22 May 2019 | 16:10 UTC — Insight Blog

Mexico's liberalized natural gas market in an era of nationalism

By J Robinson

In December, Mexico's energy market reform turned five years old. The event was unceremoniously marked by the inauguration of Andres Manuel Lopez Obrador, or AMLO—a nationalist, left-leaning presidential candidate elected partly on a promise to dismantle it.

While the recent growth of Mexico's reformed gas market has surpassed the expectations of many, it now faces new challenges ahead.

In an early move that rattled investors, president-elect Lopez Obrador in October announced the cancellation of Mexico City's new international airport. The decision followed an unofficial, popular referendum on the project that AMLO called an exemplary exercise of democracy.

Referendums, which have been subsequently used to determine the fate of even major energy infrastructure projects, are now the hallmark of a president bent on redefining Mexico's sovereignty.

The emerging challenges to Mexico's natural gas market, though, extend beyond those posed by AMLO.

In the midstream, aging infrastructure at the country's gas processing plants threatens the viability of domestic production. For imported supply too, tough environmental laws and land-use regulations in Mexico challenge the viability of critical gas transmission projects.

In downstream markets, supply scarcity, particularly in southern Mexico, continues to starve out many industrial users and power generators. Even across parts of central Mexico, where end-users are better served by a dense network of pipelines, access issues have dramatically increased fuel costs for end users.

Despite the challenges, Mexico's gas market has evolved rapidly following liberalization. In the upstream, private players have gained access to both onshore and offshore production blocs once exclusively reserved for development by state-owned Petróleos Mexicanos or Pemex. In the midstream, an enforced contract transfer program has seen more diversity emerging in shipping markets with CFEnergía and smaller distributors entering a space previously controlled by the state.

Centralizing control

Perhaps the biggest political challenge to Mexico's gas market under the Lopez Obrador administration will come from a slowdown in the implementation of its energy market reform, and potentially, an outright reversal to certain policies enacted under it.

In mid-March, for example, Mexico's Secretariat of Energy, or Sener as it is commonly known, announced a sweeping organizational change to the Comisión Federal de Electricidad or CFE – the state-owned power generator that controls over 85% the country's installed capacity.

The move reintegrated its six generating subsidiaries into one, potentially lowering operational costs, but simultaneously creating a single near-monopsony fuel purchaser for Mexico's gas-fired power plants. The change consolidates Mexico's competitive market for natural gas, but also creates a dominant state-owned market participant that is less likely to innovate.

Tightening his grasp on CFE, the president has also vowed to change the generator's existing pipeline capacity contracts, either through renegotiation or through legal action in the courts. While reform efforts saw CFE anchor many of Mexico's new gas pipelines, some of those projects have gone underutilized, leaving the utility responsible for capacity payments with little or no associated income from end users. AMLO claims that those contracts harm both the CFE and the national interest.

The push to centralize control has even extended into the market itself with the cancelation of auctions for new utility-scale power generation projects and delays to upstream oil and gas auction rounds.

On the power side, the president justified the move by claiming that utility-scale projects contracted to the lowest-priced generators would not sufficiently address Mexico's need for decentralized and distributed generation – particularly for communities not connected to the county's power grid.

The delay to oil and gas auctions, though, amounted to a more naked grab at power. At the time, the president said that exploration and development companies holding leases would first need to demonstrate their ability to increase production before more blocs would be awarded.

Administrative changes

At agencies like Cenagas, Mexico's national gas-control operator, and the CRE, its energy regulatory commission, recent and high-level administrative changes could also have the effect of slowing the growth of competition in Mexico's gas and power markets.

In late March, Mexico's senate rejected all 12 candidates nominated by AMLO to fill vacancies at the CRE, claiming that they lacked political independence and technical expertise and demonstrated anti-competitive views on how Mexico's energy markets should operate.

In early April, the president re-nominated 11 of those same candidates to fill the same CRE vacancies, in a move denounced by the opposition as a mockery of the selection process. The decision effectively forced the Senate's hand, since a second legislative rejection of the nominees would give the executive authority to select any of the previously rejected candidates to serve at the agency.

Calls from AMLO's CRE appointees to prioritize energy infrastructure for sovereign use have caused alarm among investors. The possibility that Pemex and CFE could have right-of-first-refusal access to gas processing centers, refineries or pipelines, instead of those assets operating based on a market logic, raises serious questions about the capacity of Mexico's energy markets to become truly competitive in the months and years ahead.

Pipeline construction

Beyond political and regulatory difficulties, Mexico's gas market faces separate challenges to the development and maintenance of its midstream gas transport and processing infrastructure.

