25 Feb 2020 | 19:01 UTC — Insight Blog

Charting a course for ammonia as shipping fuel, with tentative steps: Fuel for Thought

The announcement by Norway’s Equinor in January that it had signed a deal to modify a vessel to run on ammonia highlighted the opportunity for another fuel in the ever-diversifying future of bunker markets.

Equinor said the move was part of a bid to cut carbon emissions to zero. This was a bold move, but part of a wider zeitgeist in the hydrocarbons industry amid growing pressure from the public and lobbyists for companies to provide greener energy.

Ammonia and upstream hydrogen are two potential ways to meet these demands, not least in the marine fuel sector.

“We see huge potential both for hydrogen as well as ammonia for use as bunker fuel,” Grzegorz Pawelec, Research, Innovation and Funding Manager at Hydrogen Europe, the European hydrogen and fuel cell association, said.

The association identifies three main opportunities for the hydrogen-ammonia chain in the marine sector: compressed hydrogen in very short distance voyages; liquid hydrogen in short sea shipping, such as cruise ships; ammonia or other synthetic fuels such as methanol for deep-sea shipping.

Equinor’s plan is to modify the Viking Energy, a supply vessel. Those involved in the project envisage a five-year research, installation and testing program. These are baby steps for what is still a niche fuel in the marine fuel sector. Factors such as cost and infrastructure loom large in the prospects for the fuel’s uptake.

“It is clear that markets have started to organize around longer-term energy solutions that are designed to stand the test of time, as energy transition moves from theory into practice,” Dave Ernsberger, Global Head of Commodities pricing for S&P Global Platts, said. Platts started assessing hydrogen in December.

“We have seen genuine and sustainable trade flow emerging for hydrogen in several locations, organized around natural gas or electrolysis supply chains, and the building blocks were clearly in place for us to start providing insight into the value of hydrogen in those markets,” Ernsberger said.

Go deeper: Podcast - Costing sustainable hydrogen: prices, pathways and policies

Broader GHG curbs?

Equinor’s announcement came within the first month of 2020, a resonant year for the bunker industry.

The shipping and refining sectors have been preparing for and are still adapting to a 0.5% sulfur cap on emissions from marine fuel used on the high seas, down from a previous cap of 3.5%, mandated by the UN’s International Maritime Organization.

Many in the industry have highlighted the problems this has thrown up and the transition is proving challenging for some, but the IMO has made clear this is not the end and that it plans to cut greenhouse gas emissions from shipping by 50% by 2050, compared with 2008 levels.

The industry is having to think creatively about the future and this poses questions that ripple through the supply chain.

LNG is one option that meets the strictures of IMO 2020 but, as methane, it could fall short of future caps on greenhouse gases. The costs of LNG for bunkering are low, but those for installing liquefaction terminals and equipping barges are high and the so-far undeveloped scope of these facilities limits uptake of the fuel.

S&P Global Platts assessed LNG for bunkers at Rotterdam at $186.432/mt February 20, compared with $465/mt for 0.5% sulfur fuel oil, the prevalent IMO-compliant bunker fuel.

It is difficult to compare hydrogen and oil product prices because the technologies that operate on H2 are very different from oil consumption, one analyst said.

Some logistical challenges

The

infrastructure problemis one that ammonia and upstream hydrogen share.

In 2016 there were over 2,800 miles of dedicated H2 pipeline installed globally, with 1,600 miles in the US. This stands in contrast to over 130,000 miles of onshore oil pipelines and 300,000 miles of onshore natural gas pipelines in the US alone, according to figures from S&P Global Platts Analytics’ Scenario Planning Service.

So there would be some building still to do for hydrogen and ammonia to significantly expand their presence at international ports.

