09 Jun 2021 | 10:29 UTC — Insight Blog

Europe’s nascent bionaphtha market gearing up to serve demand for cleaner fuels and petchems

The first instalment of a two-part series taking a broad look at the developing market for bionaphtha, this article focuses on supply, production and pricing. Read the second instalment: Regulation, consumer demand drive bionaphtha use in fuels, petchems

From the production of greener gasoline to lower-carbon plastics, bionaphtha is a versatile product poised to be key in the transition to a cleaner energy future.

Driven by innovative technologies and emerging regulations, supply of, and demand for, bionaphtha are building across Europe, alongside the potential for a liberalized, transparently priced market.

From "Greek fire" to renewable fuel

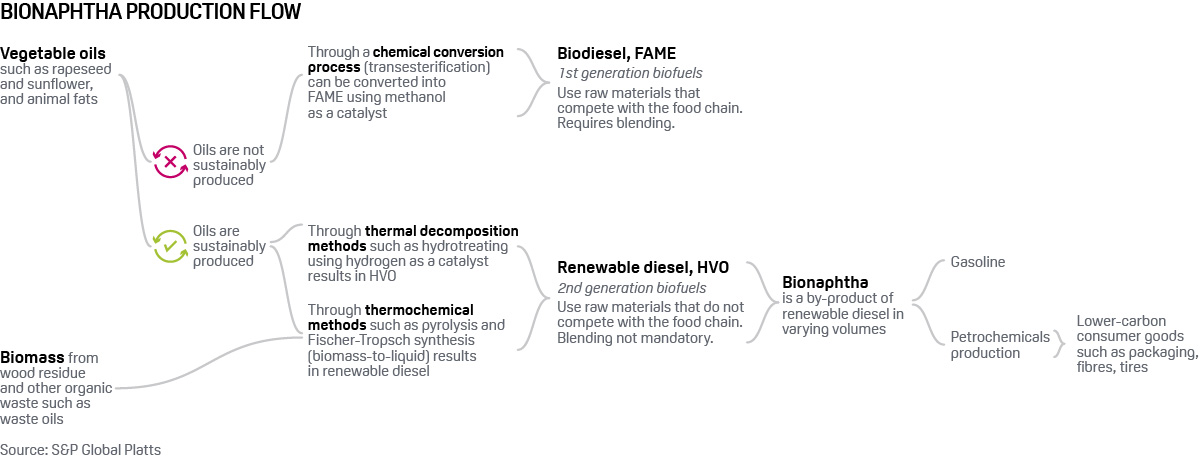

It's tempting to refer to naphtha as "Greek fire"—it was the base for the secret formula of the Byzantine Greeks' superweapon of the seventh century—so let's start with some clarity on what we mean by bionaphtha. The terms bionaphtha, green naphtha and renewable naphtha are largely used interchangeably for the same product, which we'll refer to as bionaphtha for consistency.

Although an emerging market, bionaphtha is largely a byproduct of the more lucrative and well-known renewable diesel. Unlike naphtha, it's worth noting that the definitions for the better-known biomass-based diesel are not interchangeable and denote different products.

Traditional biodiesel is a first generation fatty-acid-methyl-ester (FAME) product, created from vegetable oil and fats. Renewable diesel is a second-generation hydrotreated vegetable oil (HVO) product from renewable waste and other raw materials not competing with the food chain. European bionaphtha is a byproduct of second-generation biofuels, such as HVO, not FAME.

Bionaphtha, just like legacy naphtha, is primarily used as a gasoline blending component or a feedstock for petrochemical crackers that make ethylene, propylene and butadiene, key for consumer plastics production. Alternatively, if there is a demand shortage, it can be used to fuel refinery operations.

Bionaphtha specifications

Bionaphtha shares a similar molecular makeup to its fossil fuel cousin, and has the same uses as a petrochemical feedstock or gasoline blendstock.

There are several different grades of naphtha, with the predominant in Europe being Platts' benchmark open specification. Producers say bionaphtha can meet the legacy naphtha specification.

Naphtha end users look closely at paraffinic content—which petrochemicals producers want in higher quantity—naphthenes and aromatics. They also check contaminants such as sulphur and chloride levels. The range between the initial and final boiling points in Europe can often span between 30C-210C, while the benchmark open specification ranges from 30C-180C.

