28 Oct 2021 | 02:05 UTC — Insight Blog

Energy transition strategic to China’s long-term economic goals

"Crossing the river by feeling the stones" is an expression that describes the approach to reforms and opening up under Deng Xiaoping, the architect of modern China who ended decades of isolation and laid the groundwork for the country's current economic ascent.

The expression refers to the concept of taking small and measured steps and making gradual progress, as opposed to implementing big policies that shock the system into change. It reflected a more nuanced and realistic policy making approach that contrasted with the ideological, social, and political turmoil of the decades preceding China's economic reforms.

Feeling the stones served China well through the 1990s and early 2000s, and the approach in many ways underpins China's current decarbonization policies. It also describes how the country's future climate policy is likely to be devised and implemented, following President Xi Jinping's pledge to peak carbon emissions by 2030 and achieve net-zero emissions by 2060.

More importantly, China's calibrated policy approach highlights an important aspect of its decarbonization road map — energy transition is unlikely to happen at the cost of economic growth and energy security.

Fortunately, Beijing's goals are in alignment. China under Xi sees a huge economic opportunity, and the creation of new industries of the future, in the pursuit of energy transition. It has already leveraged its manufacturing prowess to bring down global renewable energy costs and is pushing to build an economy around electric vehicles and clean energy.

On the energy security front, Xi laid out the country's energy strategy in 2014 at the conference of the Leading Group for Financial and Economic Affairs under the CPC Central Committee.

The so called "Four Reforms and One Cooperation" strategy comprised four reforms — one demand-side reform to curb unnecessary energy consumption, a supply-side reform to diversify energy sources, one reform to improve energy technologies and one to introduce market-based mechanisms to boost growth of the energy sector. The cooperation referred to the greening of its Belt and Road Initiative.

These will continue to guide future climate policy.