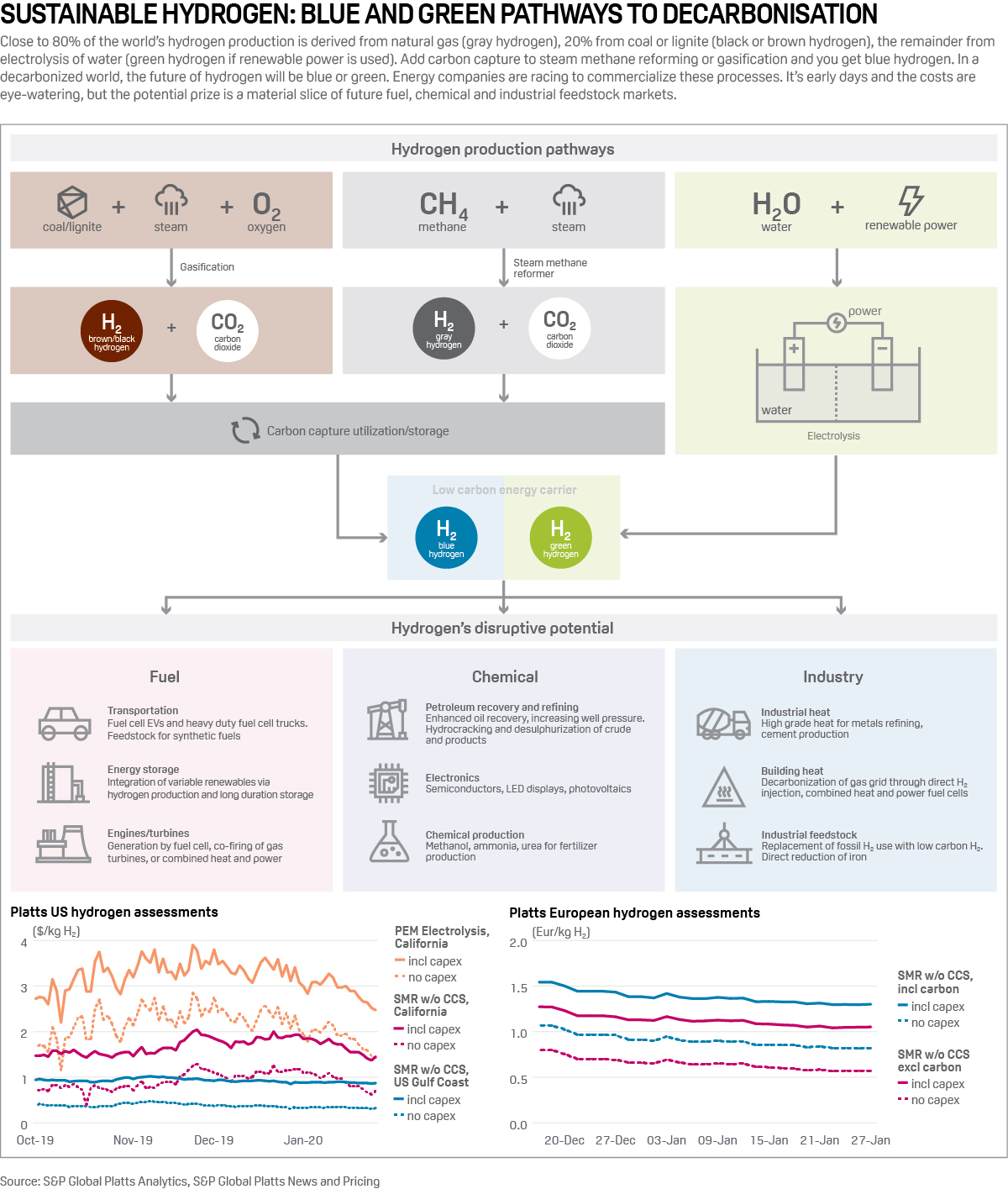

There are different ways to produce hydrogen and downstream ammonia, reflecting what is still a varied market with differing levels of green credentials. This is all part of the infrastructure question.

Click for full-size infographic

Roughly 95%-99% of hydrogen is produced at refineries and ammonia plants, so-called grey hydrogen. When combined with carbon capture and storage technology this is known as blue hydrogen. Alternatively, hydrogen can be manufactured by electrolysis from renewable energy, known as green hydrogen.

“While low carbon typically has a cost premium to fossil hydrogen, negative power prices and curtailed renewables do offer pathways to cost competitive zero-carbon H2,” Zane Macdonald at Platts’ Analytics Scenario Planning service said.

Platts Analytics estimates that a global 5% blending of zero carbon H2 into the gas grid cold abate up to 175 million mt of CO2 per year – equal to the total annual GHG emissions of a country like The Netherlands.