Not many bionaphtha grades have specs that are publicly available, but UPM BioVerno naphtha, for example, includes a maximum sulphur content of 10 mg/kg, maximum boiling point of 210 C, and density at 15 C of maximum 775 kg/m3, making it largely paraffinic and therefore attractive for petrochemical cracking operations.

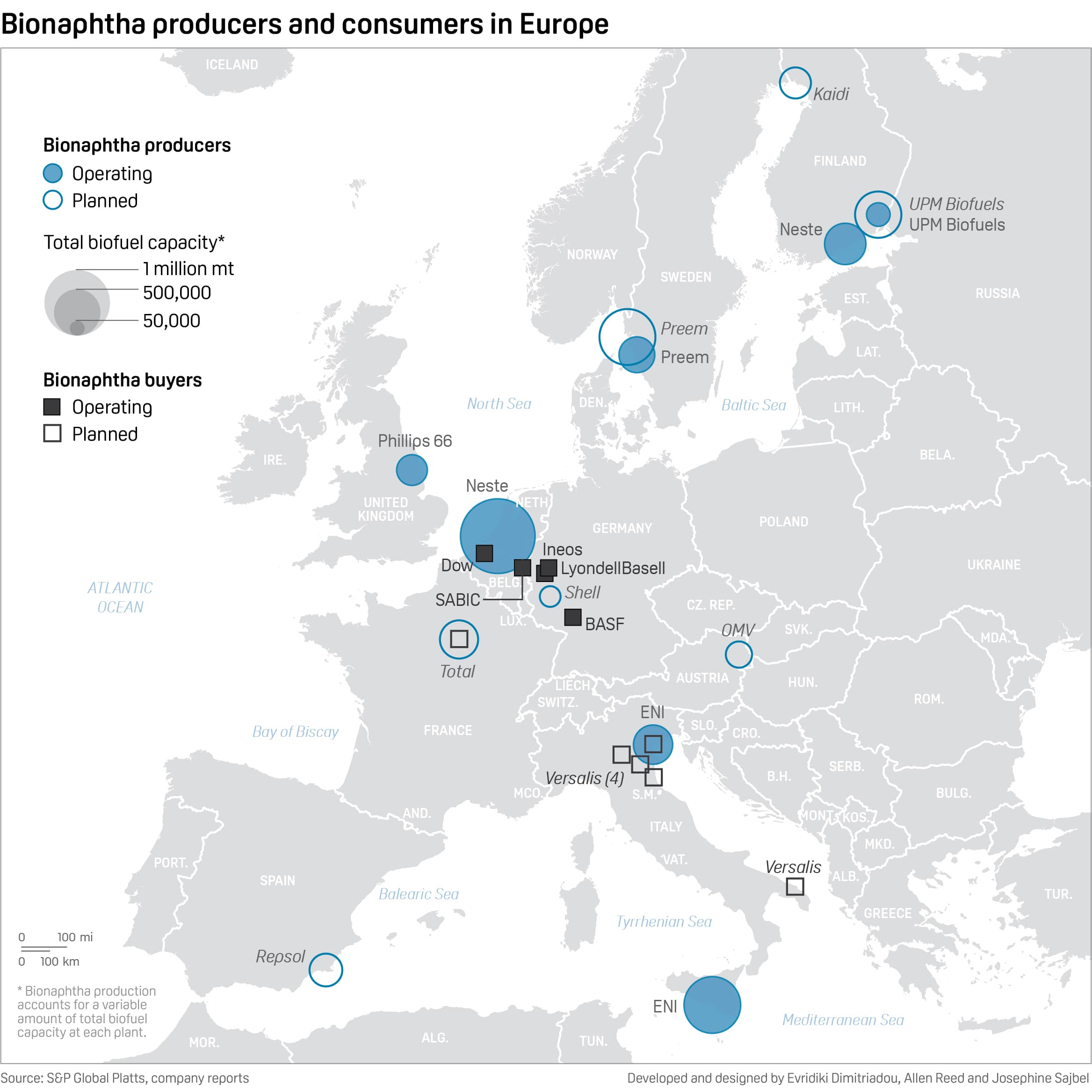

European biorefining capacity

While most companies proudly display their bio-bonafides, the amount of production that is specifically bionaphtha is much harder to ascertain as most do not report fixed production levels. As in traditional naphtha production, output will fluctuate depending on the cost of raw materials, demand levels and other factors.