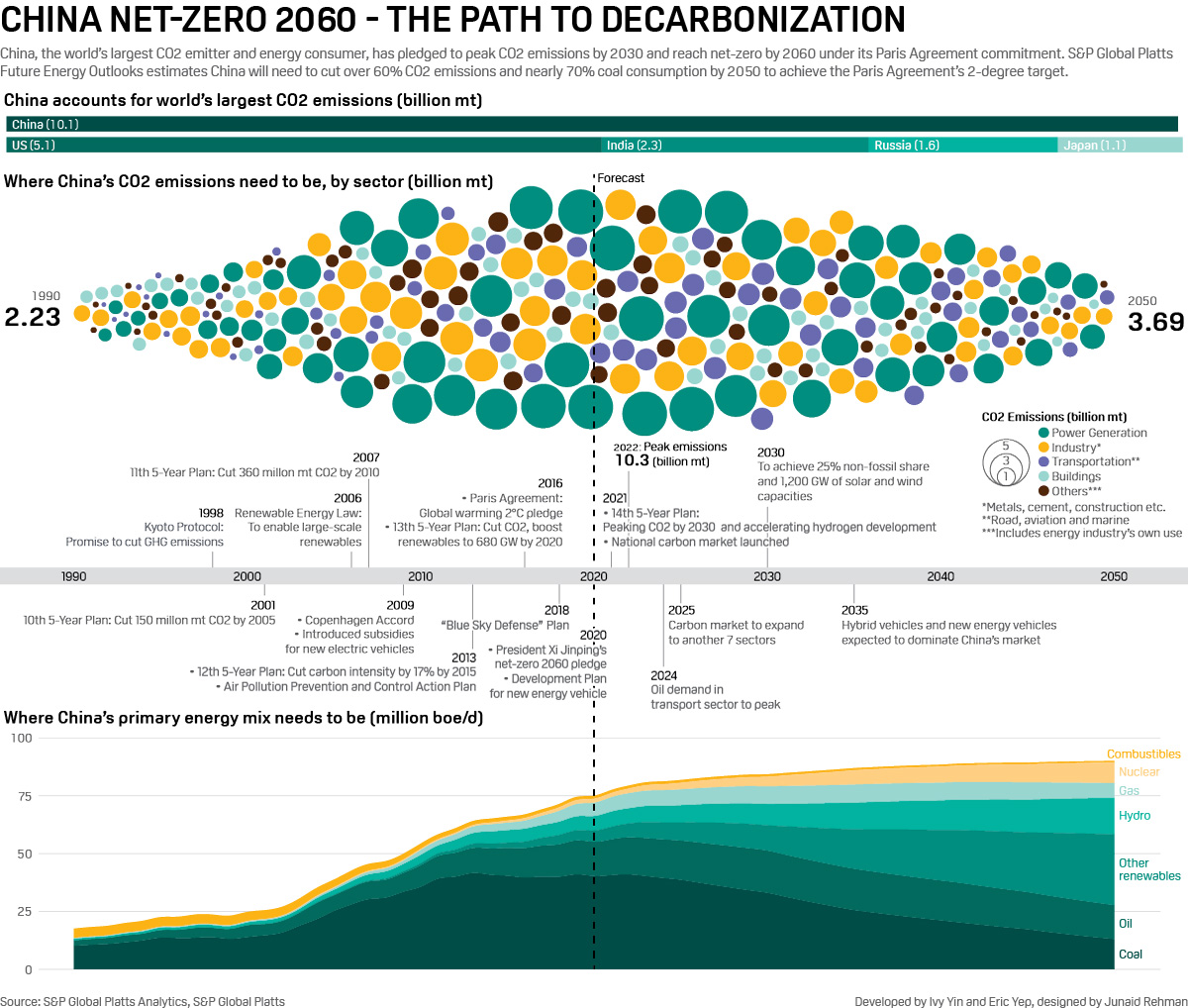

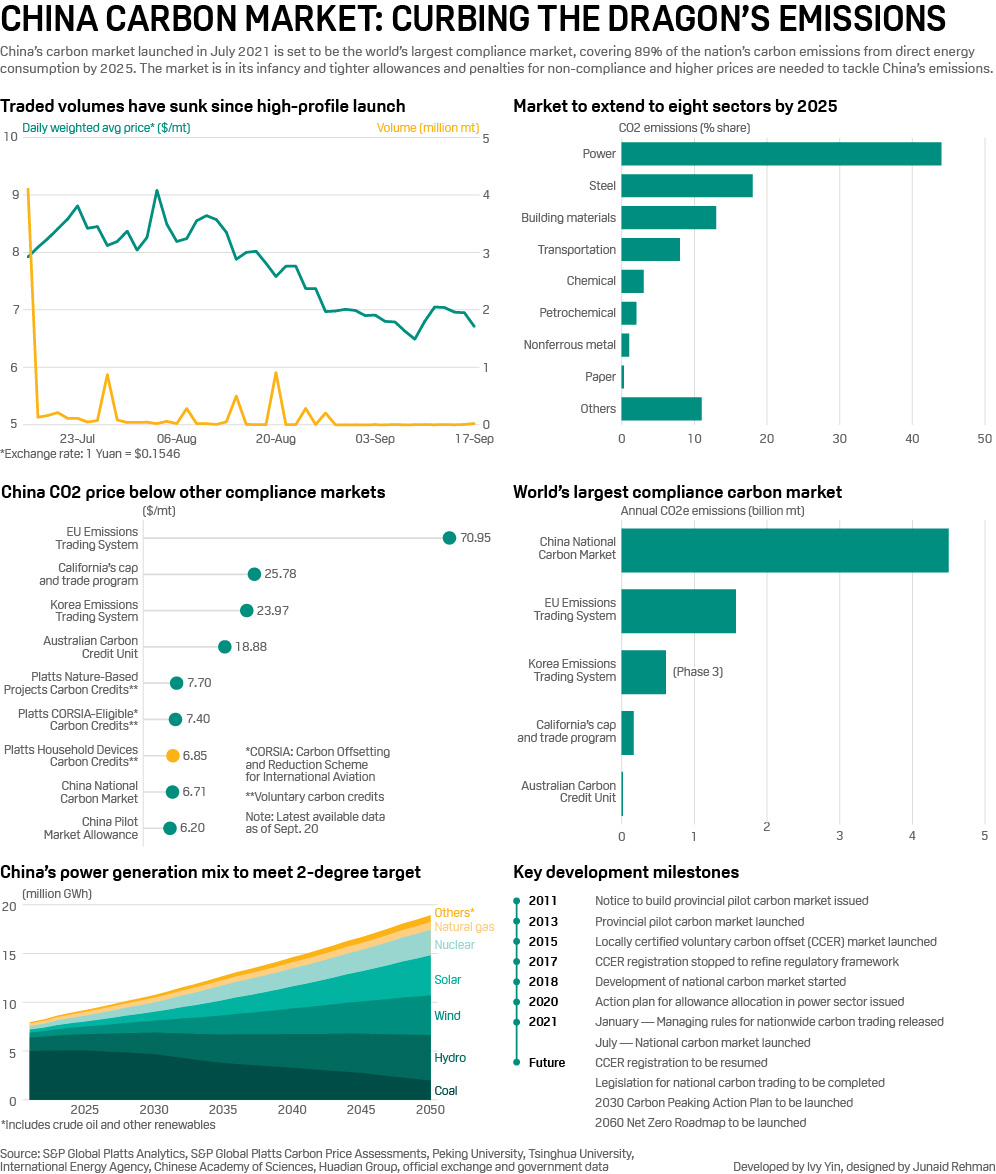

Broadly, China's energy choices will be instrumental in the global climate fight because of its sheer size as the world's largest energy consumer and producer. The launch of its national carbon market in July 2021 put a price on 7.4% of global GHG emissions covering 4.00 GtCO2e in one go, surpassing the EU's carbon market that was the biggest until then.

China already accounts for the world's largest annual wind and solar capacity additions, and an emissions peak in 2030 or 2035 could also mean a peak for global emissions.

Coal is too strategic to fully eliminate

The power sector is estimated to account for 40% of China's energy consumption-based carbon emissions, and over 60% of the country's power generation comes from coal, making it the prime target for decarbonization.

However, China's energy demand is still growing, and instead of paring back existing coal-fired generation, it is much more likely to switch new capacity to renewables.

S&P Global Platts Analytics' base case scenario for China is that the country is in line to reach most of its Paris Agreement targets for 2030 via a combination of renewables and efficiency gains, such as electric vehicles replacing combustion engines, and an economy that becomes overall less carbon intensive.

It expects hydro, nuclear, and other renewables to account for about 26% of China's primary energy demand by 2030, with the country meeting its goal of 1,200 GW of installed wind and solar capacity by the end of this decade.

"This will also help them in achieving peak carbon emissions within that time period," Matthew Boyle, manager, Global Coal and Asia Power Analytics at S&P Global Platts, said.

"The announcement of a 2060 net zero target in China suggests that the country will seek to reduce the role of coal in its energy mix, although we believe this may be more aspirational rather than achievable," Boyle added.

He said Chinese electricity generation is overwhelmingly concentrated in coal-fired plants, and Platts Analytics' base case assumption is that China will continue to develop clean energy capacity but also continue to increase its coal-fired generating capacity.

Hence, decarbonization in China's power sector is likely to be achieved through renewables capacity additions, which means utilization of coal-fired power plants will continue to rise along with increasing nuclear, wind and solar generation capacity.

"Our current view implies around 5-6 GW of new nuclear plant builds annually out to 2050, whereas coal and gas plant additions will stop after 2040. In terms of plant load factors, loads are expected to increase toward the end of our forecast period to 2050 as capacity comes offline," Boyle said.

He said Chinese coal-fired power generation is the largest globally, and likely to remain so in 2060, even though the use of fossil fuels in the electricity mix will have declined by 2060 when compared to 2020 levels.

