22 Dec 2017 | 17:30 UTC — Insight Blog

LME ferrous scrap contract spread to underlying market persists: analysis

By Pascal Dick and Vaseem Karbhari

With the London Metal Exchange's ferrous scrap futures contract clearing a record 500,000 metric tonnes last month, we take a closer look at market fundamentals driving up both physical and forward prices for obsolete scrap in recent weeks.

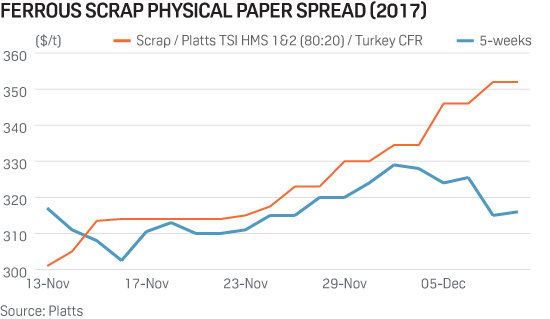

Spot prices for HMS #1&2 80:20 CFR Turkey were range-bound for the first half of November, with Platts TSI's assessment between $300-310/mt.

At the same time, the front-month futures contract on the LME (December 2017) was trading at a premium, with the contango as high as $20/mt.

While a strong contango or backwardation structure is not unusual, the $20/mt spread between the spot assessment (reflecting a 3-8 week delivery window) and the front-month futures contract was "far greater than the cost of carry," as one trader put it.

In which case, why were traders bullish in their price expectations for the remainder of 2017?

The answer partly lies in the recent strength of finished steel prices in both Europe and Asia. European domestic rebar prices reached a six-year high of €555/mt in November, capping off a bull run which began in July and saw prices rise over €100/mt over the summer period.

Additionally, Turkey's very own rebar market has seen prices hit $550/mt – a level not reached since the end of 2014.

The effect has been two-fold. European recyclers exporting to Turkey would have been emboldened by higher finished steel prices, knowing the tailwind effect on obsolete scrap prices would soon materialise.

Similarly, with Europe being Turkey's largest export market this year at 5 million mt (as of December 15, 2017), strengthening rebar prices will have been seen as a welcome opportunity for Turkey's steelmakers to close sales at higher levels.

In Asia, at a time when winter production cuts take effect across the Middle Kingdom, raw materials prices for iron ore and coking coal have held firm to the surprise of many, primarily driven by strong steel mill margins.

A commodities hedge fund active on the LME scrap contract said that China's increasing focus on serving domestic markets and the subsequent decline in exports this year had provided Turkish exporters an opportunity to increase market share, thereby providing support to higher scrap prices.

Indeed, in a recent statement to S&P Global Platts, the Turkish Steel Exporters Association said Asia was the largest growth region this year in percentage terms, though the total volume exported to-date is minuscule at 1.2 million mt.

Other factors also contributed to the rise, such as an expected rise in scrap prices in the US Midwest that meant scrap exporters were in no rush to book deals, with cargo availability limited.

CHALLENGES

With cargo sales to Turkey all on an outright (spot) basis, opportunities to "lock in" the differential are more complex. "In theory the strong contango is there to benefit from, but you are taking risk on the timing and execution of the physical sale and the hedge unwind," a metals derivatives trader said.

This is unlike other commodity markets such as iron ore, which commonly apply indexation as an accepted form of pricing physical cargoes.

While the LME scrap contract has cleared almost 3 million mt this year, the contract has some way to go before larger players are able to fully hedge their physical positions. The vast majority of trade remains on a spread basis between the two listed ferrous contracts or between monthly periods.

This is exacerbated by access issues for some of Turkey's steelmakers. Local companies are only able to access the LME contracts via Turkish subsidiaries of Europe-based financial institutions that are registered members of the LME.

Similarly, European investment banks without a base in the Turkish Republic are "restricted in dealing directly with Turkish steelmakers," according to a source at one such company.

However, several developments point to a convergence of the two curves in the future. The contract's rising popularity on the bourse implies that bigger hedges could already be possible in the near term, as the exchange saw its largest trade of 2,000 lots (20,000 mt) done on November 23 for January 2018 futures at $314/mt.

On the physical side, trading firm Ferrometrics has demonstrated an appetite to bridge some of these divides, working with a UK-based recycler with several dockside locations to hedge physical exposure.

Similarly, Stemcor confirmed to Platts that it was using the Platts TSI assessment in collection contracts within the UK.

The extent to which an increase in the number of market players active in both physical and "paper" scrap contributes to even greater volumes will ultimately determine the success of LME scrap futures as a price risk management tool.

If scrap price movements are still seen as the economic indicator of choice as once popularized by Alan Greenspan, former chairman of the US Federal Reserve, then the development of associated futures markets will be a welcome development for many in the industry and beyond.