From current biorefineries, bionaphtha could likely account for 5% of total output, according to industry sources. Of that, more than 90% is already committed to buyers, leaving some room for spot activity. While production volumes are growing, most material doesn't yet reach the open market. Producers such as ENI and Preem often supply their own downstream operations.

Global supply is estimated at 250,000 mt-500,000 mt per year, with Europe responsible for more than 100,000 mt, according to industry sources.

However, as demand is anticipated to grow in the next three to five years, total supply volumes are set to double in line with expanding European capacity, with notable growth projected in the next five years. There has been much media reporting on diesel or sustainable aviation fuel production, but bionaphtha is a byproduct and will grow as well.

Although renewables production does not currently enjoy the same profitability as oil, capital investments are certainly evidence that the market is motivated by more than wishful thinking.

Neste's Q1 2021 financial report showed that the company's renewable products segment, which includes bionaphtha and biopropane, accounted for 90% of total operating profits, up from 66.3% in 2018. The increase followed capital expenditures in these areas that represented 89% of the total in Q1 2021, compared to 33% in Q1 2018. Neste's current annual production capacity—including its Singapore refinery—totals 3.2 million mt of renewables, with global production capacity set to increase to 4.5 mt in 2023, a company spokeswoman said.

UPM's branded BioVerno bionaphtha is sold into both gasoline blending and bioplastics production. The company is planning a second biorefinery with a 500,000 tons/year capacity.

"We are increasingly seeing bionaphtha as an equally important part of our business and future plans," said vice president of UPM Biofuels, Panu Routasalo.

Preem's Gothenberg, Sweden, refinery has produced diesel with 30% renewable content since 2010. In 2017 the company announced an increase from 10% to 16% in the renewable content of its Evolution-brand gasoline. The forest-derived renewable components are 10% bionaphtha, 5% ethanol and 1% ETBE.

Other entrants in the European market such as Kaidi, are also planning to produce bionaphtha on a commercial scale as the product is anticipated to be important for both plastics production and transportation fuels, said Sunshine Kaidi CEO, Pekka Viljakainen.

While Scandinavian producers have been leading the European renewables market growth, continental players such as TotalEnergies (formerly Total), Shell, and ENI, have increasingly expanded offerings. A side-effect of coronavirus shuttering refineries worldwide was the acceleration of some biofuel production plans.

Repsol will build Spain's first advanced biofuels plant in Cartagena, with annual total capacity of 250,000 tons of hydrobiodiesel, biojet, bionaphtha, and biopropane. The company also has plans for a renewable hydrogen plant in Bilbao by 2024, producing another key product for the energy transition.

Austria's OMV is also making investments to reduce the carbon footprint in their Schwechat refinery. The company anticipates demand for its hydrogenated biofuels to increase tenfold by 2030.

In 2019, Neste, UPM, and ENI produced a combined volume of bio-naphtha between 100,000mt-150,000 mt/year in Europe for use as a chemical feedstock, according to a Nova Institute report. The institute projects demand to grow substantially.

Many companies provide more information on their wider biofuels offering than bionaphtha specifically. Phillips66 entered the European renewable diesel market in 2018 with its Humber, UK, refinery and is planning to increase capacity to 5,000 bpd by 2024. Although it is unclear whether renewable naphtha will be produced there the capacity likely exists.

The company plans to convert its San Francisco Refinery in Rodeo, California into one of the world's largest renewable fuels plants, bringing an initial 800 million gallons per year (52,000 bpd) of renewable fuels production capacity online by 2024, including bionaphtha.

Americas-based producers have been increasingly active in the renewable naphtha market, notably Marathon petroleum and Valero, but these volumes are not yet moving to Europe. Bionaphtha production is smaller, and thus loaded on smaller vessels, which tend to make shorter voyages or stay within a single company's system. European bionaphtha trades in small clips—one trader said 3kt was common—although it is less clear what sized vessels are used. Still, arbitrage dynamics between Europe and the US could develop depending on regulation.

