15 Mar 2021 | 09:48 UTC — Insight Blog

Commodity Tracker: 5 charts to watch this week

Featuring S&P Global Platts

European carbon emission prices rise to fresh highs while in the US, tight gas supply in the Permian is driving up premiums at key Texas hubs. Plus, trends in steel and its raw materials, and sustainable aviation fuel adoption in Asia.

1. EU carbon breaks new record as difficulties of border tax proposal emerge

What's happening? The price of emitting a ton of carbon dioxide in Europe pushed up again to a new all-time high of over Eur42/mt after the EU Parliament backed a proposed Carbon Border Adjustment Mechanism (CBAM) on March 10. The market has also taken support from strength in the wider energy complex as well as ongoing bullish sentiment over an expected longer-term tightening of supply.

What's next? If passed into law, the CBAM would place a charge on the carbon content of goods imported into Europe starting 2023. The CBAM paves the way for a possible phasing out of free carbon allowances for Europe's industrial companies, although the parliament removed language specifying this in the agreed text on March 10. This has turned the issue of free allocation into a political football and creates uncertainty over whether the CBAM—to be proposed under legislation in June—will comply with WTO rules on trading. The market will also be watching out for signals in the oil and gas markets, which filter through into carbon via the coal-to-gas fuel switching price for electricity generation.

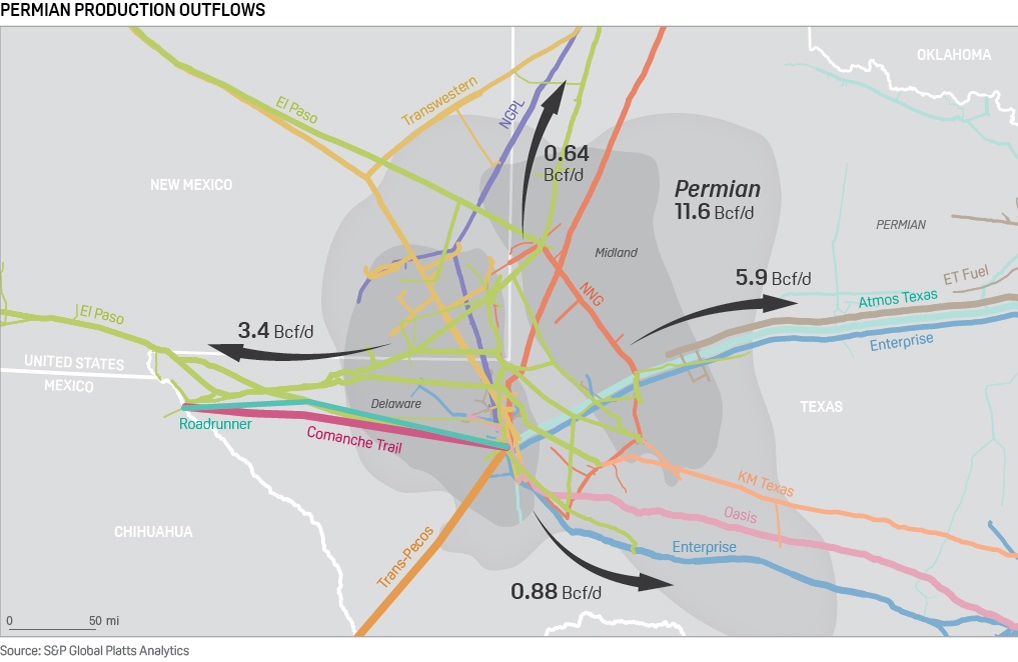

2. Permian gas supply tightness in focus for Texas market

<

Click to enlarge map

What's happening? Demand hubs like Houston Ship Channel (HSC) and Texas Eastern South Texas (STX) are having to price at a premium to incentivize stronger inflows from either the US Permian or Henry Hub areas. This price premium has been present despite Kinder Morgan's Permian Highway Pipeline entering service on Jan. 1, increasing Permian takeaway capacity to the Katy area by 2 Bcf/d. A driving factor has been low supply from producers amid growing demand, mainly in the form of LNG feedgas consumption.

What's next? The market tightness has gained more attention recently as the forwards for both HSC and STX are trading at premium to Henry Hub for most of 2021 and into the beginning of 2022. S&P Global Platts Analytics is forecasting US Gulf Coast LNG terminals to be running near full capacity through the end of 2021, based on contractual obligations and current netbacks pricing.

3. European flat steel sees fresh price rally as material shortage, mills backlog intensify

What's happening? European hot-rolled coil prices are seeing a fresh price rally following offer increases by producers. At Eur780/mt ex-works Ruhr March 11, the Platts HRC assessment is nearing the all-time high from 2008 at Eur800/mt EXW Ruhr, while the Italian Platts HRC assessment at Eur760/mt EXW Italy is just Eur5/mt below its all-time high. In contrast to 13 years ago, when the rally was primarily driven by speculation, the current increases are stemming from persistent undersupply and demand that is outpacing ramp up at mills. As a result, steel inventory levels in Germany, Europe's biggest steel market, are at a 33-year low.

What's next? Although mills are expected to increase their capacity utilization in Q2, there is little hope that lead times will be shortened in the near term as they must work through an order backlog first. Several European mills have delivery delays of up to three months and buyers are struggling to find competitive import opportunities.

4. Middle East, North Africa DRI production rebounds in January, scrap prices rise

What's happening? Direct reduction iron (DRI) production in key Persian Gulf and North African markets such as the UAE, Egypt and Saudi Arabia increased in January from rates last year, following stronger ferrous scrap and regional steel prices. DRI-based steel plants in the region typically produce long steel products such as rebar and sections, and steel demand rose as construction resumed after the initial COVID-19 pandemic. A recovery in oil and gas prices towards the end of 2020 boosted sentiment further.

What's next? Iron ore pellet premiums and overall prices have risen in early 2021, putting pressure on costs at DRI plants. Regional steel markets are closely tracking scrap, pig iron and DR pellets with steel prices and demand to gauge support for DRI operating rates. Higher scrap prices generally favor DRI plants, which rely on iron ore and natural gas. Middle East and North African DRI plants in 2020 saw weaker production than in 2019, with tight iron ore pellet availability and relatively high costs compared with scrap limiting DRI operating capacity in the past two years.

5. SAF adoption no longer a long-haul flight in Asia

What's happening? Sustainable aviation fuel has been slow to take off in Asia due to hurdles including unfavorable economics. But the drive to reduce emissions and need to maintain reputational goodwill, along with ready feedstock availability in Asia, is likely to spur SAF adoption. Neste last year tied a deal with Japan's largest airline, All Nippon Airways, representing the refiner's first SAF supply agreement with an Asian airline. Hong Kong's Cathay Pacific in 2019 voiced support for the Carbon Offsetting and Reduction Scheme for International Aviation, and is cutting reliance on fossil fuels through biofuels use and other measures. Airbus offers SAF-powered delivery flights from some of its US and European centers, and wants to roll this option out in Tianjin as well.

What's next? Under the radar, other Asian airlines are also planning to adopt SAF with full zest as supply ramps up, industry sources said. However, they cited a need to de-risk industry loans, provide support through government grants, and conduct further research and development globally, to increase its use. Increased offtake agreements, greater industry collaboration, and linking loans to SAF use would also accelerate the energy transition pathway, they added.

Reporting by Laura Varriale, Surabhi Sahu, Ng Jing Zhi, Hector Forster, Frank Watson and Harry Weber