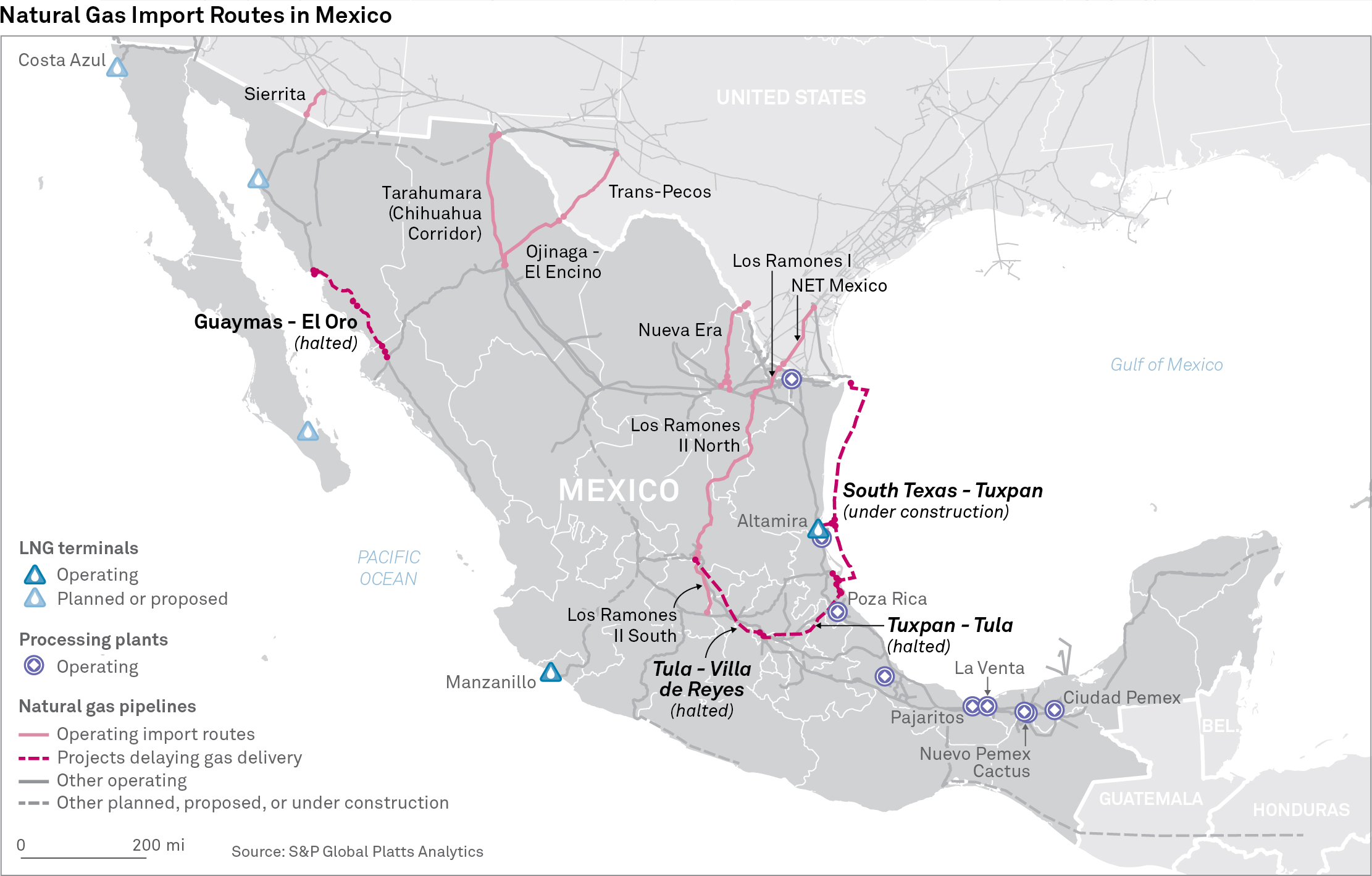

According to Sener, construction work on at least five natural gas pipelines has been suspended due to environmental regulations, land-use constraints, or some combination of the two.

Click to enlarge

In November, two key projects targeting additional supply to central Mexico were halted by TransCanada, one of the largest post-reform investors in Mexico's midstream industry. At the time, the developer said that social and legal uncertainties related to construction precluded further investment in the projects.

The Tuxpan-Tula and Tula-Villa de Reyes pipelines would have delivered nearly 1 Bcf/d of imported US gas to central Mexico. The projects were initially designed to pull supply from the 2.6 Bcf/d Sur de Texas-Tuxpan pipeline, currently nearing completion off the Gulf Coast of Texas and Mexico. Upon startup, the new marine pipeline system will become the second major import route to Mexico, along with the Los Ramones system, also located in South Texas.

Another stalled project is northwest Mexico's Guaymas-El Oro Pipeline. The critical supply route saw its gas transmissions abruptly halted shortly after it began flowing gas in April 2017, when a local indigenous group, the Yaqui tribe of Lomas de Bacum, damaged the pipe over an unresolved legal dispute about land use.

Processing infrastructure

Further upstream, Mexico's gas processing infrastructure is confronting its own mounting risks.

In late February, state-owned oil and gas company Pemex declare a force majeure at its Poza Rica gas processing plant, ultimately resulting in a 27% cut in supply to affected industrial consumers.

