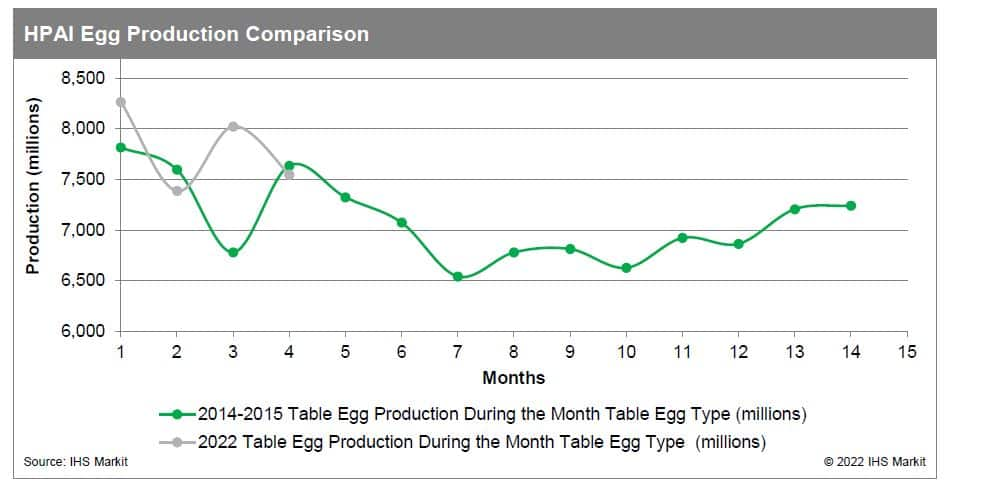

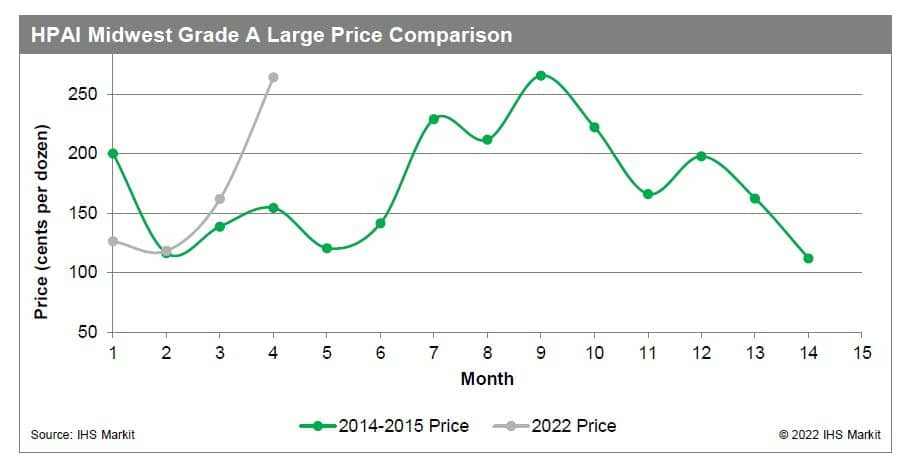

The previous HPAI outbreak in the United States occurred during 2014-2015, when similar behavior in trends across all poultry and egg markets occurred. Depopulation was still implemented at the time as the primary form of mitigation against the outbreak of the disease. Egg production declined sharply from May to December 2015, with the layer inventory falling to 2011 levels. As a result, prices increased sharply, with the benchmark egg price reaching a 61% premium from the previous year at its peak. Both processing and consumer grade eggs saw similar price action during the initial outbreak, but the spread between the two narrowed from May to August 2015 due to larger price increases in processing eggs, fueled by strong demand from commercial operations. Monthly egg exports declined by nearly 50% at the onset of the outbreak and resulted in a $41 million loss in export income. Turkey production endured a similar drop but began recovery in mid 2015 and returned to pre-HPAI levels by early 2016. Price fluctuations were relatively muted, with a slight increase occurring after the outbreak period, but returned back to pre-HPAI levels by December 2016. Monthly exports declined by nearly 40% and resulted in a $177 million loss in export income. Broiler production was not impacted by the spread of the virus and continued its sideways trend for the duration of the outbreak. Similarly, prices also trended sideways with a slight bias towards the downside throughout and past the outbreak period. Monthly exports also continued the regular trend and had no discernable impact on income. Egg production remains considerably elevated in 2022 when compared to the 2014-2015 level. Similarly, Midwest Grade A Large prices are trending higher this year when compared to the previous HPAI outbreak.

This article was published by S&P Global Energy and not by S&P Global Ratings, which is a separately managed division of S&P Global.