Missing from this picture are several household names and as with any emerging market, other companies are likely to expand into bionaphtha as demand grows for bioplastics and transportation fuels.

Organic waste as feedstock

Bionaphtha is made from a wide range of organic materials such as wood pulp residue, vegetable oil waste, used cooking oils and fish fat. Key in this is crude tall oil (CTO), which is largely a byproduct of wood pulp production from pine trees, according to ETIP bioenergy. This takes what could be a waste product from the paper-making process and gives it new life as a renewable fuel.

Leading CTO producers include Scandinavia, Russia and the USA. According to a study by Ecofys, these countries combine for approximately 91% of global production with Scandinavia accounting for roughly 30% of that. It should come as no surprise then that prominent renewables producers are associated with Sweden and Finland, notably UPM Biofuels, Neste and Preem.

CTO's future availability is uncertain as demand is anticipated to rise sharply alongside biorefinery buildouts. Renewable transportation fuel demand rose 76% during 2010-2019 according to Eurostat and is projected to rise further alongside stricter 2030 targets in Europe set by the RED II directive. This leaves one wondering, is there is enough forest in Scandinavia?

While CTO is the predominant raw material for UPM, its planned expansion will use sustainable liquid waste and residues. Neste also uses a variety of raw materials including vegetable oil waste and residues alongside CTO.

Moving from conifers to the continent, TotalEnergies will convert its Grandpuits refinery by 2024. It will primarily use European animal fats as well as cooking oil, supplemented with other vegetable oils, excluding palm.

ENI announced in early 2021 that its chemical company Versalis will use bionaphtha and other sustainable materials to produce petrochemicals for manufacture of furniture, clothes, carpets and several other consumer products. Bionaphtha is produced at ENI's biorefineries utilizing vegetable oils, exhausted food oils or other types of organic waste.

Shell plans to produce bionaphtha at its German Rheinland refinery using biomass and green hydrogen, which is in turn produced by splitting water into hydrogen and oxygen in an electrolyser powered by renewable electricity.

Pricing patterns may vary

Similar to a healthy diet of quality fruits and vegetables, going green does not always come cheap. Renewable products including bionaphtha are currently priced at hefty premiums over fossil-fuel alternatives.

Several market participants indicated that renewable naphtha in May 2021 could be valued at between $1200/mt-$1800/mt, for example. In contrast, Platts CIF NWE benchmark naphtha averaged $592.94/mt in May 2021 and $544.57/mt in May 2019. Road fuels such as gasoline and diesel, which averaged $663.86/mt for CIF NWE gasoline cargoes and $559.54/mt for ULSD 10ppm CIF NWE cargo in May 2021 respectively, offer another yardstick for comparison.

Market sources said bionaphtha is commonly contracted, discussed and priced as a differential to its oil-based predecessor, Platts benchmark CIF NWE naphtha cargoes. Even though most volumes stay in-system or committed to term contracts, there have been several NWE spot bionaphtha trades, according to industry sources. It's unclear how often these spot trades occur or in what volumes.

Given the little spot activity it's not surprising that prices reported to Platts vary. Bionaphtha could be priced from $500-$600/mt for open specification naphtha, to a factor of 2 or 3 times more, sources said in May.

Due to the product's close relationship to renewable diesel, prices could also correlate with gasoil, sources said. This would also be a steep premium, above the range of $500-600/mt in Europe, they said. Additionally, each producer's biorefinery economics will vary, also influencing volatility in pricing. Production costs would comprise raw materials, storage facilities, processing, and transportation to name a few elements.

Capital expenditures will also likely trickle down into the price. Key players have substantially invested in research and development since continuous technological advancement is common in biofuels. Crucially, substantial capacity expansion and infrastructure investment is required, which tie invested capital for much lengthier time periods than standard exploration and production oil operations. We will expand on these topics however in part two.

Bionaphtha is an emerging market without firm standards or norms, and little by way of public information. If you would like to give feedback on this report or discuss any of the issues raised further, please contact evridiki.dimitriadou@spglobal.com.