An issue at the facility's cryogenic unit raises questions about the potential for further outages, disruptions or forces majeure at Mexico's aging gas processing centers.

In 2018, electrical outages affected operations throughout the year at the 880 MMcf/d Nuevo Pemex facility in southern Mexico. In January 2018, the 182 MMcf/d La Venta processing plant was shut for an entire month due to an extended maintenance.

For 2019, a decision by Pemex to assign its entire $2.9 billion downstream budget toward the rehabilitation of its refineries effectively leaves no resources to cover planned, or potentially even unscheduled maintenance at its gas processing facilities.

Adding still more risk to Mexico's processing infrastructure is the fact that just three of its facilities—Cactus, Ciudad Pemex and Nuevo Pemex process nearly 1.8 Bcf/d, or about 73% of Mexico's domestic gas supply, according to S&P Global Platts Analytics.

Underserviced demand

One of the biggest challenges in Mexico's downstream gas market is access to supply, particularly for end-users across the country's southern and peninsular states.

In southern Mexico, a gas shortage that began last year hit a feverish pace during the autumn months when Pemex began halting gas supply nominations to industrial users in the country's South.

The move came as southern Mexico's dry gas production continued to decline, dipping to record lows at under 2 Bcf/d, according to Platts Analytics. Meanwhile, Pemex maintained its practice of reinjecting natural gas to its existing wells – a process known as enhanced oil recovery or EOR.

Go deeper: Mexico’s gas dependence on US pushes politicians to consider fracking

Currently, Mexico's domestic industry produces approximately 2.7 Bcf/d, according to Platts Analytics. Demand from Pemex alone, though, is about 1.8 Bcf/d of that total, leaving just 900 MMcf/d of marketable domestic production for the country's other end users.

Former Pemex CEO, Carlos Trevino, has estimated that in the southern region alone, nearly 1 Bcf/d of underserviced demand exists from power generators and industry.

Even for Pemex, Mexico's largest domestic gas producer, refinery consumption has been hard hit recently. In 2018, the producer's consumption fell 7% or about 130 MMcf/d compared to the year prior.

LNG imports

With no existing gas storage infrastructure in Mexico, LNG imports have increasingly become a supply of last resort to end-users in southern and even parts of central Mexico. The Altamira and Manzanillo terminals, on the Gulf Coast and Pacific Coast, respectively, have been a key source of backup supply. Mexico's third Costa Azul terminal on Baja California, meanwhile, has largely gone underutilized due to its isolated location off the country mainland pipeline grid.

The biggest issue with LNG sendout, though, relates to transparency around its use and cost.

Currently, LNG supply in Mexico is used primarily for system-balancing purposes. At the end of each month, system operator Cenagas notifies shippers retroactively if their injection and withdrawal activity has created an imbalance.

Although shippers have an opportunity to repay the deficit in kind with gas, imbalance penalties and other usage fees have seen some shippers paying as much as $19/MMBtu for gas supply, or more than six times the current price of gas at the US benchmark Henry Hub.

Increasing the availability of LNG supply is one solution that has offered the potential to help alleviate Mexico's supply shortage, particularly in the south. In 2018, Pemex proposed the installation of a fourth LNG import terminal in the southern state of Vera Cruz.

The floating storage and regasification unit or FSRU was designed to supply 500 MMcf/d to the onshore grid through an interconnection at the Port of Pajaritos in Vera Cruz state.

In a surprise decision announced earlier this year, though, Pemex cancelled the project. While the reasons behind the cancellation were unclear, the move likely came at the behest of Mexico's new presidential administration, which had previously stated its budgetary priority to ambitiously grow oil and gas production at Pemex.

Midstream challenges

A partial resolution to Mexico's gas supply shortage could come from the 2.6 Bcf/d Sur de Texas-Tuxpan marine pipeline, which is currently expected to enter service in April, according to Mexico's Secretary of Energy.

While only a small volume of the imported molecules are expected to reach southern Mexico, the pipe will move additional supply into central Mexico, effectively leaving more of the southern region's own production within its boundaries.

The midstream infrastructure issues in Mexico could potentially pose a longer-term challenge to the country's burgeoning gas market, especially those related to pipeline development and construction.

While the legal battle over some pipeline projects remains lodged in the courts, the outlook is even more bleak for projects that developers have simply halted based on a strategic commercial decision.

For projects like the Tuxpan-Tula and Tula-Villa de Reyes pipelines, a restart could depend on a decision by impacted communities to invite developers back to the negotiating table with well-defined, contract-based demands for remuneration.

On the political and regulatory side, potential challenges posed by the Lopez Obrador administration could be more fluid than they currently appear. By 2021, a changing political landscape in Mexico could see opposition parties regain control from Lopez Obrador's ruling coalition in congress – a move that would diminish the administration's capacity to slow reform and weaken the growth of competition in Mexico's energy markets.