Other key things to note are that China's coal plant fleet is quite young, with plants likely to continue operating through to 2050. With China moving toward self-sufficiency in coal, and the current focus on economic growth and energy security over decarbonization, dependency on coal will continue through to 2060.

"Putting this another way, the more focused the government is on GDP growth, the more it necessitates a build out in power generation, and therefore the more likely they are to rely on their fleet of young, supercritical and ultra-supercritical coal-fired power plants," Boyle said. "The economics of renewables and the required investment to replace coal in the power stack are just not there at the moment," he added.

The long-term outlook by state-run China National Petroleum Corp.'s research arm Economics and Technology Research Institute has indicated that the share of coal in China's primary energy mix will drop from 57.7% currently to around 50% by 2025, 42.5% by 2035 and 33% by 2050.

Boyle said one of the key things to look out for will be how technologies like Carbon Capture Utilization and Storage are developed, along with producing gray hydrogen from unused or uneconomical coal mines, which will help monetize China's vast coal reserves and young coal-fired power plants.

"This could create a form of additional revenue for the industry that might provide the financial incentive to help it meet its targets," he added.

Implementation challenge looms

China's policy challenge is interesting because in regions like Europe, coal-to-gas switching has been triggered by market-based mechanisms.

China will largely rely on a top-down system, the limits of which were seen in haphazard anti-pollution coal-to-gas policies in the northern regions a few years ago, which led to more hardship for the community and prompted Premier Li Keqiang to call for a more measured approach.

China lacks a dedicated energy ministry, and regulation of its energy sector has traditionally been split between its most powerful economic planning agency the National Development and Reform Commission, the National Energy Administration, and state-run enterprises that often wield as much power as the government in directing energy policies.

Further down the chain are a mix of provincial and city-level governments and numerous government-backed energy companies that handle the local operations of power utilities, transmission networks and oil refiners.

The tussle between state-run refiner China Petroleum & Chemical Corp. or Sinopec and provincial independent refiners once called teapots is an example of how localized industries that create jobs and generate tax revenue can clash with national energy mandates. Beijing recently tightened controls on independent refiners this year by supervising their crude quota usage and tax reporting.

This is truer for industries like coal. China's most carbon-intensive industries are also the most coal-intensive, and heavy industries are concentrated in the northern provinces, while eight out of the 10 provinces with the highest GDP are southern provinces that collectively contributed almost half of China's GDP, official data showed.

An imbalanced decarbonization policy risks affecting northern provinces' economic development and exacerbating existing income inequalities. For instance, northern provinces like Shanxi, Inner Mongolia and Shaanxi have much heavier dependency on coal mining and power sector for taxation, Peng Wensheng, Chief Economist at China International Capital Corp, said at an industry event in July.

In the power sector, generation and distribution is concentrated among a few players.

China's five largest independent power producers, or IPPs, accounted for around 44% of the country's total installed generating capacity of 2.2 TW at the end of 2020. Together called the Big 5 they are Huaneng Group, Huadian Group, China Energy Investment Corp (CEIC), State Power Investment Corporation (SPIC) and Datang Group.

In addition, there are four smaller generation companies — SDIC Huajing Power Holdings (SDIC Power), China Shenhua Group Guohua Power Branch (Guohua Power), China Resources Power Holdings and China General Nuclear Power Group — and numerous provincial power producers that together make China the world's largest electricity producer.

The Big 5 were formed after power sector reforms designed to decentralize power generation and separate electricity production from transmission and distribution. So far, the Big 5 have been ahead of the curve in aiming for peak emissions by 2025 even before national pledges were announced, including announcing renewables targets and a higher share of clean fuels in their energy mix by 2025.

But the power generation companies lack a dedicated road map for coal plant decommissioning, face high costs of renewable capacity additions, and a nascent carbon trading market.

Like the rest of the world, the conversation and debate around climate change in China has accelerated significantly in the past two to three years — and it's now more likely a question of how its decarbonization will evolve, rather than if it will evolve.